Key Summary

In many Indian households, “Joint Financial Planning” is mistakenly limited to sharing a bank account or discussing monthly expenses. Bima Saathi suggests that true joint planning is about building an impregnable, shared safety net that secures both partners’ dignity, health, and income, no matter what life throws at them. This blog moves beyond traditional saving advice to explain why protection (insurance) must be the first step in your combined financial journey, and how robust planning creates mutual respect and lasting financial symmetry.

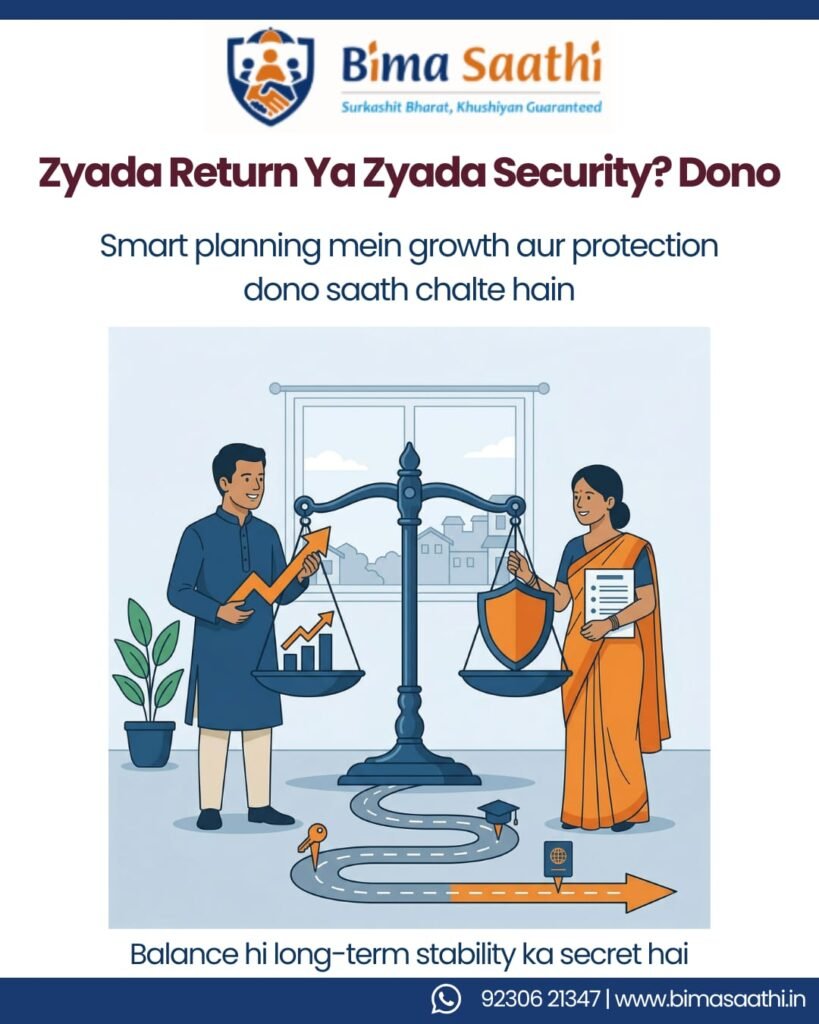

Introduction: The “Shared Dreams, Silent Risks” Paradox

When two people get married in India, it is more than just a union of hearts; it is a merger of financial lives. We happily discuss our “Shared Dreams”: “Kab ghar lenge?” (When will we buy a house?), “Bacche kab honge?” (When will we have children?), and more…

We save for these moments with great enthusiasm. We open recurring deposits and track our gold investments.

But closely following these shared dreams are “Silent Risks” that most Indian couples fail to discuss jointly. Very few sit down together to ask the “Uncomfortable Conversations” about the “What if I can’t work tomorrow?” or “What if one of us faces a medical crisis?”

We often leave these protective decisions to the earning member, usually the husband, assuming that as long as money is being saved, the family is safe.

Pehle ‘Suraksha’, fir ‘Sukh’!”

At Bima Saathi, we believe that the foundation of modern, resilient joint financial planning isn’t just about investing together; it’s about Protecting Together First. Let’s explore why this gap is real and dangerous.

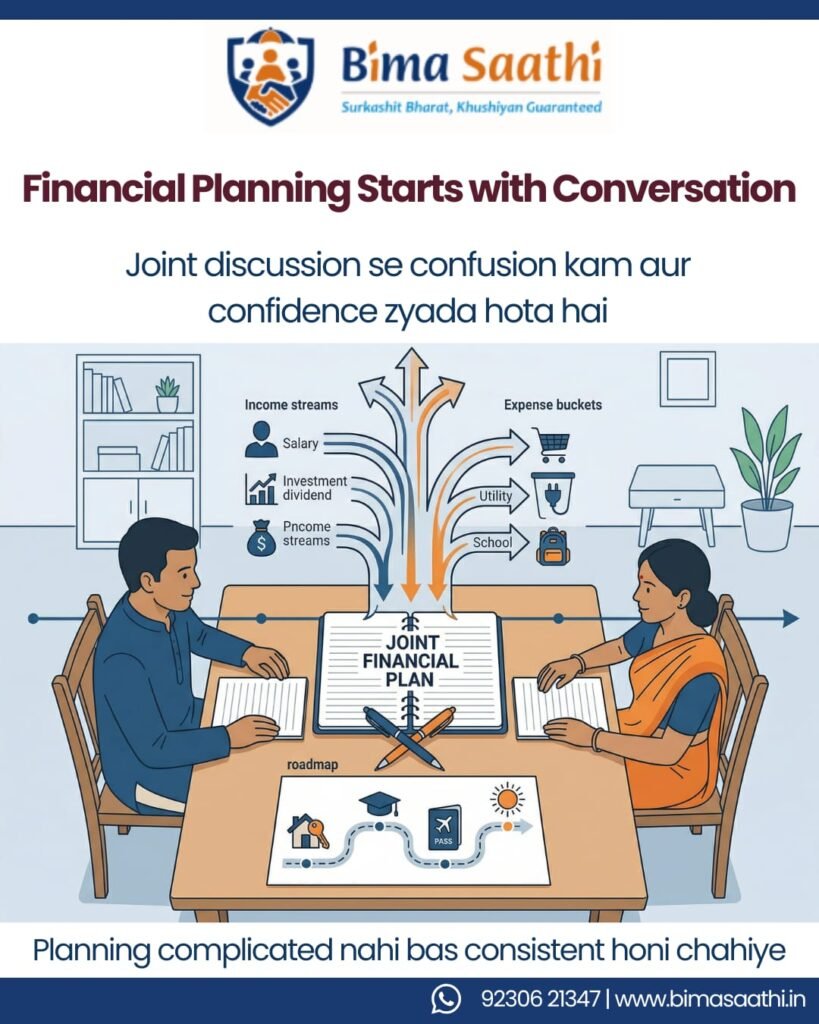

What is Joint Financial Planning for Husband and Wife?

Joint financial planning ka matlab hai ki husband aur wife dono milkar financial decisions lein, samjhein aur track karein.

Isme include hota hai:

- Income understanding: Dono ko pata ho total household income kya hai

- Expense planning: Fixed aur variable expenses clearly defined ho

- Savings aur investments: Goals ke according allocate kiye jayein

- Insurance coverage: Dono ka adequate protection ho

- Future planning: Short-term aur long-term goals aligned ho

Is process ka core hai: transparency + shared responsibility

Why Joint Financial Planning is Important

1. Better Decision-Making

Jab dono partners involve hote hain, toh decision-making balanced hoti hai.

Ek partner risk-oriented ho sakta hai, dusra stability prefer karta hai — dono milkar better outcome create karte hain.

Studies suggest ki households jahan joint decisions liye jate hain, wahan long-term financial stability higher hoti hai.

“Ek ka decision fast hota hai… dono ka decision strong hota hai.”

2. Financial Transparency

Agar financial information shared nahi hai, toh trust issues aur confusion create ho sakta hai.

Joint planning ensure karta hai:

- Sab accounts aur policies visible ho

- Koi hidden liability na ho

- Clarity ho ki paisa kahan ja raha hai

Transparency se unnecessary conflicts bhi kam hote hain.

“Jahan clarity hoti hai, wahan unnecessary tension nahi hota.”

3. Emergency Readiness

India mein ek common problem hai:

Sirf ek insaan ko financial details pata hoti hain.

Agar emergency aa jaye:

- Doosre partner ko policies ka pata nahi hota

- Claim process delay hota hai

- Stress multiply ho jata hai

Joint awareness ensure karta hai ki kisi bhi situation mein dono ready hain.

“Information share nahi hai, toh planning half hai.”

4. Long-Term Goal Alignment

Family goals jaise:

- Bachon ki education

- Ghar kharidna

- Retirement

Agar dono aligned nahi hain, toh:

- Savings mismatch ho jata hai

- Goals delay hote hain

- Frustration build hota hai

Joint planning ensures ki dono same direction mein kaam kar rahe hain.

“Direction same ho, toh speed matter nahi karti.”

Reality Check: Financial Awareness Gap in Couples

India mein financial awareness gap clearly dikhta hai:

- ~70% households mein financial decisions ek hi partner leta hai

- <25% women insurance decisions mein actively involved hoti hain

- Bahut cases mein wives ko policy details ya nominee structure tak nahi pata hota

Yeh gap long-term risk create karta hai.

👉 Related read:

Why Every Woman Should Understand Insurance

https://bimasaathi.in/why-every-woman-should-understand-insurance/

The Problem: The Inevitable “Interrupt” and the Collapse of Dignity

Optimism is a great virtue, but in finance, Optimism Bias (believing bad things won’t happen to you) is dangerous. Your income is your family’s oxygen. You must ensure it never stops. To learn more about how to shield your family responsibly, read our detailed guide on Protecting the “Earning Years”: Disability and the Loss of Income Gap.

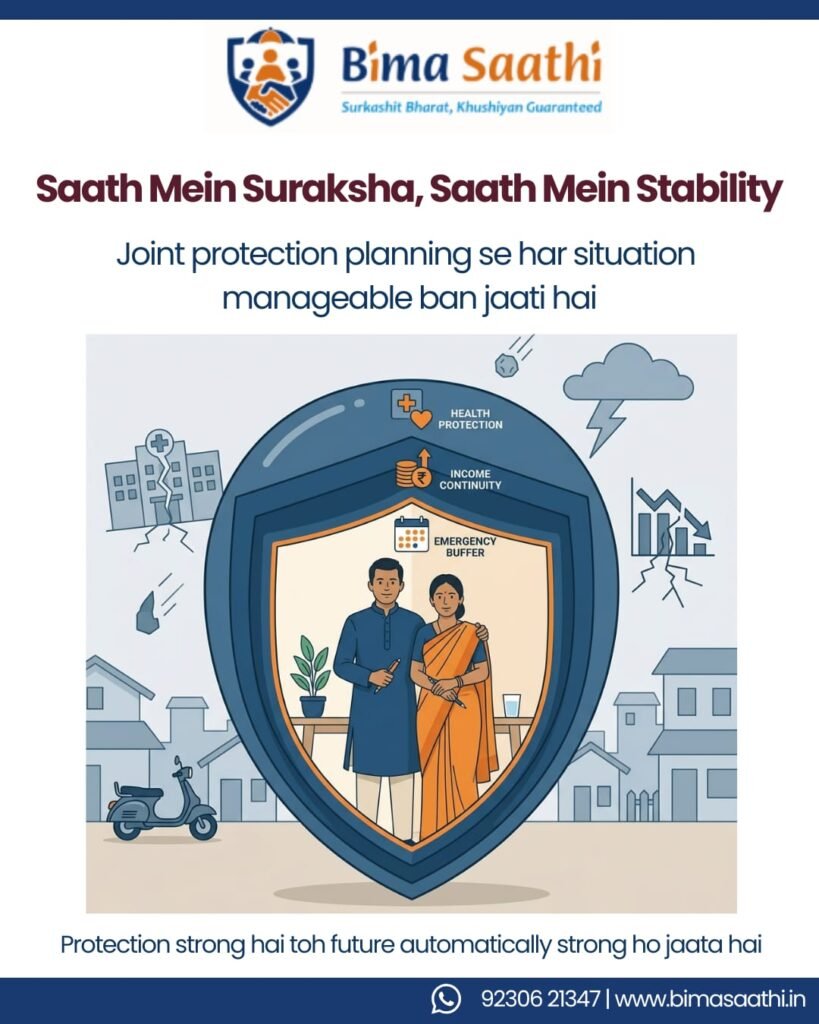

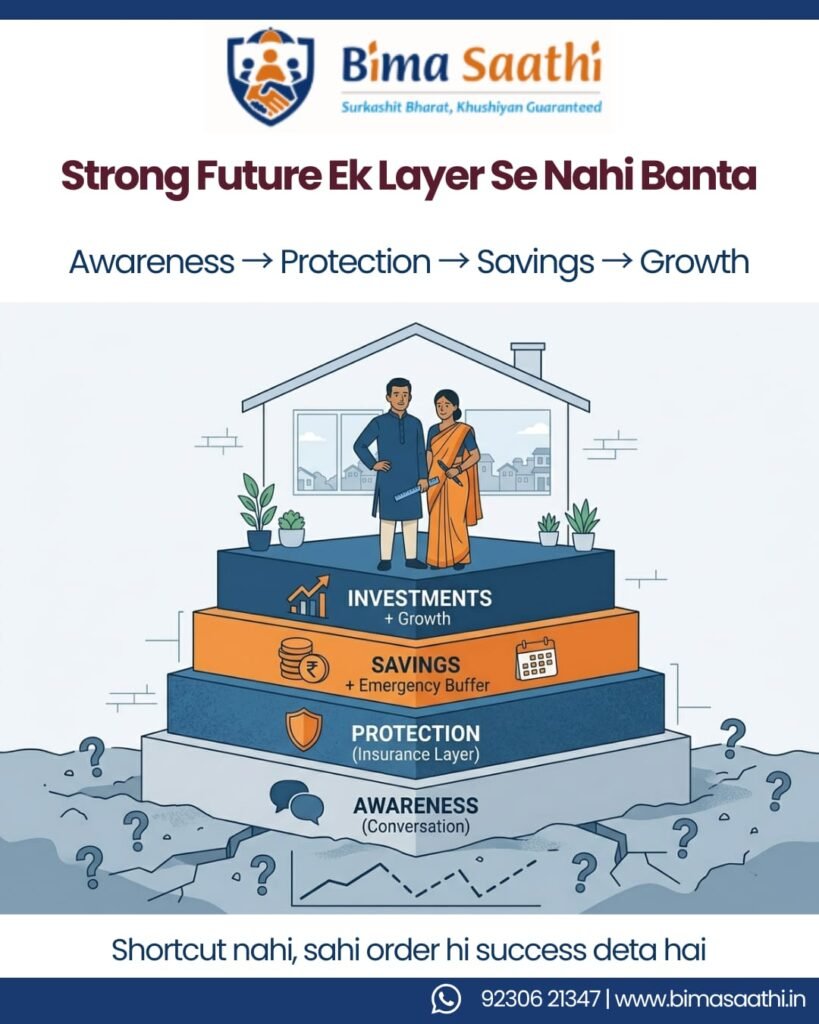

Solutions: The Bima Saathi Blueprint for Joint Resilience

True joint financial wellness is built in layers, starting with awareness and protection first.

Step 1: Open Financial Conversation

Ek simple baat se start karein:

- Total income kya hai

- Monthly expenses kya hain

Important: Yeh discussion judgement-free hona chahiye.

Step 2: Immediately Build Your “Protection Shield”

Before you invest for the future, protect the present. Pehele ‘Suraksha’, fir ‘Sukh’ (Protection first, then happiness).

2.1. Robust Insurance (The Emergency Shock Absorber):

Medical inflation in India is moving at 12-14% annually. Reliance only on a partner’s or company cover is reckless. A Hospital Bill can Vanish your Saving: Why Health Insurance Matters. Secure a standalone Family Floater Plan + Super Top-up. Look for plans with Restoration Benefit, which reloads your cover if you use it up. Add specific Women’s Critical Illness Riders.

2.2. Pure Term Life Insurance (The Income Continuity Shield):

If the main earner passes away or faces Permanent Total Disability, the family faces the double blow of lost income and rising expenses. Your Sum Assured should be 15-20 times your annual income. A Term Plan with an Income Payout option acts as a “replacement salary,” ensuring your family’s dignity and future goals are comfortably secure.

2.3. Specific Women’s Critical Illness Payout:

Understanding insurance is crucial for women, especially in Tier-2 and Tier-3 cities. We must move beyond the “locker mentality” (relying only on physical gold) and understand pure protection. Why Every Woman Should Understand Insurance. Dedicated Women’s Critical Illness riders pay a lump sum upon diagnosis (Cervical Cancer, Breast Cancer), allowing women Dignity in Recovery without touching family gold.

Step 3: Goal Identification and Diversified Growth

Only after Step 1 is secure should you focus on investing for growth.

3.1. Beat Education Inflation for Child Goals:

General inflation is 5-6%, but education inflation is closer to 10-12% annually. You must invest in inflation-beating assets like Equity Mutual Fund SIPs for these long-term goals. SSA/PPF can act as a safe haven. To learn how to secure your child responsibly, read our detailed guide on Financial Planning for Young Parents in India: Securing Your Child’s Dreams from Day One.

3.2. Dedicated Retirement Corpus:

“Education loans existence mein hain, par retirement loans exist nahi karte.” Do not compromise your retirement fund to overfund your child’s goals. A financially independent parent is the ultimate gift you can give your adult child later.

Step 4: Build Emergency Fund

Experts recommend karte hain:

6–9 months ke expenses ka emergency fund

Example:

Monthly expense ₹50,000

Emergency fund = ₹3–4.5 lakh

Yeh buffer unexpected situations handle karta hai bina savings todhe.

Step 5: Responsibility Assign Karein (Knowledge Share Karein)

Roles divide ho sakte hain:

- Ek investments handle kare

- Dusra expense tracking kare

Lekin dono ko overall understanding honi chahiye.

Step 6: Monthly Review System

Har mahine 20–30 minutes ka review karein:

- Budget check

- Savings track

- Goal progress

Consistency planning ko effective banati hai.

“Jo review hota hai wahi improve hota hai.”

Final Thoughts: Strong Relationship = Strong Financial System

Shaadi sirf emotional bond nahi hai

👉 Yeh financial partnership bhi hai

Strong system ke pillars:

- Transparency

- Awareness

- Planning

“Future secure karna hai… toh planning saath mein karni padegi.”

FAQs

- What is joint financial planning for husband and wife?

Joint financial planning means both partners managing income, expenses, and investments together. - Why is joint financial planning important?

It improves transparency, reduces risk, and ensures better financial decisions. - How can couples start financial planning together?

They can start by discussing income, expenses, and setting common goals. - What role does insurance play in joint planning?

Insurance protects savings and provides financial support during emergencies. - Can couples earn together as POSP advisors?

Yes, couples can build a flexible and trust-based income as POSP advisors.

Connect with BIMA SAATHI

Ek simple sawaal:

“Aap planning alag-alag kar rahe hain… ya saath mein?”

Agar aap:

- Joint financial planning start karna chahte hain

- Insurance samajhna chahte hain

- POSP opportunity explore karna chahte hain

BIMA SAATHI aapke saath hai.

Pehle samjhana. Phir margdarshan karna.

📞 Call / WhatsApp: +91 92306 21347

📧 Email: support@bimasaathi.in

🌐 Visit: https://bimasaathi.in/

Decision aapka hoga. Saath hum denge. 🤝

Leave A Comment