In the whirlwind of modern life, where professional ambitions and lifestyle aspirations often take center stage, the bedrock of our existence remains our family. We work, save, and invest primarily to ensure that the people we love are comfortable, safe, and provided for. However, “hoping” for the best is not a financial strategy. Family First Finance is a philosophy that shifts the focus from mere wealth accumulation to intentional, protection-oriented financial planning.

At Bima Saathi, we believe that true financial freedom isn’t about how much you earn; it’s about how well you protect what you have and how effectively you prepare for the “what ifs.” This guide explores a practical, step-by-step approach to putting your family first in every financial decision you make.

Key Summary

Family First Finance is a holistic strategy designed to prioritize the security and well-being of the household over speculative gains. It involves identifying the unique needs of every family member from aging parents to growing children and building a “financial fortress” around them. This approach focuses on high-liquidity emergency funds, comprehensive health coverage, life protection, and goal-based investing. By shifting the perspective from “individual wealth” to “family resilience,” you ensure that your loved ones remain stable regardless of economic cycles or personal setbacks.

Introduction: Why We Need a “Family First” Lens

Most financial advice is generic. It tells you to “invest in the stock market” or “diversify your portfolio.” While that advice isn’t wrong, it often overlooks the emotional and practical nuances of a family unit. For a young professional in London or a growing family in Mumbai, financial planning isn’t just about numbers on a screen; it’s about the school fees next year, the medical bills for a parent, or the mortgage on a forever home.

A “Family First” approach means that every rupee or dollar spent or invested is evaluated against one question: “How does this strengthen my family’s future?” It’s a transition from being a passive saver to an active protector.

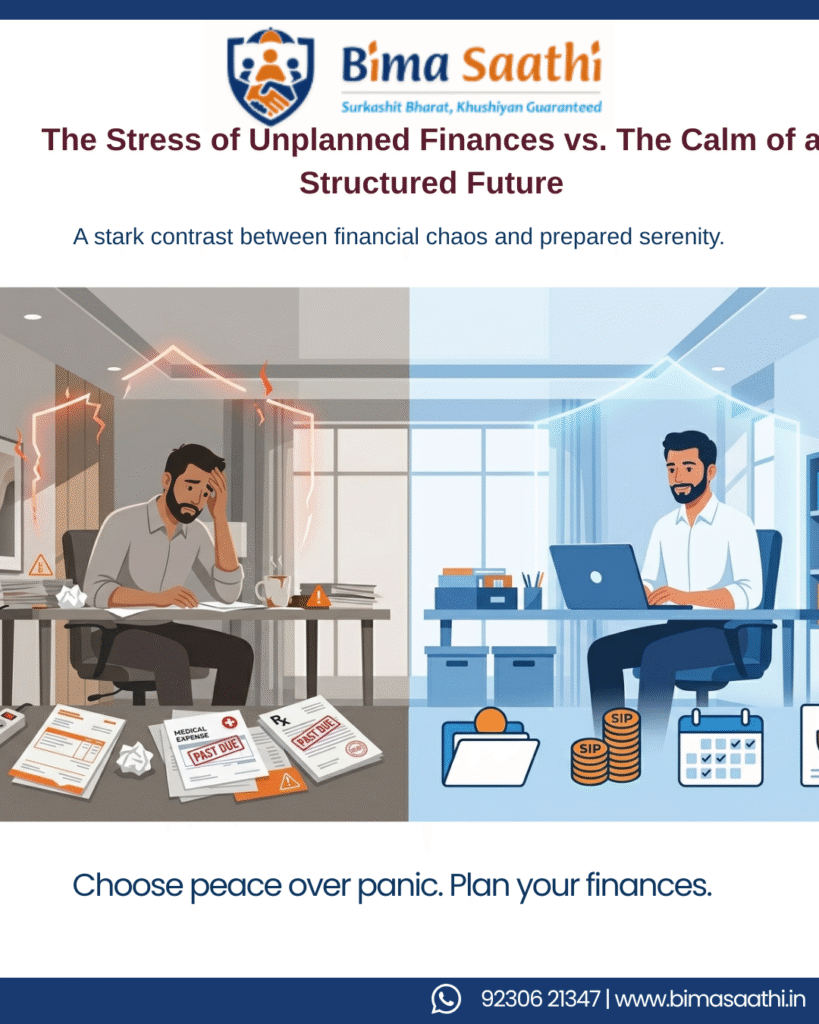

The Core Problem: The Fragility of Modern Household Finances

Many families today live in a state of “perceived stability.” They have steady incomes and some savings, but they are often just one major event away from a financial crisis. Common pitfalls include:

1. The Single-Income Trap: Families relying on one breadwinner without adequate life or disability insurance.

2. Medical Debt Inflation: As healthcare costs rise, a single hospital stay can wipe out years of savings if the family is under-insured.

3. Lifestyle Creep: Increasing expenses as income rises, leaving little room for a “safety net.”

4. Lack of Liquidity: Having assets tied up in real estate or long-term lock-in investments when cash is needed for an emergency.

Without a practical framework, families often find themselves reacting to crises rather than preventing them.

A Practical Framework for Family First Finance

To implement this approach, we must look at financial planning as a pyramid, with protection at the base and growth at the top.

1. Building the Foundation: The Protective Layer

Before you think about the stock market, you must secure the “Base.”

• Term Life Insurance: This is the ultimate “Family First” tool. It isn’t an investment; it’s a replacement for your economic value. At Bima Saathi, we emphasize that a Term Plan should cover at least 10-15 times your annual income plus any outstanding debts.

• Comprehensive Health Cover: Employer-provided health insurance is rarely enough. A dedicated family floater plan ensures that your parents, spouse, and children have access to the best medical care without depleting your bank account.

2. The “Sleep Well at Night” (SWAN) Fund

A practical approach requires an emergency fund that covers 6 to 12 months of family expenses. This shouldn’t be in a volatile market. It belongs in a high-yield savings account or a liquid fund. This fund is your family’s shock absorber against job loss or unexpected repairs.

3. Goal-Based Investing: Education and Beyond

Stop investing “randomly.” Instead, tag your investments to specific family milestones:

• The Education Fund: Using tools like SIPs in diversified funds to combat education inflation.

• The Legacy Plan: Ensuring that your estate whether it’s property or shares is documented through a clear will or nomination process.

Real-Life Examples

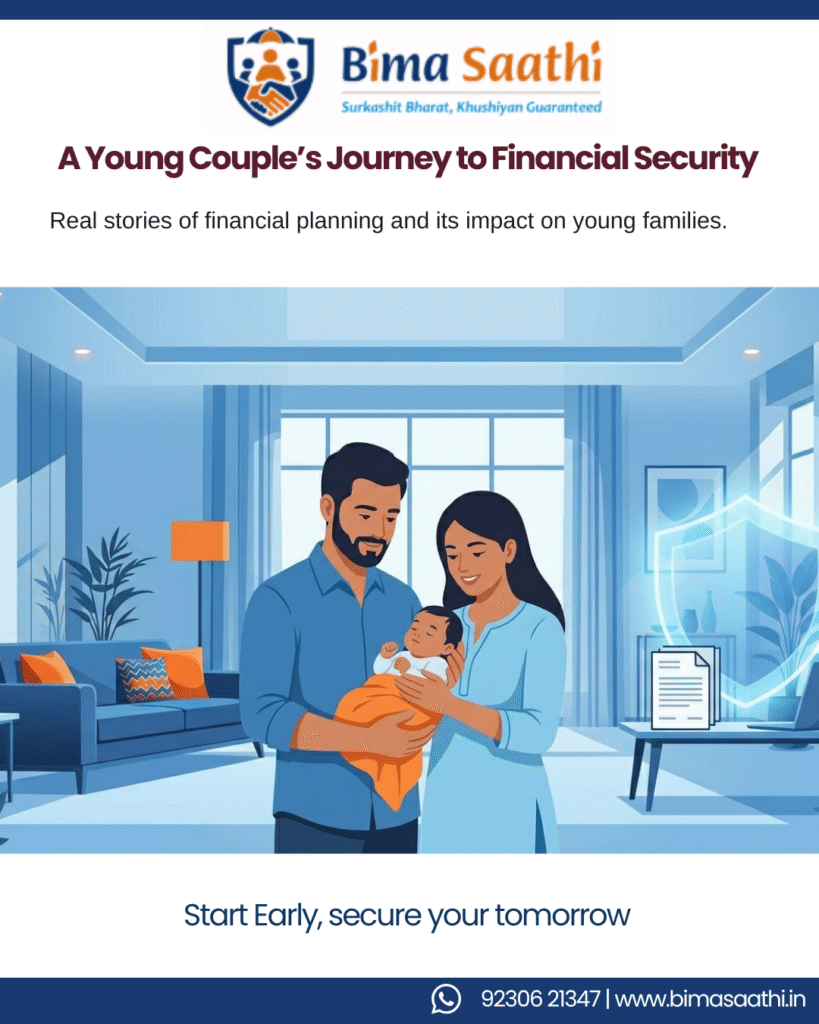

Example A: The Young Couple

Rahul and Priya just started their family. They were focused on buying a bigger car. However, after a Family First consultation, they realized that while the car adds comfort, a Term Insurance policy and a Health Super Top-up would add security. They reallocated their “luxury budget” to ensure that if anything happened to Rahul (the primary earner), Priya and their newborn would never have to leave their home.

Example B: The Multi-Generational Household

Anish supports his wife, two children, and his elderly parents. His biggest risk was “Medical Gap.” By opting for Critical Illness Insurance and a specialized Senior Citizen Health Plan for his parents, he protected his primary savings from being liquidated during a health scare.

The Solutions: How to Start Today

1. The Audit: Sit down with your spouse. List every debt, every asset, and every monthly expense.

2. The Gap Analysis: Use the Bima Saathi tools to check if your current insurance coverage actually meets your family’s needs. Are you under-insured?

3. Automate the Safety Net: Set up automatic transfers to your emergency fund and insurance premiums. Security should be non-negotiable and automatic.

4. Review the Nominees: A simple but vital step. Ensure all your bank accounts and policies have the correct family members listed as nominees.

Related Section & Resources

To dive deeper into specific protection strategies, explore our detailed guides:

• Understanding the Importance of Term Life Insurance

• Choosing the Right Health Insurance for Your Parents

Why Family First Financial Planning India Works

Because it shifts focus from:

❌ “Mere paas kitna paisa hai?”

👉 to

✅ “Meri family kitni secure hai?”

Aur honestly, end goal bhi wahi hai.

“We don’t earn just for ourselves we earn for peace of mind.”

FAQs (SEO Optimised)

1. What is family first financial planning in India?

Family first financial planning focuses on securing family needs through budgeting, insurance, savings, and goal-based investments.

2. How much emergency fund should a family have in India?

A family should maintain at least 6 months of expenses as an emergency fund.

3. Why is insurance important in financial planning?

Insurance protects families from financial shocks like medical emergencies and loss of income.

4. Can POSP be a good career option in India?

Yes, POSP offers flexible income opportunities with low investment and high earning potential.

5. How to start financial planning for beginners in India?

Start with budgeting, build an emergency fund, get insurance, and begin SIP investments.

Takeaways & Final Words

Family First Finance is not about deprivation; it’s about prioritization. It’s the peace of mind that comes from knowing that no matter what the world throws at you, your home remains a sanctuary. Money is a tool make sure it’s serving the people you love the most.

At Bima Saathi, our mission is “Surakshit Bharat, Khushiyan Guaranteed.” We don’t just sell policies; we build safety nets. Whether you are looking for life cover, health protection, or guaranteed return plans to secure your child’s future, we are here to guide you with a human-tech approach.

Don’t leave your family’s future to chance. Let’s build your fortress together.

Connect With Us

Ready to take the first step toward a Family First financial plan? Reach out to our expert consultants for a personalized risk gap analysis.

• 📞 Call / WhatsApp: + (91) 92306 21347

• 📧 Email: support@bimasaathi.in

• 🌐 Visit: www.bimasaathi.in

• Follow us for more tips: Stay updated with the latest in financial security and insurance by visiting our blog regularly.

Leave A Comment