Key Summary

Becoming a parent in India is a milestone filled with joy, but it also triggers a massive shift in financial responsibility. With education inflation touching 10-12% and healthcare costs soaring, traditional saving methods are no longer enough. This comprehensive guide outlines the essential financial planning steps for young Indian parents—from building a robust “Protection Shield” with life and health insurance to investing smartly for long-term goals like higher education—ensuring your child’s future remains bright, no matter what life throws at you.

Introduction: The Joy, the Diapers, and the Realization

There is perhaps no greater joy in the Indian context than holding your newborn baby for the first time. The tiny fingers, the soft sighs, the overwhelming sense of love it is a magical moment. But closely following that wave of love is often a wave of mild panic.

You are no longer just planning for your next vacation or a bigger car. You are now responsible for another life’s food, shelter, education, health, and happiness for the next two decades. In India, where family bonds are tight and parental aspirations are high, this responsibility feels particularly heavy.

The cost of raising a child in India is skyrocketing. According to various industry estimates, the total cost of raising a child from birth to age 21 in a metro or Tier-1 city can easily range between ₹60 Lakhs to ₹1.2 Crores, excluding exotic foreign education.

This blog is not meant to scare you. It is meant to empower you. At Bima Saathi, we believe that the best gift you can give your child is not an expensive toy today, but a financially secure tomorrow. Let’s look at how young Indian parents can navigate this journey calmly, clearly, and responsibly.

Real-Life Scenario: A Tale of Two Planning Styles

Let’s meet two sets of young parents living in a bustling Indian city.

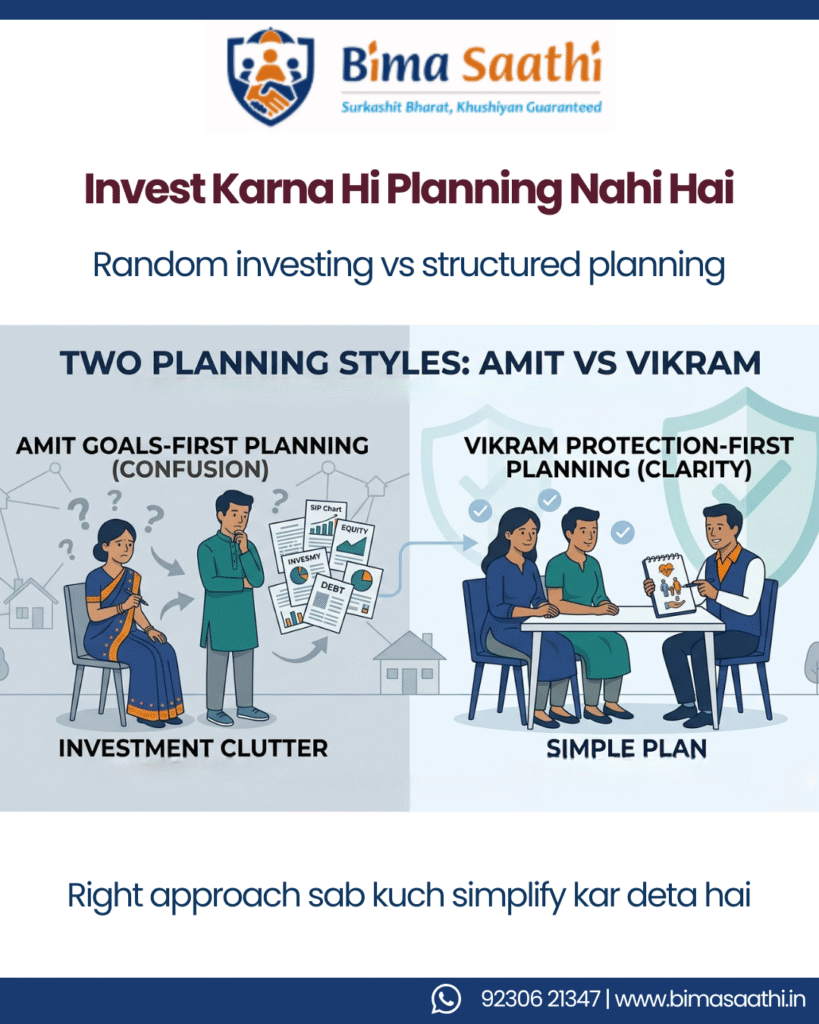

Case 1: Amit & Priya (The “Goals-First” Planners)

Amit and Priya (both 28) are aggressive savers. As soon as their daughter, Diya, was born, they opened a Sukanya Samriddhi Account (SSA) and started a high-growth SIP for her “Higher Education Fund.” They save ₹20,000 every month. However, they rely only on Amit’s corporate health cover (₹5 Lakhs) and have no separate term life insurance because they believe “Insurance mein return nahi milta” (Insurance gives no returns).

Case 2: Vikram & Megha (The “Shield-First” Planners)

Vikram and Megha (both 29) are balanced planners. Before starting any specific child-goal investment for their son, Aryan, they sat down with a Bima Saathi advisor. Their first priority was a “Protection Shield”:

A robust family float health plan of ₹10 Lakhs with a ₹20 Lakh Super Top-up.

A Term Life Insurance plan for Vikram (the main earner) with an “Income Continuity” rider, ensuring Megha gets a monthly “salary” if Vikram is not around.

Vikram and Megha only invest ₹10,000 per month for Aryan’s education, starting slower than Amit and Priya.

The Problem: The Shock of Reality (Inflation and “What Ifs”)

The standard Indian financial advice is: “Sona kharido ya FD karao” (Buy gold or make an FD). While safe, these methods often fail to beat the single biggest enemy of young parents: Inflation.

1. The Education Inflation Shock

General inflation might be 5-6%, but Education Inflation in India is closer to 10-12%.

A professional degree that costs ₹10 Lakhs today will likely cost nearly ₹40 Lakhs in 15 years.

Agar aap sirf safe instruments mein save kar rahe hain (7-8% return), your money is actually losing purchasing power against the cost of college.

2. The Medical Inflation Shock

Healthcare inflation is growing at 12-14% annually. A standard C-section delivery that costs ₹80,000 today will cost double that in a few years. Specialized child treatments travel to metros, which adds massive hidden costs. Relying only on a ₹3-5 Lakh corporate cover is incredibly risky.

3. The “Uncomfortable Conversation” (Loss of Income)

This is the hardest part. If the main earning member faces an untimely demise, a critical illness, or a permanent disability, the family’s entire economic structure collapses. Without a plan, school fees stop, home loan EMIs default, and dignity is compromised.

Solutions: The Bima Saathi Step-by-Step Guide to Financial Freedom

The only real solution is to build a comprehensive plan that integrates Protection, Continuity, and Growth.

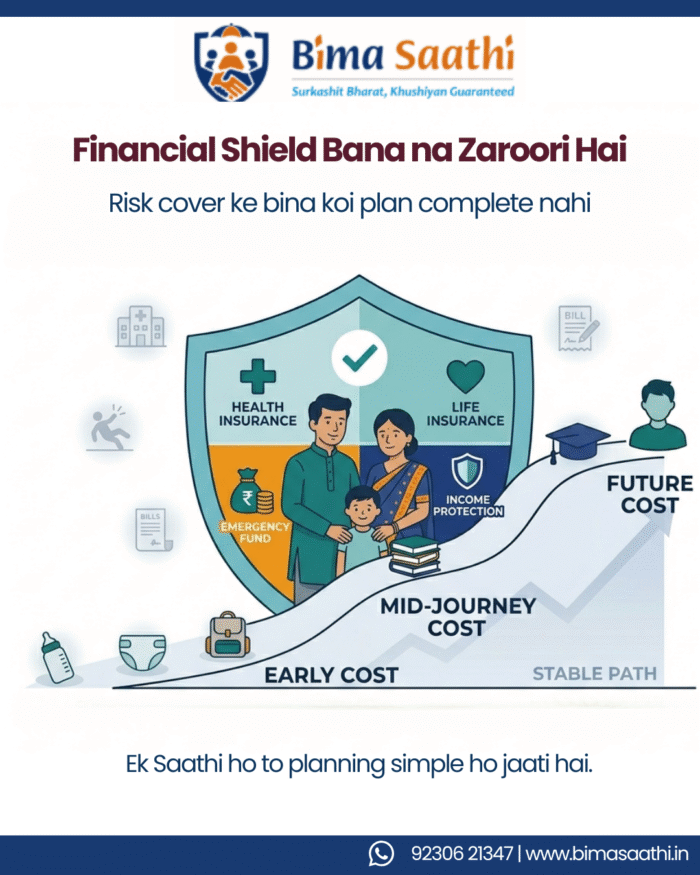

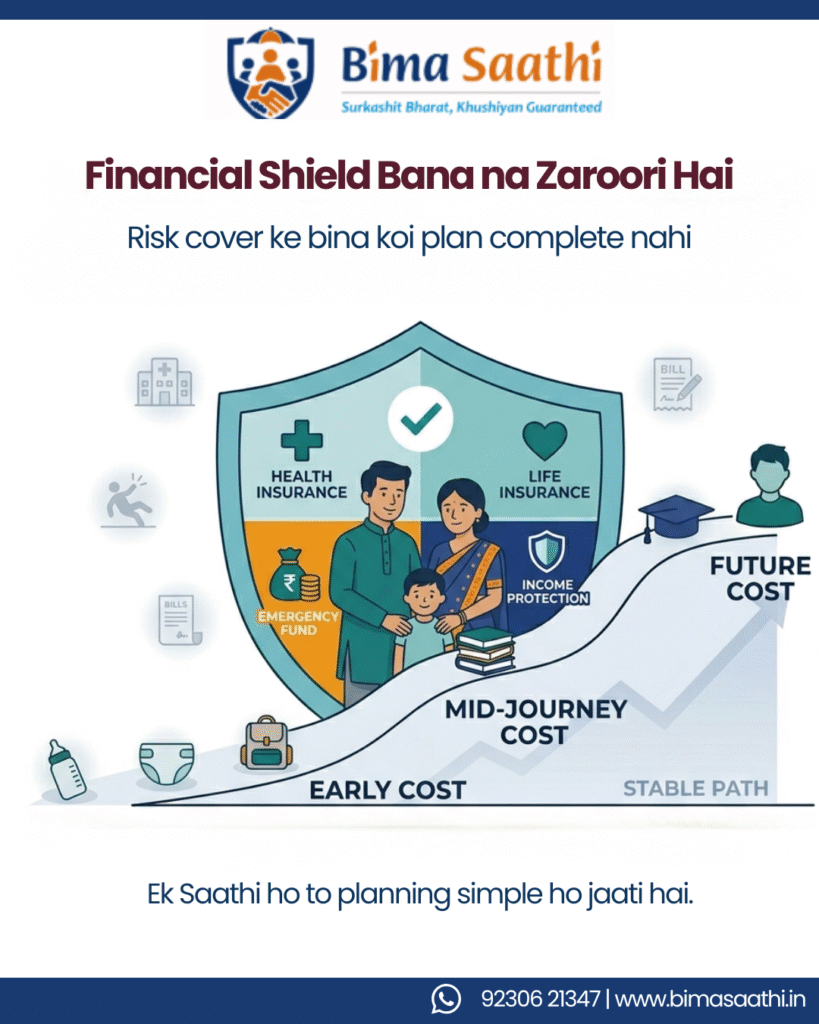

Step 1: Immediately Build Your “Protection Shield” (The Non-Negotiables)

Before you invest for the future, protect the present.

1.1. Robust Health Insurance (The Medical Shock Absorber): Do not rely on your company policy. Buy a stand-alone Family Floater Plan. If one family member faces a serious illness, your entire years of savings shouldn’t vanish. Add a Super Top-up for affordable, high-cover protection. Look for plans with Restoration Benefit, which reloads your cover if you use it up.

1.2. Term Life Insurance (The Income Continuity Shield): A Term Plan is not “death insurance”; it is Family Security. Your Sum Assured should be at least 15-20 times your annual income. If you are not there, this money ensures your child’s standard of living—their school, their home, and their dreams—remains exactly the same.

Pro Tip: Choose the “Monthly Payout” option. A lump sum of ₹1 Crore can be overwhelming and mismanaged by a grieving family. A monthly “salary” replacement is far more effective for Tier-2/3 families.

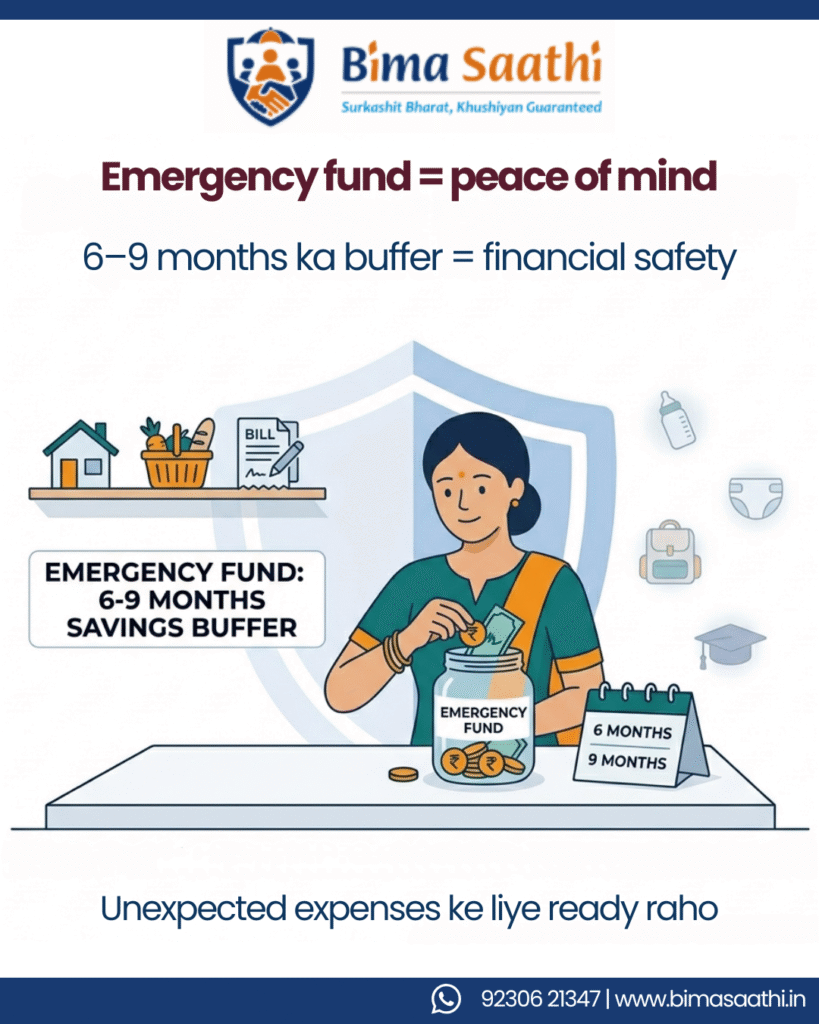

1.3 Emergency Fund – Sabse Pehla Safety Net: Before any goal, there is survival. Simple sawaal: “Agar income ruk gayi toh ghar kaise chalega?”. Your emergency fund is your first protection layer. It is the buffer that prevents you from tapping into your child’s education fund for a sudden car repair.

Experts suggest: 6–9 months of expenses

Easily accessible (savings account / sweep-in FD / liquid funds)

Example: Monthly expenses = ₹50,000. Emergency fund = ₹3–4.5 lakh.

1.4 Income Protection – The Ignored Risk: Most parents plan for what happens after death. But what about survival with disability or long-term illness? If income stops:

- expenses continue

- savings reduce

- stress increases

This gap is dangerous. “Zindagi chalti rehti hai par income kabhi bhi ruk sakti hai.” Secure a Personal Accident and Critical Illness cover to bridge this gap.

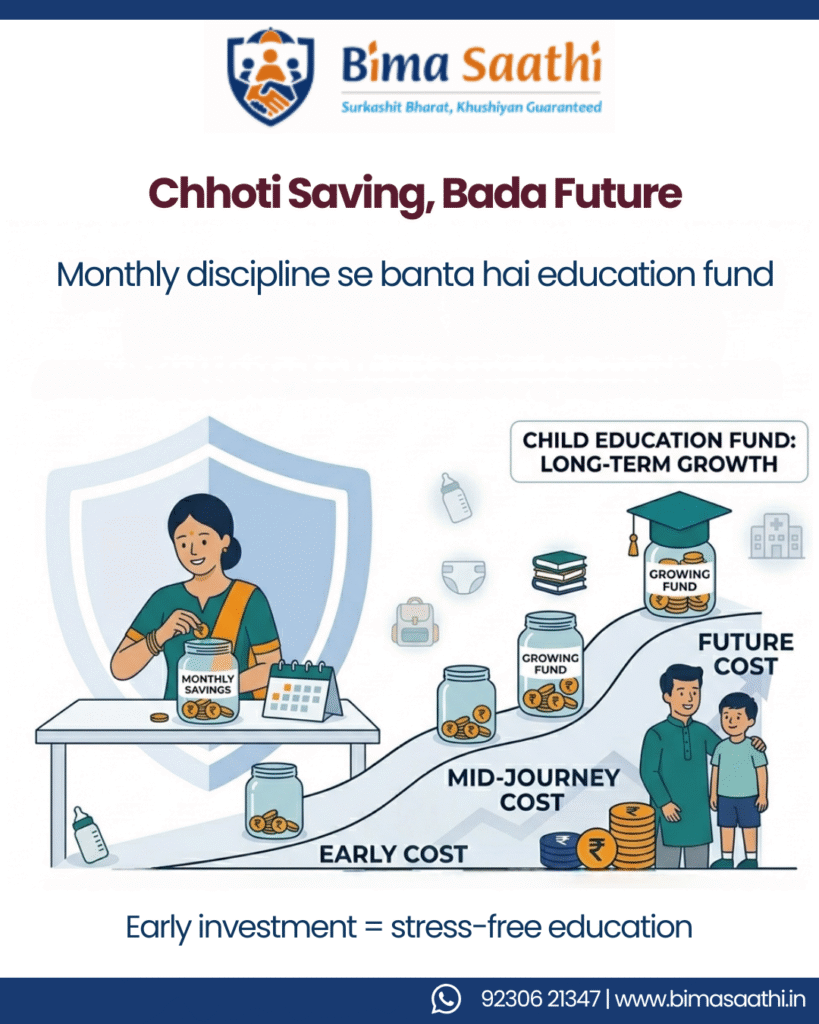

Step 2: Create a Dedicated Child Education Fund (Beat Inflation)

Once your protection is secure, focus on growth.

2.1. Start Early (The Power of Compounding): Even ₹2,000 invested monthly when your child is 1 year old will grow significantly larger than investing ₹10,000 monthly when they are 12 years old.

2.2. Diversify for Growth (Equity SIPs): Since education goals are 15-18 years away, you must invest in inflation-beating assets. Equity Mutual Funds via SIPs (Systematic Investment Plans) are ideal. Historical data suggests they comfortably provide 12-15% long-term returns, beating education inflation.

2.3. Safe Havens (Debt/Government Schemes): Use the Sukanya Samriddhi Account (SSA) for a daughter (excellent returns, tax-free) or Public Provident Fund (PPF) (safe, tax-efficient) for general stability. These provide the ‘debt’ component to your portfolio.

Step 3: Don’t Forget Your Own Retirement

We say it often at Bima Saathi: “Education loans exist; retirement loans do not.” Do not compromise your retirement fund to overfund your child’s goals. If you don’t plan for your retirement, you become a financial burden on your child later. A financially independent parent is the ultimate gift you can give your adult child.

Step 4: The “Audit” and Objection Handling

As young parents, you will face pressure from well-meaning elders to invest only in safe, traditional ways (FDS, Gold). Handle this calmly:

Objection: “SIP risks hai!” (SIP is risky)

Bima Saathi Solution: “Risk tab hai jab 20 saal baad paise inflation se kam honge. SIP short-term risky ho sakti है, long-term safe hai.”

Review your financial plan every year. Expenses change, income grows, and inflation continues.

Common Mistakes Young Parents Make

Let’s call it out honestly. We see these errors every day in our communities. Avoid them at all costs:

❌ “Abhi time hai”

Reality: Time nahi hota. Delay hota hai. The cost of delay is exponential.

❌ “Savings enough hai”

Reality: Savings protection nahi hota. Savings can be wiped out in months. Protection ensures savings continue.

❌ “Insurance mehenga hai”

Reality: Emergency zyada mehenga hota hai. The premium for safety is a fraction of the cost of a crisis.

❌ “Sab online samajh lenge”

Reality: Financial decisions Google se nahi, guidance se aate hain. Your family is unique; generic advice doesn’t apply to them. Talk to a human Saathi.

Final Takeaways: From Pressure to Peace of Mind

Financial planning for young parents isn’t about becoming “rich”; it’s about becoming “Resilient.” It’s about building a fortress around your family that keeps their dignity and dreams intact, no matter how harsh the world outside becomes.

Pehele ‘Suraksha’, Fir ‘Sukh’ (Protection first, then happiness).

Health & Term Insurance is Your Shield. SIPs & Schemes are Your Sword.

Start Early. Even a Small Step is a Giant Leap for Compound Interest.

A financially independent parent is the best safety net a child can have.

Connect with Bima Saathi

Is your current financial portfolio strong enough to protect your child’s dreams against inflation and unpredictable “Interruption”? At Bima Saathi, we specialize in helping young Indian parents like Amit and Vikram design their customized, resilient financial shields and growth plans.

Don’t leave your family’s security to chance or complete optimism. Let’s have that “uncomfortable” conversation today to ensure your child’s tomorrow is comfortably secure.

📞 Call / WhatsApp: +91 92306 21347

📧 Email: support@bimasaathi.in

🌐 Visit: www.bimasaathi.in

Aapke bacche ke har ‘Kal’ ki suraksha humari zimmedari. Bima Saathi – Hamesha aapke saath!

Decision aapka hoga. Saath hum denge

FAQ’s – Frequently Asked Questions

1. Is my corporate health insurance enough after having a baby?

No, corporate covers are usually low (₹3-5 Lakhs) and end if you lose your job. You need a separate, higher Family Floater plan to protect your newborn and family from rising medical costs long-term.

2. How much Term Life Insurance does a young father or mother in India need?

Ideally, you need a sum assured that is 15 to 20 times your total annual income. This ensures your child’s standard of living and future goals are secured even in your absence.

3. When is the best time to start investing for my child’s higher education in India?

The best time is today, or as soon as your child is born. Starting early allows even small monthly amounts to grow significantly over 15-18 years through the power of compounding.

4. Between Gold, FD, and SIPs, what is best for a 15-year education goal?

To beat education inflation (10-12%), you must invest a portion in Equity Mutual Funds via SIPs. Use FDs or Gold only as small, safe components; they cannot be your primary growth engine.

5. Can I add my newborn to my existing health insurance policy immediately?

A: Most Indian policies allow you to add a newborn only after 90 days from birth, unless it is a specialized maternity cover. Contact Bima Saathi or your insurer immediately after birth to understand the exact process and timelines.

Leave A Comment