Key Summary (65 words)

Chahe aap ₹10,000 kama rahe ho ya ₹1 lakh, financial planning ka funda same rehta hai sirf numbers change hote hain, principles nahi. India mein rising inflation, unpredictable income aur financial literacy ki kami ke beech, structured planning hi long-term security deti hai. Yeh blog batayega ki kaise same strategy har income level par kaam karti hai, aur kaise POSP jaise opportunities se aap apni income ko multiply bhi kar sakte hain.

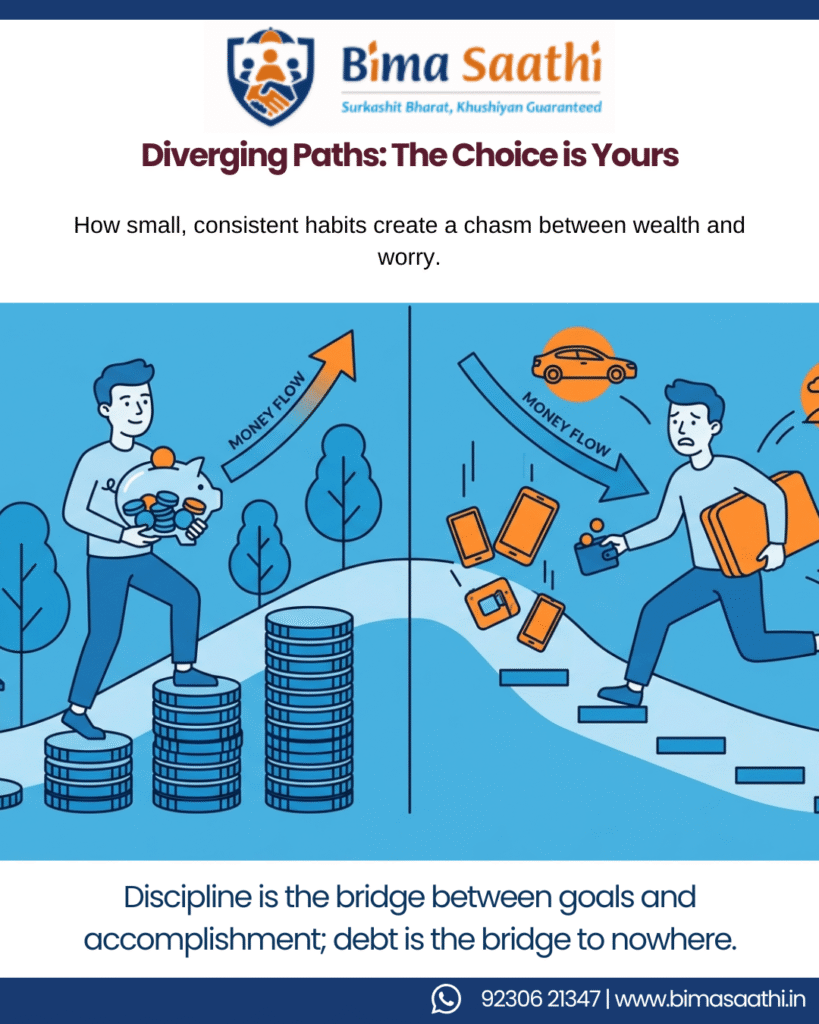

₹10,000 Salary Ho Ya ₹1 Lakh – Planning Same Kyun Honi Chahiye

“Income badalne se life improve hoti hai, lekin planning badalne se future secure hota hai.”

Aksar log sochte hain ki financial planning sirf unke liye hai jo ₹50,000+ ya ₹1 lakh kama rahe hain. Reality? Planning ka game salary se nahi, discipline se jeeta jaata hai.

Aap ₹10,000 kamao ya ₹1 lakh agar planning nahi hai, toh dono situations mein financial stress almost same hi feel hota hai.

1. Income Change Hoti Hai, Expenses Automatically Adjust Ho Jaate Hain

India mein ek interesting pattern hai jaise hi income badhti hai, expenses bhi uske saath race laga dete hain.

- ₹10,000 salary → basic survival (rent, food, transport)

- ₹1 lakh salary → lifestyle upgrade (EMIs, dining out, gadgets, travel)

Stat: According to RBI household surveys, urban Indian households spend 60–70% of income on lifestyle & consumption, regardless of income bracket.

Iska matlab kya hai?

Zyada kamaane se savings automatically nahi badhti.

“Aaj ₹10,000 mein struggle hai, kal ₹1 lakh mein bhi ‘kahan gaya paisa?’ wali feeling aa sakti hai.”

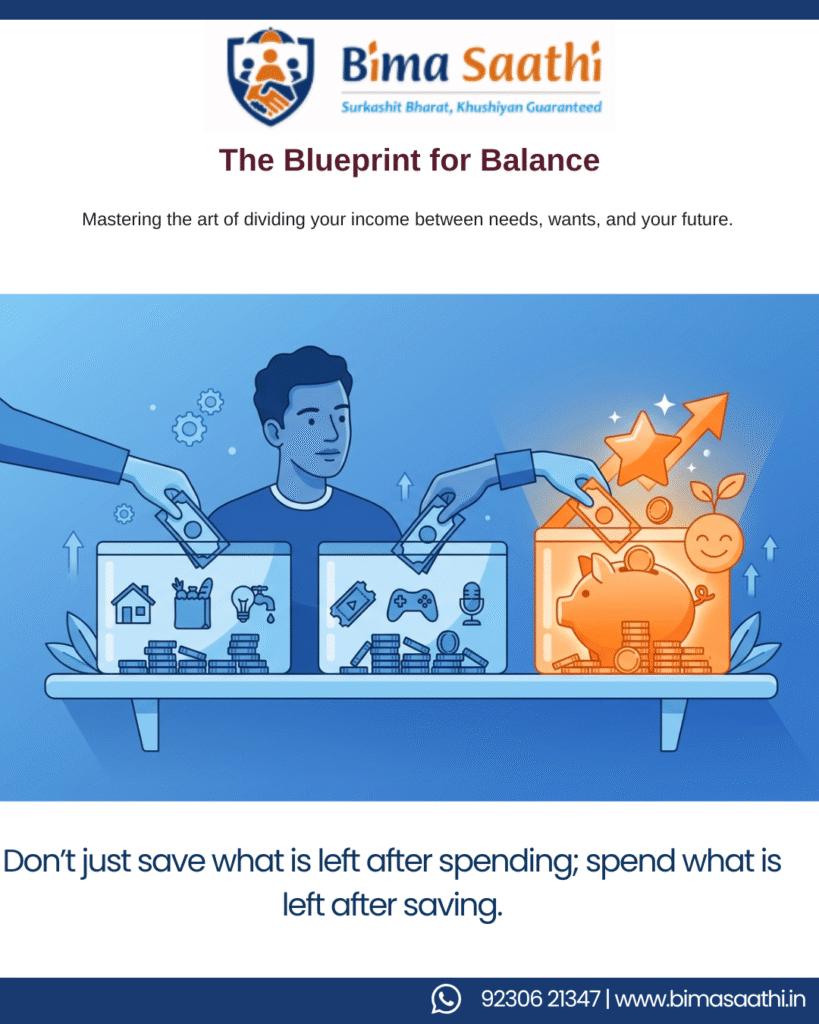

2. Financial Planning = System, Not Salary

Chahe income kuch bhi ho, ek strong financial system same hi hota hai:

Basic Structure:

- 50% Needs

- 30% Wants

- 20% Savings & Investments

Agar ₹10,000 kama rahe ho:

- ₹2,000 bhi save karna powerful hai

Agar ₹1 lakh kama rahe ho:

- ₹20,000 save nahi kiya, toh problem hai

Stat: India ka average savings rate 30% ke around hai, lekin urban youth mein yeh 15–20% tak gir chuka hai.

“System follow karoge toh chhoti income bhi grow karegi, warna badi income bhi slip ho jayegi.”

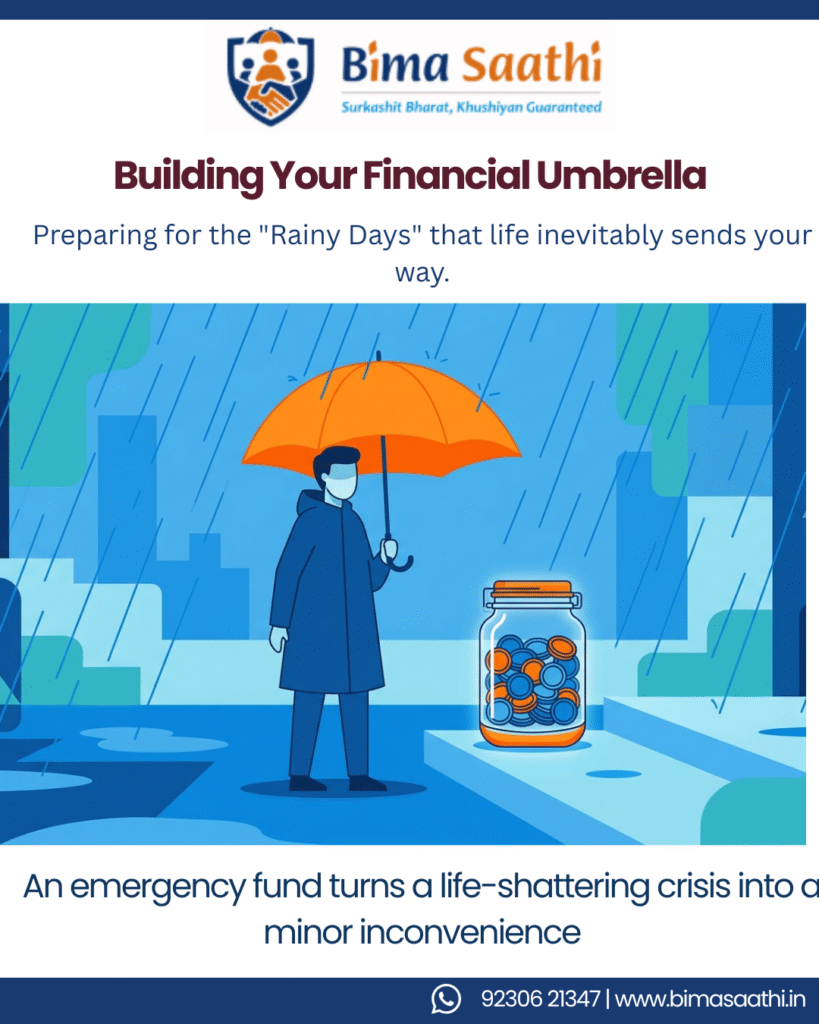

3. Emergency Fund – Sabke Liye Zaroori

Emergency aapki salary dekh kar nahi aati.

- Medical emergency

- Job loss

- Family crisis

Experts recommend:

👉 At least 3–6 months of expenses saved

Example:

- ₹10,000 earner → ₹30,000–₹60,000 emergency fund

- ₹1 lakh earner → ₹3–₹6 lakh emergency fund

COVID-19 ke time pe millions of Indians ne realise kiya ki savings hona luxury nahi, necessity hai.

“Jab income rukti hai, tab planning ka asli test hota hai.”

4. Insurance – Risk Sabka Same Hai

Risk kisi income group ka wait nahi karta.

- Accident

- Illness

- Death

Stat: India mein 70% population underinsured hai (IRDAI data).

Agar ₹10,000 kamaane wala insaan family ka breadwinner hai, toh uski importance kam nahi hoti.

Basic coverage:

- Term Insurance

- Health Insurance

Premiums bhi affordable hote hain:

- ₹500–₹1000/month mein decent cover mil sakta hai

“Income chhoti ho sakti hai, lekin responsibility kabhi chhoti nahi hoti.”

5. Investments – Amount Nahi, Habit Important Hai

Log bolte hain:

👉 “Mere paas invest karne ke liye paise nahi hain”

Truth:

👉 “Aapne invest karne ki habit nahi banayi”

Example:

Scenario A:

- ₹2,000/month SIP

- 12% return

- 20 years

→ ₹20 lakh+ corpus

Scenario B:

- ₹20,000/month SIP

- Same return & time

→ ₹2 crore+ corpus

Difference? Sirf amount.

Principle? SAME.

“Consistency > Amount. Time > Timing.”

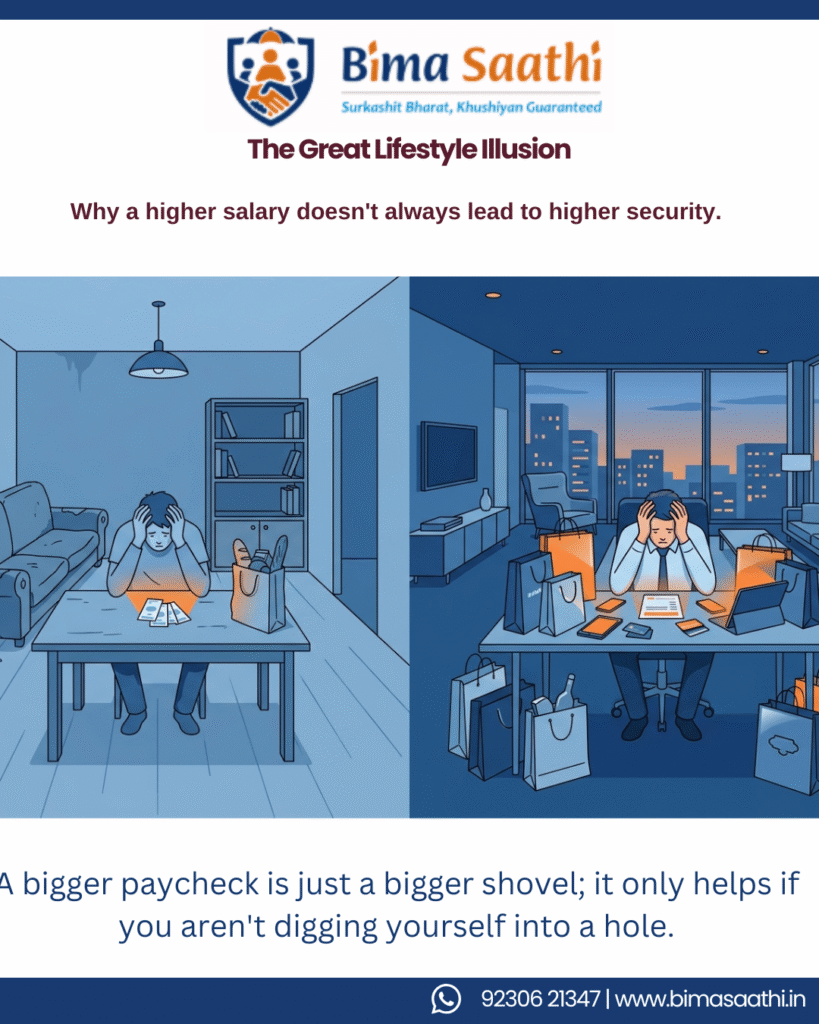

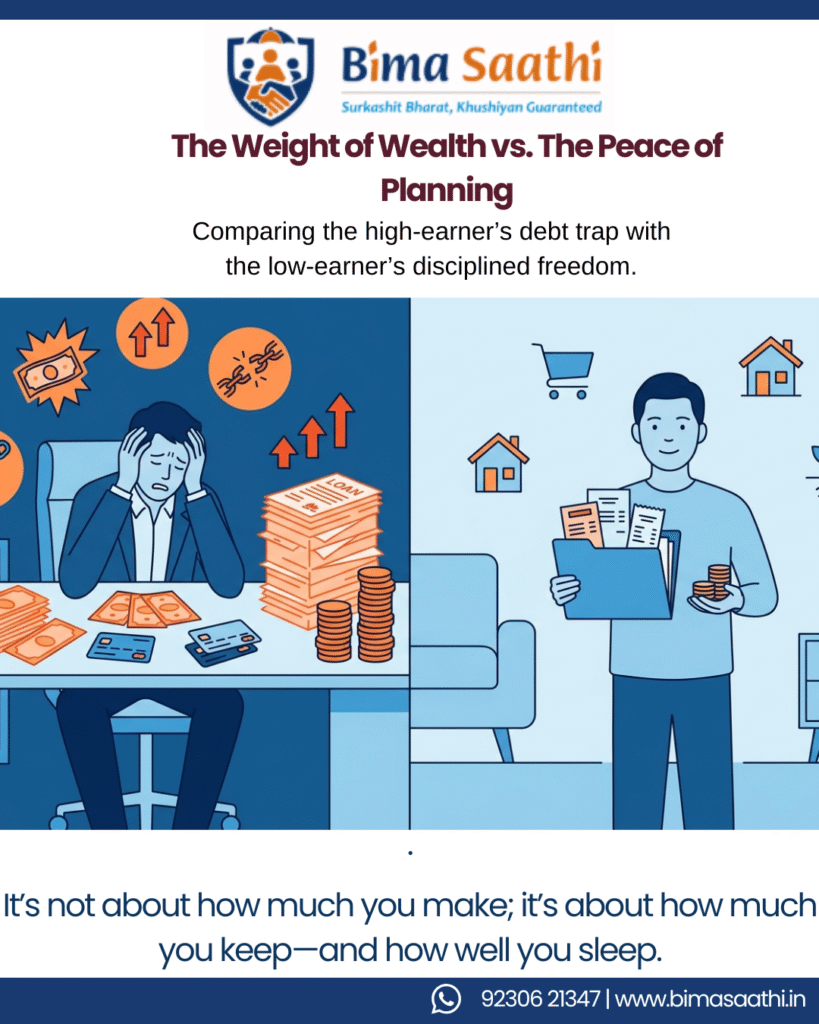

6. Financial Stress Income Se Nahi, Mismanagement Se Aata Hai

Ek ₹1 lakh kamaane wala insaan bhi stress mein ho sakta hai agar:

- EMI high hai

- Savings zero hai

- Credit card debt hai

Aur ₹10,000 kamaane wala insaan peaceful ho sakta hai agar:

- Expenses controlled hain

- Savings discipline hai

Stat: A survey by LocalCircles found that over 60% Indians feel financial stress, even in higher income brackets.

“Problem paisa kam hone ki nahi, control na hone ki hoti hai.”

7. POSP Career – Income Ko Break Karne Ka Smart Tarika

Ab sawal aata hai agar planning same hai, toh income kaise badhayein?

Yahan aata hai POSP (Point of Sales Person) opportunity.

- Flexible work

- Zero heavy investment

- Commission-based earning

- Side hustle ya full-time career

India mein insurance penetration abhi bhi low hai (~4%), jo ek huge opportunity create karta hai.

Aap:

- Apni financial planning strong bana sakte ho

- Dusron ki help karke earn bhi kar sakte ho

“Aaj planning seekhoge, kal planning se kamaoge.”

8. Real Life Example

Ravi (₹10,000 salary)

- ₹2,000 savings

- ₹500 insurance

- ₹1,000 SIP

10 saal baad:

→ Financial stability + side income from POSP

Aman (₹1 lakh salary)

- ₹0 savings

- ₹40,000 EMI

- ₹20,000 lifestyle

10 saal baad:

→ High income, low net worth

“Income nahi, decisions aapki life define karte hain.”

9. Same Planning, Different Speed

Ek simple analogy:

- ₹10,000 income = cycle

- ₹1 lakh income = car

Destination same hai → Financial Freedom

Bas speed different hai

Lekin agar direction galat hai, toh car bhi galat jagah pahunchayegi.

“Speed se zyada zaroori direction hoti hai.”

10. How to Start Today (Action Steps)

Chahe aap kisi bhi income level par ho:

✔ Track your expenses

✔ Start emergency fund

✔ Get basic insurance

✔ Begin SIP (even ₹500)

✔ Explore POSP opportunity

Aaj start karna perfect planning se better hai.

“Perfect plan ka wait karoge, toh life imperfect hi reh jayegi.”

Useful Resources

Agar aap financial planning aur insurance career ko seriously lena chahte ho, toh yeh resources help karenge:

👉 Start your journey as a POSP

https://bimasaathi.in/posp-insurance-agent

“Apni income ko next level pe le jaane ka smart tareeka”

👉 Learn basics of insurance planning

https://bimasaathi.in/insurance-guide

“Financial protection samajhna hi real wealth ka start hai”

👉 Explore earning opportunities with BimaSaathi

https://bimasaathi.in/earn-with-us

“Jahan learning bhi hai aur earning bhi”

FAQs (SEO Optimised)

1. Why should financial planning be same for all income levels?

Financial planning principles remain same because expenses, risks, and goals exist at every income level.

2. How much should I save from a ₹10,000 salary in India?

You should aim to save at least 20%, even if it means starting with ₹1,000–₹2,000 monthly.

3. Is SIP investment possible with low income in India?

Yes, you can start SIP with as low as ₹500 and build long-term wealth through consistency.

4. What is POSP and how can it increase income?

POSP is an insurance advisor role where you earn commission by selling policies with flexible working hours.

5. Why do high-income earners still face financial stress?

Because of poor money management, high expenses, and lack of savings or investments.

Connect With Us

Agar aap sirf paisa kamaana nahi, balki usse grow karna aur secure future build karna chahte ho toh abhi action lene ka time hai.

BimaSaathi ke saath:

✔ Financial planning seekho

✔ Insurance samjho

✔ POSP ban kar earning start karo

📞 Call/WhatsApp: +91 9324981867

📧 Email: support@bimasaathi.in

🌐 Website: https://bimasaathi.in/

“Kal ka wait mat karo. Aaj ka decision hi kal ka lifestyle banata hai.”

Leave A Comment