Key Summary

Financial priorities set karna sirf budgeting nahi hai it’s about deciding where your money should go before life decides for you. From emergency funds and insurance to investments and retirement planning, the right financial priorities help you avoid stress, debt, and confusion. Is blog mein hum practical examples, real statistics, and simple strategies ke through samjhenge ki kaise smart financial planning aapko financially secure aur mentally relaxed bana sakti hai. Kyunki “salary aani important hai, lekin salary bachni aur grow karni usse bhi zyada important hai.”

Financial Priorities Set Karna Itna Important Kyun Hai?

Aaj ke time mein paisa kamana tough hai, aur usse sambhalna usse bhi tough. India mein inflation average 5–6% ke around chal raha hai. Matlab agar aapka paisa sirf savings account mein pada hai, toh technically uski value dheere dheere kam ho rahi hai.

According to a 2024 survey by DSP Mutual Fund, around 72% Indians feel financially stressed, aur major reason hai lack of financial planning.

Bahut log salary aate hi:

- EMI bhar dete hain

- random online shopping kar lete hain

- “salary toh next month aa hi jayegi” mindset mein rehte hain

Phir month-end mein account balance bolta hai:

“Hum toh aapke hain kaun?”

Isi liye financial priorities set karna zaroori hai.

Step 1: Sabse Pehle Emergency Fund Banao

Agar kal job chali gayi ya sudden medical expense aa gaya toh?

Emergency fund aapka financial seatbelt hota hai.

Ideal Emergency Fund:

- Salaried employees: 6 months expenses

- Freelancers/business owners: 9–12 months expenses

Example:

Agar aapka monthly expense ₹40,000 hai:

- Minimum emergency fund = ₹2.4 lakh

Is amount ko:

- Savings account

- Liquid mutual fund

- Sweep FD

mein rakh sakte hain.

COVID ke time millions logon ko realise hua:

“Income temporary ho sakti hai, expenses nahi.”

Step 2: Insurance Ko Expense Nahi, Protection Samjho

India mein healthcare costs rapidly badh rahe hain.

Ek private hospital mein:

- Minor surgery: ₹1–2 lakh

- ICU stay: ₹25,000+ per day

Agar health insurance nahi hai, toh savings ka “Game Over” bahut jaldi ho sakta hai.

Priority Insurance Checklist:

1. Health Insurance

At least:

- Individual: ₹5–10 lakh cover

- Family floater: ₹10–20 lakh

2. Term Insurance

Agar aapke dependents hain, toh term plan must hai.

Ideal cover:

- Annual income ka 10–15x

Example:

Income = ₹12 lakh/year

Recommended term cover = ₹1.2–1.8 crore

Insurance ka purpose investment nahi hota.

Uska kaam hota hai “financial damage control.”

Life unpredictable hai. Premium predictable rakho.

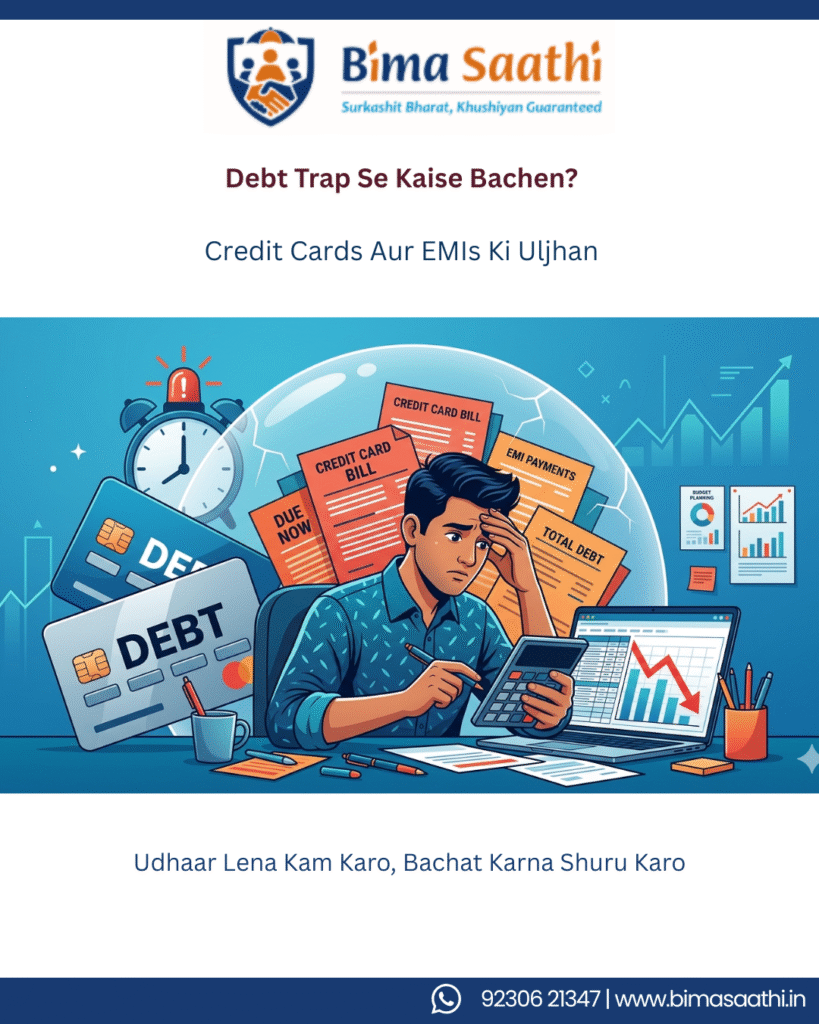

Step 3: High-Interest Debt Ko Jaldi Khatam Karo

Credit card debt sabse dangerous financial trap ho sakta hai.

India mein credit card interest:

- 30%–42% annually tak ja sakta hai.

Agar ₹1 lakh ka outstanding hai aur minimum due bharte rahe, toh repayment years tak stretch ho sakta hai.

Debt Priority Order:

- Credit card debt

- Personal loan

- Consumer durable EMI

- Car loan

- Home loan

Smart Strategy:

Use the Avalanche Method

- Highest interest debt pehle clear karo.

Kyuki:

“EMI chhoti lagti hai… until total interest dekh lo.”

Step 4: Financial Goals Clearly Define Karo

“Paise bachane hain” koi goal nahi hota.

Specific goals define karo.

Good Financial Goals Examples:

- 2 years mein Europe trip ke liye ₹3 lakh

- 10 years mein house down payment ₹20 lakh

- Retirement corpus ₹5 crore

- Child education fund ₹25 lakh

SMART Formula Use Karo:

- Specific

- Measurable

- Achievable

- Relevant

- Time-bound

Financial goals clear honge toh spending automatically disciplined ho jaati hai.

Step 5: Investing Jaldi Start Karo

Sabse bada financial mistake?

“Invest karne ke liye perfect time ka wait karna.”

Perfect time usually kabhi nahi aata.

According to AMFI data:

- SIP investors in India crossed 10 crore accounts in 2025

- Long-term equity mutual funds historically delivered around 10–14% annualised returns

Example of Compounding:

Agar aap:

- ₹5,000 monthly SIP

- 12% annual return

- 25 years

invest karte ho…

Approx corpus:

- ₹95 lakh+

Total investment:

- ₹15 lakh only

Compounding silently kaam karta hai.

Bilkul uss dost ki tarah jo kam bolta hai but sabse reliable hota hai.

Step 6: Retirement Planning Ko Ignore Mat Karo

Retirement planning sirf “old people topic” nahi hai.

Aaj retirement age ke baad average life expectancy:

- 75+ years

Matlab retirement ke baad bhi 20–25 saal expenses chalenge.

Common Mistake:

“Bachche sambhal lenge.”

Reality:

- Nuclear families

- rising expenses

- changing lifestyles

make self-dependent retirement more important than ever.

Retirement Rule:

Invest at least:

- 15–20% of income for retirement

Options:

- EPF

- PPF

- NPS

- Mutual Funds

Retirement planning ka best time kal tha. Dusra best time aaj hai.

Step 7: Lifestyle Inflation Ko Control Karo

Salary badhte hi:

- iPhone upgrade

- expensive subscriptions

- unnecessary dining

- luxury EMI

ye sab quietly budget destroy kar dete hain.

Isko kehte hain:

Lifestyle Inflation

Example:

Salary:

- Earlier = ₹50,000

- Now = ₹1 lakh

But savings same hi hai.

Problem income ki nahi. Habits ki hai.

Smart Rule:

Whenever salary increases:

- 50% savings/investment increase

- 50% lifestyle upgrade

Balance bhi rahega aur future bhi secure hoga.

Step 8: Budgeting Boring Nahi, Powerful Hai

Budgeting ka matlab “khushiyan sacrifice” nahi hota.

Budgeting simply means:

“Money ko direction dena.”

Popular Rule:

50-30-20 Rule

- 50% Needs

- 30% Wants

- 20% Savings & Investments

Example:

Income = ₹80,000

- Needs = ₹40,000

- Wants = ₹24,000

- Savings = ₹16,000

Simple systems long-term mein best kaam karte hain.

Kyuki complicated budget Excel sheets usually 3 din mein abandon ho jaati hain.

Common Financial Priority Mistakes

1. Insurance Ignore Karna

Savings pe pura focus, protection zero.

2. Friends Ke Lifestyle Se Compare Karna

Instagram financial advisor nahi hai.

3. Investment Delay Karna

“Next month se start karunga.”

Woh next month kabhi kabhi next decade ban jaata hai.

4. Sirf Tax Saving Ke Liye Invest Karna

Investment ka purpose wealth creation bhi hai.

Financial Priorities Ka Ideal Order

Agar confusion ho ki pehle kya karein, toh ye sequence follow karo:

- Monthly budget

- Emergency fund

- Health insurance

- Term insurance

- High-interest debt repayment

- Goal-based investing

- Retirement planning

- Wealth creation investments

Simple priorities = less stress + better financial growth.

Helpful Resources from Bima Saathi

Want to Understand Financial Protection Better?

Explore:

Health Insurance Guidance by Bima Saathi

Looking for Smart Financial Planning Support?

Check out:

Financial Planning Solutions at Bima Saathi

Confused About Insurance Priorities?

Visit:

Bima Saathi Official Website

Conclusion

Financial priorities set karna complicated nahi hai. Consistency aur clarity zyada important hai.

Aapko perfect investor ya finance expert banne ki zaroorat nahi. Bas:

- smart decisions

- disciplined habits

- long-term thinking

ye teen cheezein enough hain.

Paisa emotional topic bhi hai aur practical bhi.

Isliye planning spreadsheet se nahi, mindset se start hoti hai.

“Financial freedom ek din mein nahi milti. Lekin har smart decision uske thoda aur close le jaata hai.”

“Aaj ka planned paisa, kal ka peaceful life.”

“Budget banana boring lag sakta hai… but broke rehna usse zyada boring hai.”

FAQs

1. Financial priorities set kaise karein?

Sabse pehle emergency fund, insurance, debt repayment aur investments ko priority dein. Clear financial goals banana bhi important hai.

2. Emergency fund kitna hona chahiye?

At least 6 months ke monthly expenses jitna emergency fund maintain karna ideal hota hai.

3. Financial planning kab start karni chahiye?

Jitni jaldi start karenge, compounding ka benefit utna zyada milega. Early investing long-term wealth create karta hai.

4. Salary kam ho toh investing kaise karein?

Small SIPs like ₹500–₹1,000 se bhi investing start ki ja sakti hai. Consistency amount se zyada important hoti hai.

5. Financial planning aur budgeting mein kya difference hai?

Budgeting short-term expense management hota hai, jabki financial planning long-term wealth aur goals achieve karne ki strategy hoti hai.

Connect With Us

Friendly experts se baat kariye aur apni financial priorities ko smart direction dijiye.

📞 Call / WhatsApp: + (91) 92306 21347

📧 Email: support@bimasaathi.in

🌐 Visit: www.bimasaathi.in

“Aap future ke liye kaam kar rahe ho… ensure karo future bhi aapke liye kaam kare.”

Leave A Comment