मुख्य सार

भारत में parent बनना खुशी का एक बड़ा पल होता है, लेकिन इसके साथ financial responsibility भी तेजी से बढ़ती है। Education inflation 10–12% तक पहुँच रही है और healthcare costs भी लगातार बढ़ रहे हैं। ऐसे में सिर्फ traditional saving काफी नहीं है। सही financial planning में protection (insurance), stability और long-term investment शामिल होना चाहिए, ताकि आपके बच्चे का future हर परिस्थिति में सुरक्षित रहे।

Introduction: खुशी, डायपर… और एक सच्चाई

भारत में अपने newborn baby को पहली बार गोद में लेने से बड़ी खुशी शायद ही कोई हो।

छोटे-छोटे हाथ, हल्की सी मुस्कान… सब कुछ magical लगता है।

लेकिन इस खुशी के साथ एक और एहसास आता है—थोड़ा सा डर।

अब आप सिर्फ अपने लिए plan नहीं कर रहे हैं।

अब आपको सोचना है:

- खाना

- घर

- education

- health

- future

अगले 20 साल के लिए।

भारत में जहाँ family expectations और aspirations दोनों high होते हैं, यह जिम्मेदारी और भी बड़ी लगती है।

📊 Estimates के अनुसार:

एक बच्चे को जन्म से 21 साल तक पालने का खर्च ₹60 लाख से ₹1.2 करोड़ तक हो सकता है (metro cities में, higher education को छोड़कर)।

यह blog डराने के लिए नहीं है।

यह आपको empower करने के लिए है।

Bima Saathi का मानना है:

आज का expensive toy नहीं… कल की financial security ही सबसे बड़ा gift है।

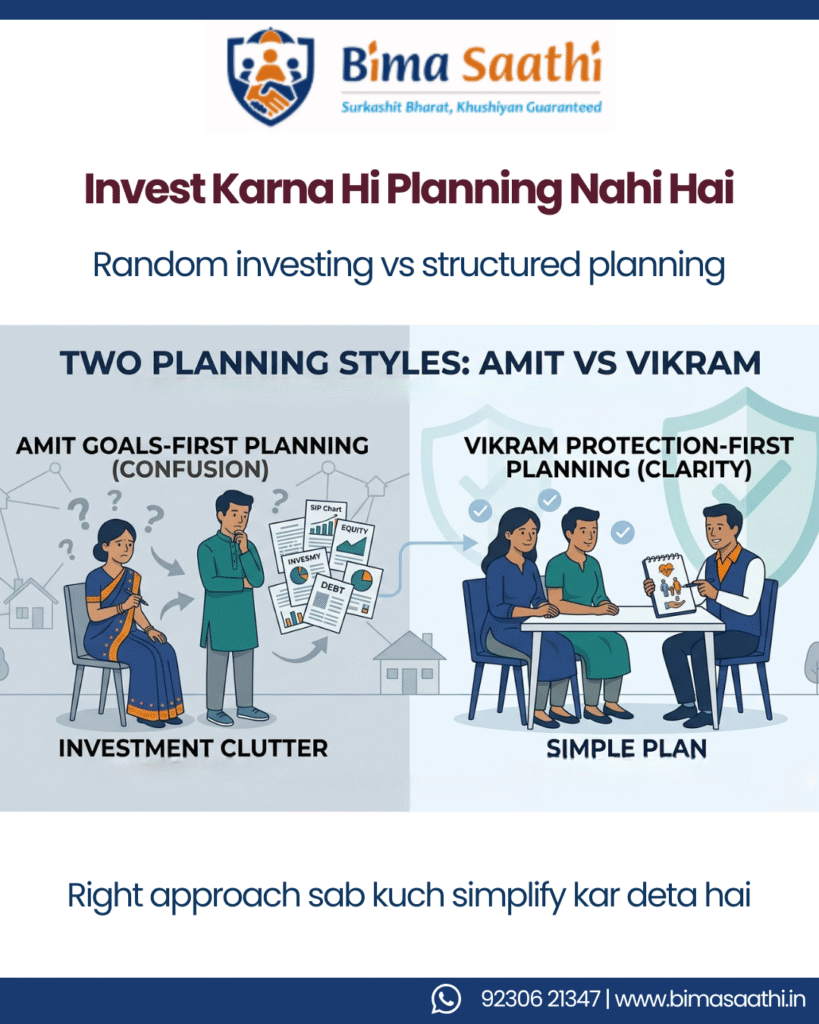

Real-Life Scenario: Planning के दो तरीके

चलिए दो families से मिलते हैं।

Case 1: अमित और प्रिया (Goals-First Planning)

दोनों की उम्र: 28 साल

बेटी: दिया

उन्होंने:

Sukanya Samriddhi Account (SSA) खोला

SIP शुरू किया (₹20,000/month)

लेकिन:

सिर्फ ₹5 लाख का corporate health insurance

कोई term life insurance नहीं

क्यों?

“Insurance में return नहीं मिलता”

Case 2: विक्रम और मेघा (Shield-First Planning)

दोनों की उम्र: 29 साल

बेटा: आर्यन

उन्होंने पहले बनाया:

Protection Shield:

₹10 लाख का family health plan + ₹20 लाख super top-up

Term life insurance + income continuity feature

फिर:

₹10,000/month SIP

Slow start, but strong foundation

Problem: Reality का झटका (Inflation + Risk)

भारत में आम सलाह होती है:

“FD करा लो या gold खरीद लो”

Safe है… लेकिन enough नहीं है।

1. Education Inflation Shock

General inflation: 5–6%

Education inflation: 10–12%

आज ₹10 लाख की degree

15 साल बाद ₹35–40 लाख हो सकती है

अगर आप 7–8% return वाले options में invest कर रहे हैं…

आपका पैसा actually value खो रहा है।

2. Medical Inflation Shock

Healthcare inflation: 12–14%

आज ₹80,000 का delivery cost

कुछ साल में दोगुना

Metro treatment = extra खर्च

₹3–5 लाख का corporate cover risky है।

3. “Uncomfortable Conversation” – Income Loss

अगर earning member को:

- accident

- illness

- disability

कुछ हो जाए…

income रुक सकती है

expenses नहीं रुकते

Result:

school fees रुकती है

EMI default होता है

financial stress बढ़ता है

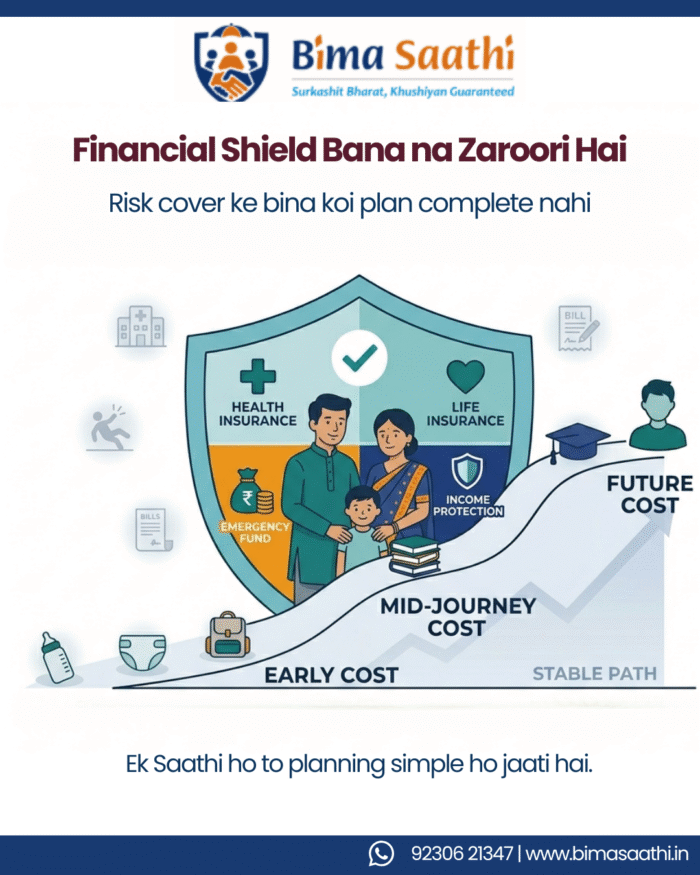

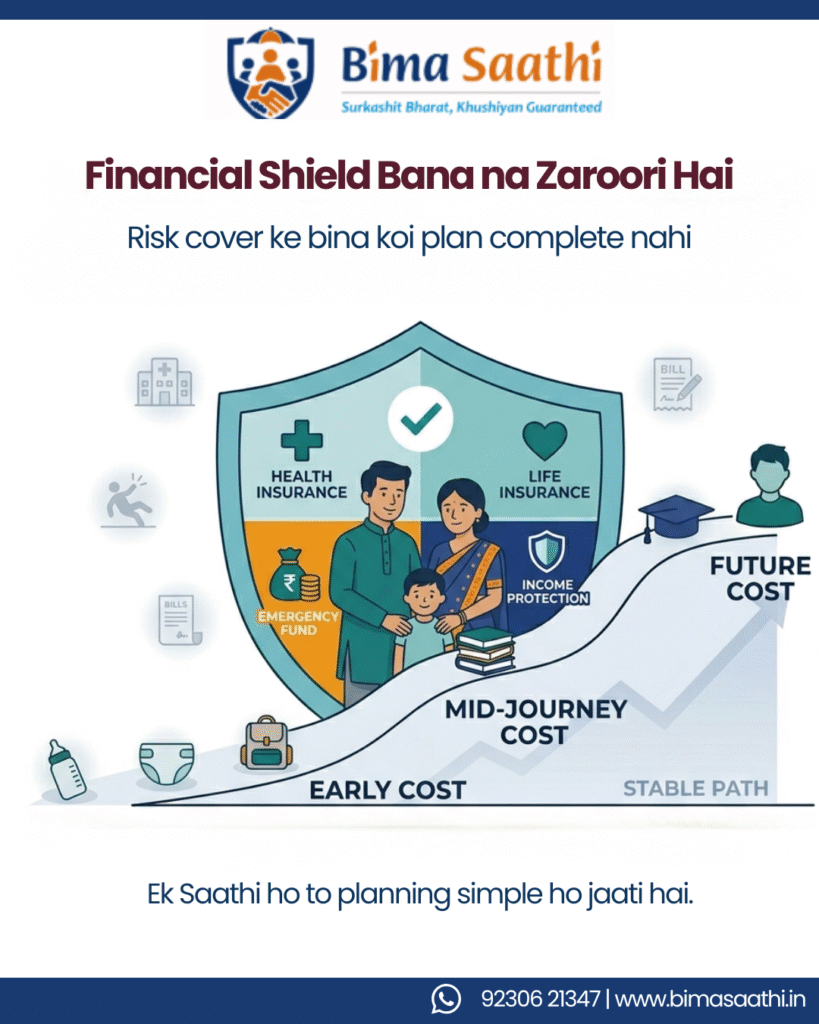

Solutions: Step-by-Step Financial Planning Guide

Step 1: Protection Shield बनाइए (सबसे जरूरी)

1.1 Health Insurance (Medical Shield)

Company policy पर depend मत रहिए

Family floater plan लीजिए

Add करें:

Super top-up (high cover, low cost)

Features देखें:

restoration benefit

cashless hospitals

1.2 Term Life Insurance (Income Protection)

यह “death insurance” नहीं है।

यह family income protection है

Rule:

15–20× annual income

Pro Tip:

Monthly payout option choose करें

क्यों?

Lump sum manage करना मुश्किल होता है।

Monthly income = stability

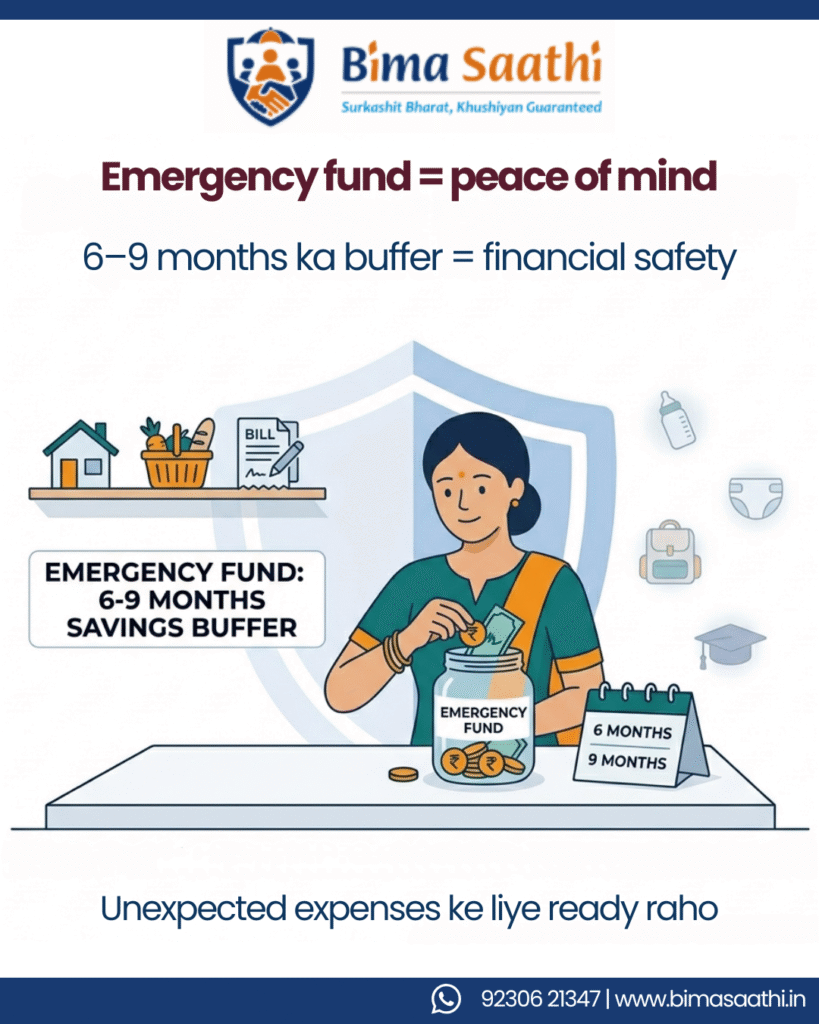

1.3 Emergency Fund (पहली सुरक्षा लाइन)

Simple सवाल:

“Income रुक गई तो क्या होगा?”

6–9 महीने का expense रखें

liquid form में रखें

Example:

₹50,000 monthly expense

₹3–4.5 लाख emergency fund

1.4 Income Protection (Ignored Risk)

Death planning सब करते हैं।

लेकिन:

disability?

temporary income loss?

अगर income रुकी:

खर्च जारी

savings खत्म

stress बढ़ता

Personal accident + critical illness cover जरूरी है

“ज़िंदगी चलती रहती है… पर income कभी भी रुक सकती है।”

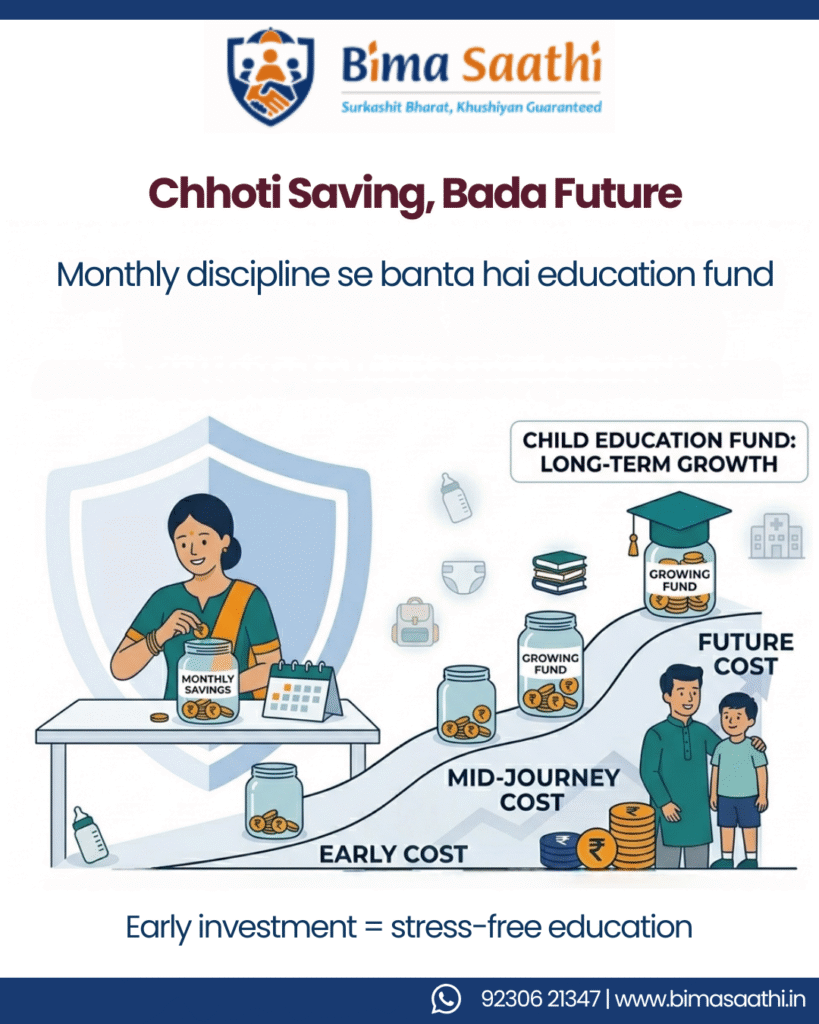

Step 2: Child Education Fund बनाइए

2.1 Early Start (Compounding Power)

₹2,000/month early start

₹10,000/month late start से बेहतर

2.2 Equity SIPs (Growth Engine)

Long-term goal: 15–18 साल

Equity mutual funds best हैं

Expected returns:

12–15% (long-term)

2.3 Safe Options

Sukanya Samriddhi (girls)

PPF

Stability के लिए

Step 3: Retirement मत भूलिए

Important line:

“Education loan मिल जाता है… retirement loan नहीं”

अगर आप plan नहीं करेंगे:

future में child पर burden बनेंगे

Step 4: Plan Review करते रहिए

हर साल check करें:

income

expenses

goals

Common Mistakes Young Parents करते हैं

❌ “अभी time है”

👉 delay costly होता है

❌ “Savings काफी है”

👉 savings खत्म हो सकती है

❌ “Insurance महंगा है”

👉 emergency ज्यादा महंगा है

❌ “Online सब समझ लेंगे”

👉 guidance जरूरी है

Final Takeaways

Financial planning का मतलब rich बनना नहीं है।

resilient बनना है

याद रखें:

पहले Suraksha, फिर Sukh

Insurance = shield

SIP = growth

Start early.

Small step = big future

Financially independent parent = child का best support

Connect with Bima Saathi

क्या आपकी current planning आपके बच्चे के future को सच में protect कर रही है?

Bima Saathi आपकी मदद करता है:

सही protection plan बनाने में

long-term growth strategy बनाने में

आज ही बात करें:

📞 Call / WhatsApp: +91 92306 21347

📧 Email: support@bimasaathi.in

🌐 Website: www.bimasaathi.in

आपके बच्चे के हर “कल” की सुरक्षा हमारी जिम्मेदारी है।

Decision aapka hoga. Saath hum denge. 🤝

FAQs

1. क्या corporate health insurance newborn के लिए enough है?

नहीं। Corporate cover limited होता है और job change होने पर खत्म हो सकता है। Separate family health plan जरूरी है।

2. Young parents को कितना term insurance लेना चाहिए?

कम से कम 15–20 गुना annual income का cover लेना चाहिए।

3. बच्चे की education planning कब शुरू करनी चाहिए?

जितनी जल्दी हो सके, ideally birth के तुरंत बाद।

4. Gold, FD और SIP में क्या बेहतर है?

Long-term goals के लिए SIP बेहतर है। FD और gold सिर्फ support role में रखें।

5. क्या newborn को health insurance में तुरंत add कर सकते हैं?

अधिकतर policies में 90 days के बाद add किया जा सकता है। Exact details के लिए insurer से check करें।

Leave A Comment