Key Summary

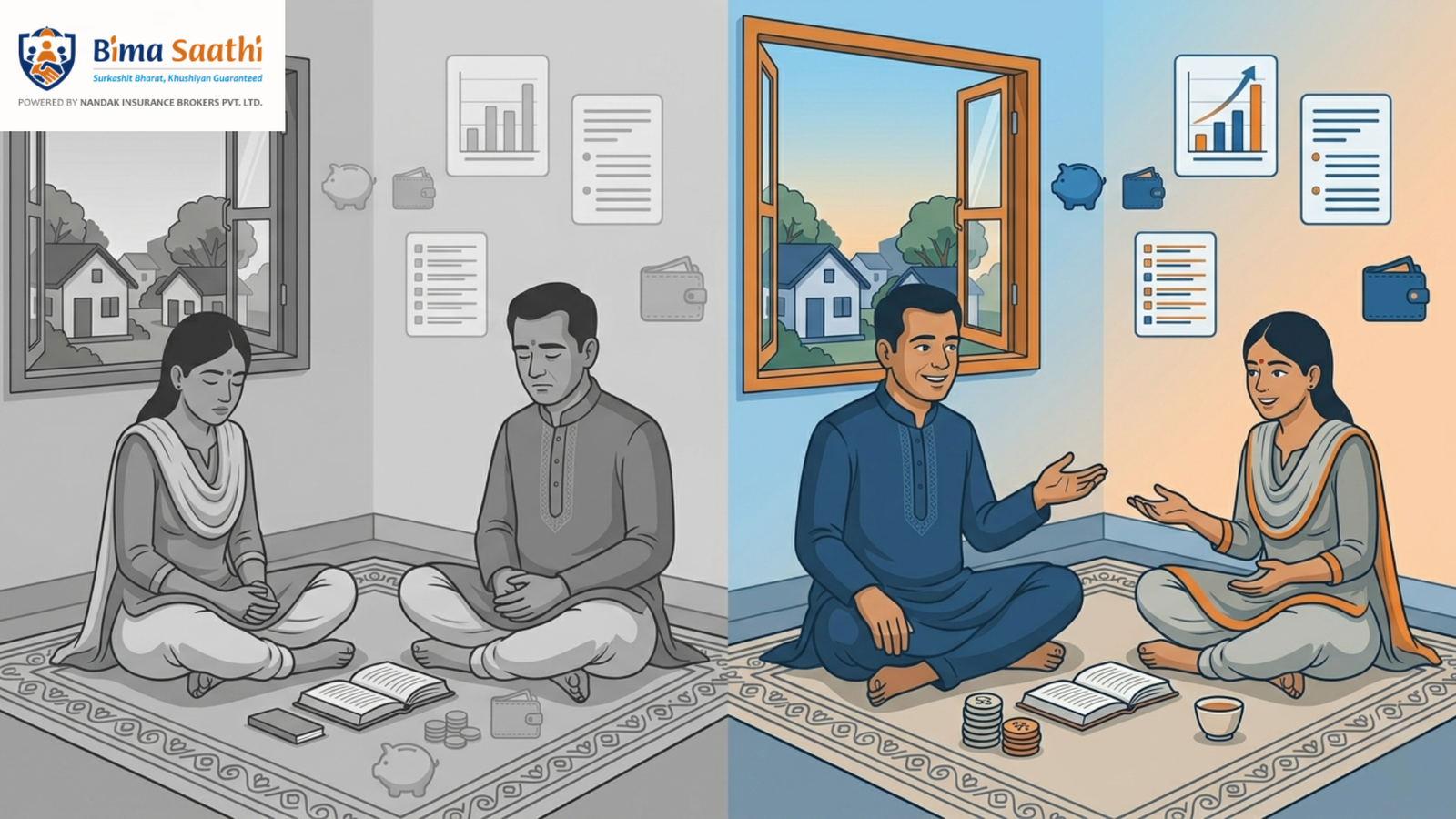

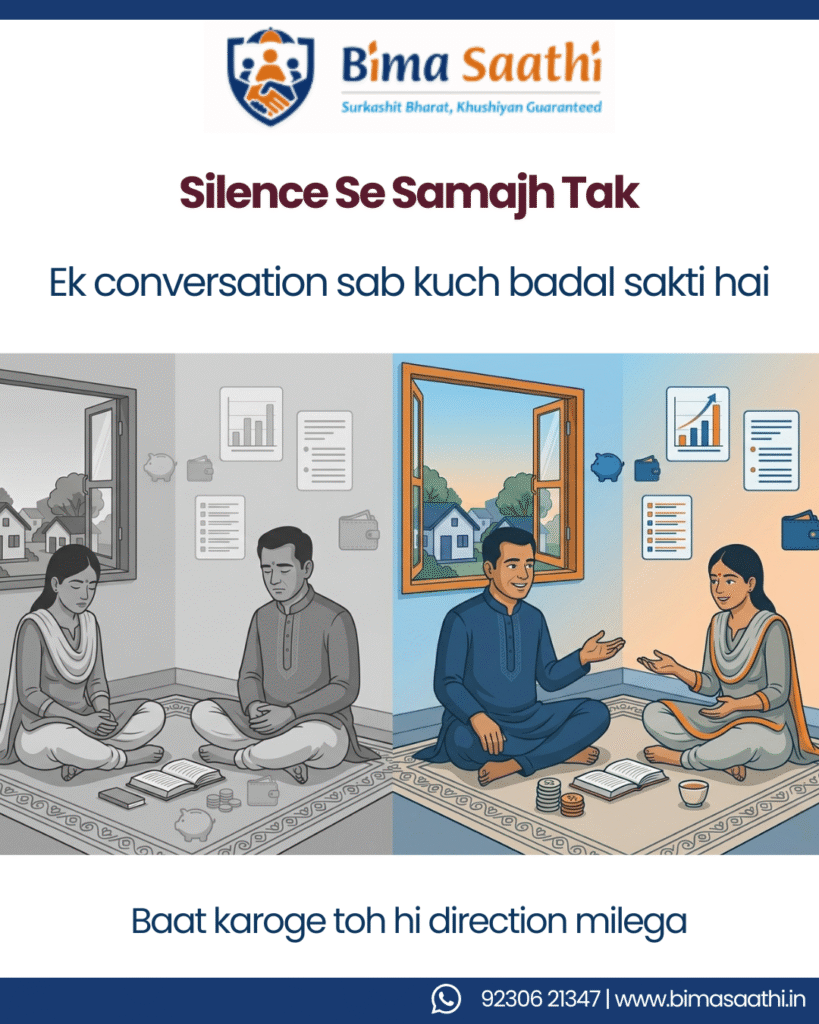

In the average Indian household, certain topics are traditionally considered “off-limits” at the dinner table. While conversations around politics, cricket, and even neighborhood gossip flow freely, a heavy silence usually descends the moment someone asks, “How much do we actually have in savings?” or “What happens to the house if the breadwinner is no longer there?”

Money is the lifeblood of a family’s security, yet it remains the ultimate taboo. At Bima Saathi, we’ve observed that the families who struggle the most during a crisis aren’t necessarily those with the least income they are those with the least communication. Avoiding the money talk doesn’t make financial problems go away; it simply ensures that when they arrive, the family is caught completely off-guard.

- The Cultural Barrier: In India, talking about money is often equated with being “greedy” or “distrustful” of elders.

- The Fear Factor: Parents often hide financial struggles to “protect” their children, unintentionally leaving them ill-prepared for adulthood.

- The Literacy Gap: Many family members avoid the topic because they feel they don’t understand complex financial jargon.

- The Protection Risk: Silence leads to misplaced documents, unknown nominees, and a massive Protection Gap during medical or life emergencies.

- The Bima Saathi Solution: Moving from “Secretive Saving” to “Transparent Protection” through family-inclusive financial planning.

Introduction: The Elephant in the Living Room

Why is it easier to talk about a terminal illness than it is to talk about a Term Insurance policy? Money is deeply tied to our sense of worth, power, and security. For a father, admitting he hasn’t saved enough for a daughter’s wedding feels like an admission of failure. For a spouse, asking about bank locker keys feels like they are “anticipating” a tragedy.

In 2026, the financial world has become exponentially more complex. With digital assets, multiple insurance riders, and shifting tax laws, the old “one person knows everything” model is dangerous. When families avoid talking about money, they aren’t just avoiding numbers; they are avoiding the reality of their own vulnerability. This silence is the single greatest hurdle to achieving true financial freedom.

The 5 Psychological Walls Stopping Money Conversations

- The “Respect + Silence” Paradox

Indian households mein ek subtle rule hota hai:

👉 “Bade jo kar rahe hain, woh sahi hi hoga.”

Bachpan se sikhaya jaata hai ki parents ke financial decisions question karna = disrespect. Result? “Papa dekh lenge” mindset develop ho jaata hai. Bachche grow up hote hain without ever understanding how money actually works—budget kya hota hai, EMI ka impact kya hota hai, ya savings ka structure kya hai.

Problem yahan start hoti hai:

Jab yeh bachche earning start karte hain, unke paas income hoti hai—but system nahi hota. They become financially dependent on guesswork. Respect ke naam pe silence ne unhe decision-making se door rakha.

- Fear of Conflict + Emotional Trigger

Money discussions logically nahi, emotionally react karte hain.

👉 Ego hurt ho sakta hai

👉 Spending habits judge ho sakte hain

👉 “Tum zyada kharch karte ho” type arguments trigger ho jaate hain

Isliye couples aur families consciously avoid karte hain.

PwC India ke according:

👉 ~60% couples uncomfortable feel karte hain finances discuss karne mein

Aur phir kya hota hai?

- Hidden expenses

- Secret credit cards

- अलग-अलग financial lives

Isse ek concept emerge hota hai: Financial Infidelity jab partners financial cheezein chhupate hain to avoid fights.

Short term mein peace milta hai…

Long term mein trust crack ho jaata hai.

“Jhagda avoid karne ke chakkar mein problem grow ho jaati hai.”

- “Log Kya Kahenge” + Social Comparison Trap

India mein financial reality se zyada financial image important ban jaati hai.

- “Unhone car le li”

- “Unka house ho gaya”

- “Unka lifestyle better hai”

Result?

👉 Log apni asli situation hide karte hain

👉 Loans disclose nahi karte

👉 Financial stress share nahi karte

Even within family:

- Income secret

- Debt hidden

- Pressure internal

Yeh comparison-driven silence dangerous hai, kyunki decisions reality pe nahi, perception pe liye jaate hain.

- Complexity + Shame Barrier

Financial world intimidating lagta hai:

- GST

- CAGR

- SIP

- HLV

- Riders

Agar kisi ko samajh nahi aata, woh poochta kyun nahi?

👉 Kyunki “stupid” lagne ka darr hota hai

Isliye log chup rehte hain.

Chup rehne se kya hota hai?

👉 Learning ruk jaati hai

👉 गलत decisions continue hote hain

SEBI data:

👉 Only ~27% Indians financially literate

Matlab majority log samajhte nahi…

Aur poochte bhi nahi.

“Samajh na aana problem nahi poochna band kar dena problem hai.”

- Privacy vs Secrecy Trap

Privacy healthy hoti hai.

Secrecy dangerous hoti hai.

Kaafi breadwinners yeh believe karte hain:

👉 “Income private hai”

👉 “Bachchon ko pata chala toh irresponsible ho jayenge”

👉 “Family ko pata chala toh expectations badh jayengi”

Result:

- Spouse ko full picture nahi pata

- Children unaware rehte hain

- Financial dependency create hoti hai

Worst-case scenario:

Agar primary earner ko kuch ho jaata hai

👉 Family ko pata hi nahi hota ki assets kahan hain, policies kya hain

Yeh silence risk create karta hai.

Real-Life Examples: The Cost of Silence

Scenario A: The “Hidden Debt” Disaster

Rajesh was a successful businessman who always provided a lavish lifestyle for his family. He never discussed his business loans or the fact that his life insurance had lapsed. When he suffered a sudden cardiac arrest, his wife and children were shocked to find that the family home was mortgaged. Because they were never part of the “money talk,” they had no plan to manage the creditors and eventually lost their home.

- The Cause: Protective silence.

- The Result: Total loss of security.

Scenario B: The “Lost Assets” Syndrome

Mrs. Kapoor had invested in several physical gold bonds and fixed deposits over thirty years. She kept the receipts in a “safe place” but never told her children where. After she passed away from old age, her children spent years running from bank to bank, unable to claim their rightful inheritance because they didn’t have the account numbers or know which branches held the deposits.

- The Cause: Lack of an organized family “Wealth Map.”

- The Result: Wealth remained “locked” and useless when needed most.

The Problem: What Happens When You Stay Silent?

The “Money Silence” leads to three major structural problems:

- The Nominee Nightmare: Thousands of crores of rupees lie unclaimed in Indian banks and insurance companies. Why? Because the nominees were never informed that a policy existed, or the nomination was never updated after marriage or childbirth.

- The Under-Insurance Gap: Without family discussion, the breadwinner often buys a “standard” policy that doesn’t actually cover the family’s real needs. If the spouse doesn’t know the household’s monthly expenses, they can’t help determine if a ₹50 Lakh cover is enough or if it needs to be ₹2 Crore.

- Emergency Panic: In a medical emergency, the last thing you want to be doing is searching for a TPA card or checking if the hospital is in the insurer’s network. Silence ensures that the family doesn’t know the “Emergency Protocol.”

How to Start Money Conversations (Simple, Practical & Stress-Free)

Solution complicated nahi hai.

Problem awareness ki nahi approach ki hoti hai.

Agar approach sahi ho, toh difficult conversation bhi natural lagti hai.

- Start Small, But Start Consistently

Most log wait karte hain “perfect time” ka.

Reality: woh time kabhi aata hi nahi.

Instead:

- Weekly ya fortnightly 10-minute conversation start karein

- Basic topics se shuru karein:

- Monthly expenses

- Upcoming payments

- Small savings

Goal yeh nahi hai ki sab solve ho jaaye

👉 Goal hai comfort build karna

- Use Real-Life Context, Not Theory

Financial jargon sunte hi log disconnect ho jaate hain.

Isliye theory nahi – real life se baat karein.

Examples:

- “Is mahine ₹5,000 kahan spend hua?”

- “Agar emergency aaye toh kya plan hai?”

- “Agla goal kya hai—travel ya savings?”

Isse:

- Conversation practical hoti hai

- Participation natural ho jaata hai

“Numbers tab samajh aate hain jab woh life se connect hote hain.”

- Shift the Frame: From Money to Responsibility

Direct “paise ki baat karte hain” bolna uncomfortable lagta hai.

Isko reframe karein:

👉 “Main ensure karna chahta hoon ki family safe rahe, no matter what.”

👉 “Chalo apna safety system set karte hain.”

Yeh shift powerful hai:

- Money → emotional topic

- Responsibility → shared purpose

- Create a No-Judgement Zone

Sabse bada blocker kya hota hai?

👉 Fear of judgement

Agar conversation mein yeh feel aaye:

- “Tum zyada kharch karte ho”

- “Tumhe samajh nahi hai”

👉 Conversation immediately बंद हो जाती है

Rule simple hai:

✔ No blame

✔ No comparison

✔ Only clarity

“Conversation tab grow karti hai jab ego side mein hota hai.”

- Make It a Family Ritual (Low Pressure, High Clarity)

Money talk ko serious meeting mat banao.

Usse ritual bana do.

Example:

👉 “Family Financial Friday” (monthly ya quarterly)

Ismein:

- Insurance documents ka location share karo

- Emergency contacts discuss karo

- Basic updates share karo

Environment:

- Casual

- Relaxed

- Open

- Make Planning a Shared Activity (Not One Person’s Job)

Often ek hi person financial decisions leta hai.

Baaki log disconnected rehte hain.

Isko change karein:

👉 Partner ke saath बैठकर discuss करें:

- Monthly needs

- Future goals

- अगर income रुक जाए तो क्या होगा

- Simplify Language (Jargon-Free Conversations)

CAGR, HLV, Riders

yeh sab sunke log disconnect ho jaate hain.

Instead:

- Simple Hinglish use karein

- Analogies use karein

Example:

👉 Insurance = umbrella

👉 Emergency fund = safety cushion

- Document Everything (Clarity Beyond Conversation)

Conversation ka next step kya hai?

👉 Documentation

Ek Master File (physical ya digital) banayein:

Include:

- Insurance policy copies

- Bank account details

- Nominee list

- Advisor / CA contact

Why this matters:

👉 Emergency mein confusion nahi hota

👉 Family dependent nahi rehti

“Jo likha hota hai… wahi kaam aata hai.”

Role of POSPs: Conversation Starters

POSPs ka real role:

👉 Awareness build karna

👉 Conversations start karna

Aap:

✔ Complex concepts simplify karte ho

✔ Families ko educate karte ho

✔ Trust build karte ho

📚 Learn Before You Speak

👉 Why Every Woman Should Understand Insurance

https://bimasaathi.in/why-every-woman-should-understand-insurance/

👉 Short-Term Happiness vs Long-Term Security: The Real Trade-Off

https://bimasaathi.in/short-term-happiness-vs-long-term-security-the-real-trade-off/

👉 Income Protection & Human Life Value

https://bimasaathi.in/income-protection-the-foundation-of-financial-stability/

Final Thought: Silence Se Stability Nahi Aati

At Bima Saathi, we believe that Financial Literacy starts at home. You don’t need a finance degree to protect your family; you just need the courage to be transparent. Talking about money is the highest form of caring. It ensures that your hard-earned wealth actually serves its purpose providing peace of mind to the people you love most.

Don’t wait for a crisis to start the conversation. Start it today, when things are calm, and everyone can think clearly. Remember, a plan that only one person knows is not a plan it’s a secret. And secrets are the enemies of security.

Saathi Ke Saath Financial Conversations Shuru Karein

Agar aap:

- Financial awareness build karna chahte ho

- POSP opportunity explore karna chahte ho

- Logon ko guide karna chahte ho

👉 BIMA SAATHI aapke saath hai samjhane ke liye, bechne ke liye nahi

📞 Call / WhatsApp: +91 92306 21347

📧 Email: support@bimasaathi.in

🌐 Website: https://bimasaathi.in/

Decision aapka hoga. Saath hum denge. 🤝

FAQs

1. Why do families avoid talking about money?

Families avoid talking about money due to discomfort, lack of awareness, and fear of conflict.

2. Is it important to discuss finances in a family?

Yes, discussing finances helps in better planning, reducing conflicts, and building financial security.

3. What problems arise when families don’t talk about money?

It leads to poor planning, hidden debts, lack of savings, and financial stress.

4. How can families start financial conversations?

They can start with small discussions, avoid judgement, and focus on simple topics.

5. How can POSPs help families improve financial awareness?

POSPs can simplify financial concepts, build trust, and guide families toward better decisions.

Leave A Comment