Key Summary

A strong personal financial system helps you manage income, savings, investments, insurance, debt, and future goals without daily stress. Instead of depending on motivation, you create habits and automation that work silently in the background. In this blog, you’ll learn how to build a smart financial system step-by-step using budgeting, emergency funds, insurance, investments, and tracking tools all explained in simple Hinglish with practical examples, real statistics, and actionable strategies.

How to Build a Personal Financial System That Actually Works

Money problems usually don’t happen because people earn too little.

Most of the time, they happen because there is no personal financial system in place.

Salary aati hai.

EMI jaati hai.

Weekend party hoti hai.

Aur month-end pe account balance emotional damage de deta hai.

Sound familiar?

The truth is simple: if your money doesn’t have a system, your stress definitely will.

According to a 2025 survey by PwC, nearly 57% of working professionals feel stressed about personal finances regularly. Even high earners struggle because income without structure becomes chaos.

A good personal financial system helps you:

– Track money automatically

– Build savings consistently

– Avoid unnecessary debt

– Grow investments

– Protect your family financially

– Reduce financial anxiety

And no, you don’t need to become Warren Buffett overnight.

Bas thoda discipline aur smart setup chahiye.

—

What Is a Personal Financial System?

A personal financial system is a set of habits, tools, rules, and automation that manage your money efficiently.

Think of it like Google Maps for your finances.

Without it:

– You guess.

– You overspend.

– You panic.

With it:

– Your money knows where to go.

– Your goals become clearer.

– Your future becomes more secure.

A solid system generally includes:

– Budgeting

– Emergency fund

– Insurance planning

– Debt management

– Investments

– Goal tracking

– Retirement planning

“Paise ko direction do, warna paise aapko direction denge.”

Step 1: Know Exactly Where Your Money Goes

Before fixing your finances, understand your spending patterns.

Most people underestimate their expenses by 20–30%.

That ₹299 subscription?

That random food delivery?

That “only one coffee”?

Sab milke budget ka band baja dete hain.

Use the 50-30-20 Rule

A simple framework:

– 50% → Needs (rent, groceries, EMI)

– 30% → Wants (travel, entertainment)

– 20% → Savings & investments

Example:

If your monthly income is ₹80,000:

– ₹40,000 → Essentials

– ₹24,000 → Lifestyle

– ₹16,000 → Savings/Investments

Use apps like:

– Walnut

– Money Manager

– YNAB

– Excel sheets (the underrated king)

Consistency beats complexity.

Step 2: Build an Emergency Fund First

A strong personal financial system always starts with safety.

An emergency fund protects you from:

– Job loss

– Medical emergencies

– Business slowdown

– Sudden expenses

Financial experts recommend saving at least 6 months of expenses.

If your monthly expenses are ₹50,000:

– Emergency fund target = ₹3,00,000

Keep this money in:

– High-interest savings account

– Liquid mutual funds

– Sweep FD accounts

Do NOT invest emergency funds in stocks or crypto.

Emergency fund ka purpose profit nahi, peace hai.

Step 3: Get Proper Insurance Coverage

Many Indians confuse investment with insurance.

LIC policy lene ke baad log samajhte hain “financial planning done.”

Reality thodi different hoti hai.

Essential Insurance Types

1. Health Insurance

Medical inflation in India is rising at around 12–14% annually.

A single hospitalization in metro cities can easily cost:

– ₹2 lakh to ₹5 lakh

Minimum recommended cover:

– Individual: ₹10 lakh

– Family floater: ₹20 lakh

2. Term Insurance

If someone depends on your income, term insurance is mandatory.

Rule:

– Coverage should be at least 10–15x annual income

Example:

If your yearly income is ₹12 lakh:

– Ideal cover = ₹1.5 crore approx.

Cheap coffee se zyada expensive ignorance hota hai.

For understanding insurance planning better, explore:

Protect Your Family Financially Bima Saathi Insurance Planning Guide

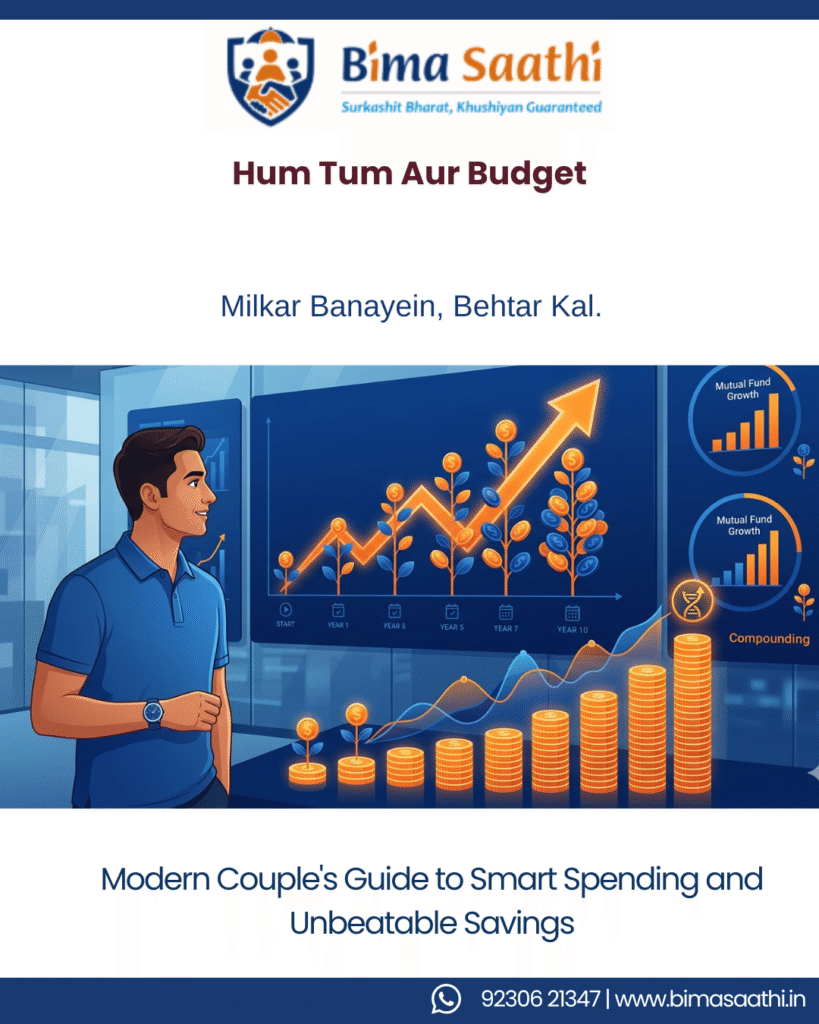

Step 4: Automate Your Savings and Investments

The biggest hack in any personal financial system is automation.

Because motivation disappears faster than salary after rent day.

Start SIP Investments

A SIP (Systematic Investment Plan) helps build wealth gradually.

Example:

If you invest:

– ₹10,000/month

– At 12% annual return

– For 20 years

You could accumulate approximately:

– ₹1 crore+

That’s the power of compounding.

Albert Einstein allegedly called compounding the “8th wonder of the world.”

Aur Indians usko ignore karke reels dekh rahe hain.

Ideal Investment Split

Depending on goals:

– Equity Mutual Funds → Long-term growth

– Debt Funds/FDs → Stability

– PPF → Safe retirement savings

– Gold → Portfolio diversification

A good thumb rule:

– Invest before spending.

– Not spend first and invest “jo bache.”

Step 5: Eliminate Toxic Debt

Not all debt is bad.

But high-interest debt is financial poison.

Dangerous Debt Examples

– Credit card dues

– Buy Now Pay Later traps

– Personal loans for luxury purchases

Average Indian credit card interest rates:

– 30–42% annually

That’s massive.

If your investment returns 12% but debt costs 36%, you’re financially running on a treadmill.

Debt Reduction Strategy

Use:

– Avalanche Method → Pay highest interest first

OR

– Snowball Method → Pay smallest loan first

Whichever keeps you consistent works best.

EMI sirf lifestyle ka symbol nahi hota. Kabhi kabhi warning sign bhi hota hai.

Step 6: Create Financial Goals With Timelines

Without goals, money disappears into random spending.

Your personal financial system should include:

– Short-term goals (1–3 years)

– Mid-term goals (3–7 years)

– Long-term goals (10+ years)

Example Goals

| Goal | Timeline | Estimated Cost |

| Emergency Fund | 1 year | ₹3 lakh |

| International Trip | 2 years | ₹2 lakh |

| House Down Payment | 7 years | ₹20 lakh |

| Retirement Corpus | 25 years | ₹5 crore |

Specific goals improve saving discipline dramatically.

Research from Dominican University found people with written goals are significantly more likely to achieve them.

Likho. Plan karo. Action lo.

Step 7: Track Your Net Worth Quarterly

Your income matters.

But your net worth matters more.

Formula

Net Worth = Assets – Liabilities

Assets:

– Savings

– Investments

– Property

– Gold

Liabilities:

– Loans

– Credit card debt

– EMIs

Tracking net worth every 3 months helps you:

– Measure progress

– Stay motivated

– Make smarter decisions

Because “busy earning” and “actually building wealth” are two different things.

Step 8: Review and Upgrade Your System Yearly

Life changes. Your financial system should too.

Review annually:

– Insurance coverage

– SIP amounts

– Tax planning

– Emergency fund

– Financial goals

Example:

If your salary increases by 20%, increase SIP investments too.

Lifestyle inflation ko control karna hi asli flex hai.

Common Mistakes People Make

1. Investing Without Insurance

One medical emergency can destroy years of savings.

2. Saving But Not Investing

Inflation in India averages around 5–7%.

Money sitting idle loses value over time.

3. Following Random Financial Influencers

“Bro trust me, crypto double hoga.”

Bro usually disappears after market crash.

4. Ignoring Retirement

Retirement planning is not an “old people problem.”

The earlier you start, the easier it becomes.

Final Thoughts

A successful personal financial system is not about being rich overnight.

It’s about:

– Control

– Clarity

– Confidence

– Freedom

Small systems create big financial results over time.

Remember:

– Automation beats motivation.

– Consistency beats intensity.

– Financial peace is the real luxury.

Aaj ka smart decision, kal ka stress kam karta hai.

And honestly, future-you deserves better than surviving on instant noodles at 58.

—

FAQs

1. What is a personal financial system?

A personal financial system is a structured way to manage income, expenses, savings, investments, insurance, and financial goals efficiently.

2. Why is a personal financial system important?

A personal financial system reduces money stress, improves savings habits, and helps achieve long-term financial goals faster.

3. How much emergency fund should I keep?

You should ideally maintain an emergency fund equal to 6–12 months of living expenses.

4. What is the best way to start investing?

Starting SIPs in mutual funds is one of the easiest and most effective ways to begin investing regularly.

5. How often should I review my financial plan?

You should review your financial plan and investments at least once every year.

Ready to Build Your Financial Future?

At Bima Saathi, we help individuals and families make smarter financial and insurance decisions with clarity and confidence.

Whether you need:

– Health Insurance

– Term Insurance

– Financial Planning Guidance

– Family Protection Solutions

We’re here to help.

📞 Call / WhatsApp: + (91) 92306 21347

📧 Email: support@bimasaathi.in

🌐 Visit: www.bimasaathi.in

“Financial planning complicated nahi hoti. Bas shuru karna difficult lagta hai.”

Leave A Comment