Key Summary

In India, securing a child’s future is often seen as the ultimate test of parenting. This overwhelming pressure, combined with skyrocketing education inflation (10-12%), frequently drives parents to “over-invest” pouring all their liquidity into one or two goals while neglecting their own retirement or immediate family security. This blog breaks down how to build a robust, sustainable financial shield for your child. It moves beyond traditional gold and FDs to explain why protection (insurance) must come before investment (growth), and how to achieve genuine stability without compromising your own financial dignity.

Introduction: The Aspirational Pressure and the “Return” Obsession

If you are a parent in a Tier-2 or Tier-3 Indian city today, the emotional weight of “settling” your child is immense. We are taught to sacrifice everything today so that our children can have a glorious tomorrow.

As soon as a child is born, the well-meaning advice pours in: “Sona khareed lo” (Buy gold), “Post Office mein FD karao” (Start an FD), or the most standard Indian response: “Insurance policy lo, returns milenge” (Buy an insurance policy, it gives returns).

This “returns-oriented” mindset is where the trouble begins. In our desperation to achieve a massive corpus for a daughter’s wedding or a son’s professional degree, we often commit to heavy, long-term investments that we can barely afford. We “over-invest” today, believing that any policy that pays out later is good, without analyzing inflation, logic, or protection value.

“Bachche ke kal ki fikar mein, hum kal (future) khud ke liye kuch bachana bhool jaate hain.”

At Bima Saathi, we believe that true child security is built on a foundation of clarity, not just sacrifice. Securing your child’s future isn’t about investing the most money; it’s about investing the right money, responsibly. Let’s shift from being “aggressive investors” to becoming “Smart Protectors.”

The Story of Ajay vs. Vijay

Let’s look at two neighbors, Ajay and Vijay, living in a vibrant Tier-2 town. Both are earning ₹50,000 a month and have identical family structures and child-centered dreams.

Ajay (The Goal-Obsessed “Over-Investor”)

As soon as his son was born, Ajay was pressured into committing to three separate Traditional/Endowment Insurance policies, each costing ₹15,000 a quarter. He pours ₹60,000 annually into these, because “return milega 20 saal baad” (I’ll get returns in 20 years). His logic is that the lump sum is his son’s “security.” He has no Term Life Insurance because he saw it as “invisible spending” with zero return.

Vijay (The “Balanced Protector”)

Vijay chose a different path after sitting with a Bima Saathi advisor. He prioritized protection before growth. He secured:

A Term Life Plan (Sum Assured: ₹1.2 Crore) with an income payout rider, costing ₹15,000 annually. (This secures his Human Life Value).

A robust standalone Health Plan (₹10 Lakh base + ₹20 Lakh Top-up). (This protects his existing savings).

After these shields, Vijay invests only ₹20,000 annually in inflation-beating SIPs (Systematic Investment Plans) for growth.

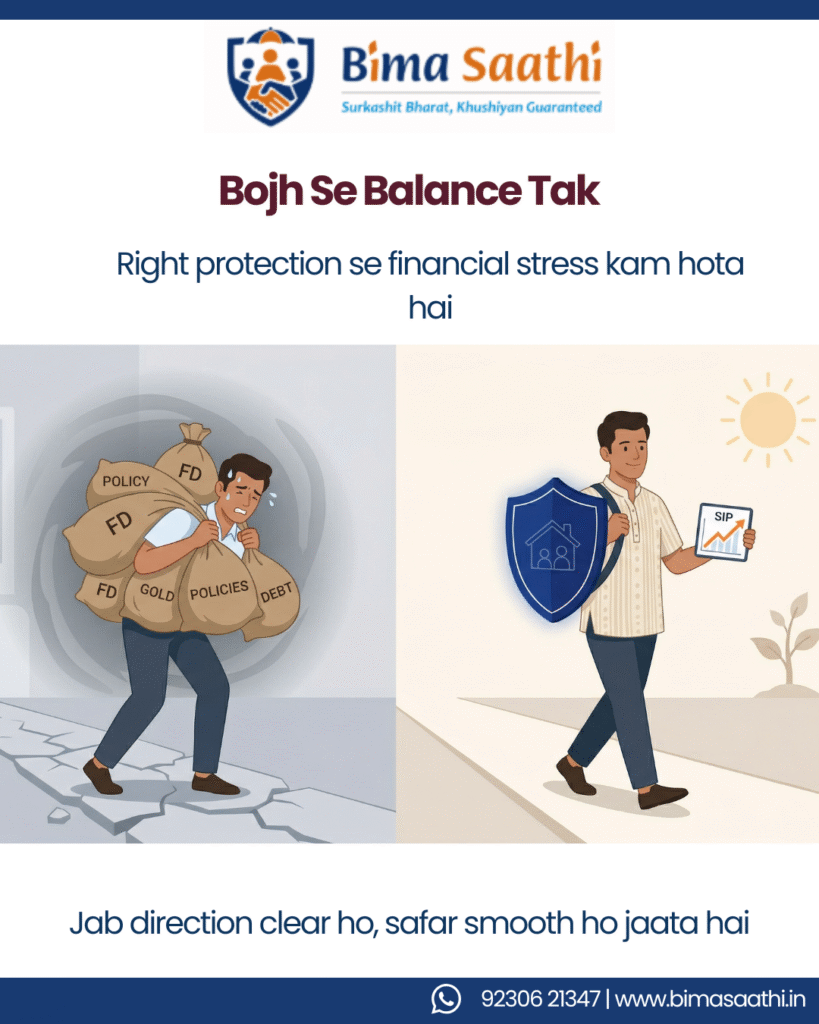

The Problem: When Over-Investing Leaves You Vulnerable

Ajay’s mistake is a common Indian parent’s mistake: confuse “savings” with “protection.”

1. Inflexible Committment & Inflation Failure

The Traditional/Endowment policies that Ajay chose are fixed, inflexible committments. If his income fluctuates (as is common in modern times), he cannot easily adjust the premium. More importantly, these policies typically yield 4-6% returns—often failing to even beat education inflation which is closer to 10-12% in India. He thinks he is over-investing, but he is actually losing purchasing power.

2. The “No Shield” Risk (Disability or Critical Illness)

The traditional policies don’t help much today. If Ajay faces a critical illness or disability tomorrow, and cannot work, his income stops. He still has to pay the premiums to get the payout in 15 years, but he cannot. His family standard of living crashes immediately. Confusing? Yes.

To avoid these traps and learn how to secure your child responsibly, read our detailed guide on Financial Planning for Young Parents in India: Securing Your Child’s Dreams from Day One.

3. Retirement Compromise

Because Ajay is over-investing in his child’s goals, he has no liquidity to save for his own retirement. He is banking on his son supporting him later. If his son doesn’t, or cannot, Ajay faces old age without dignity—an emotional and financial strain on his child.

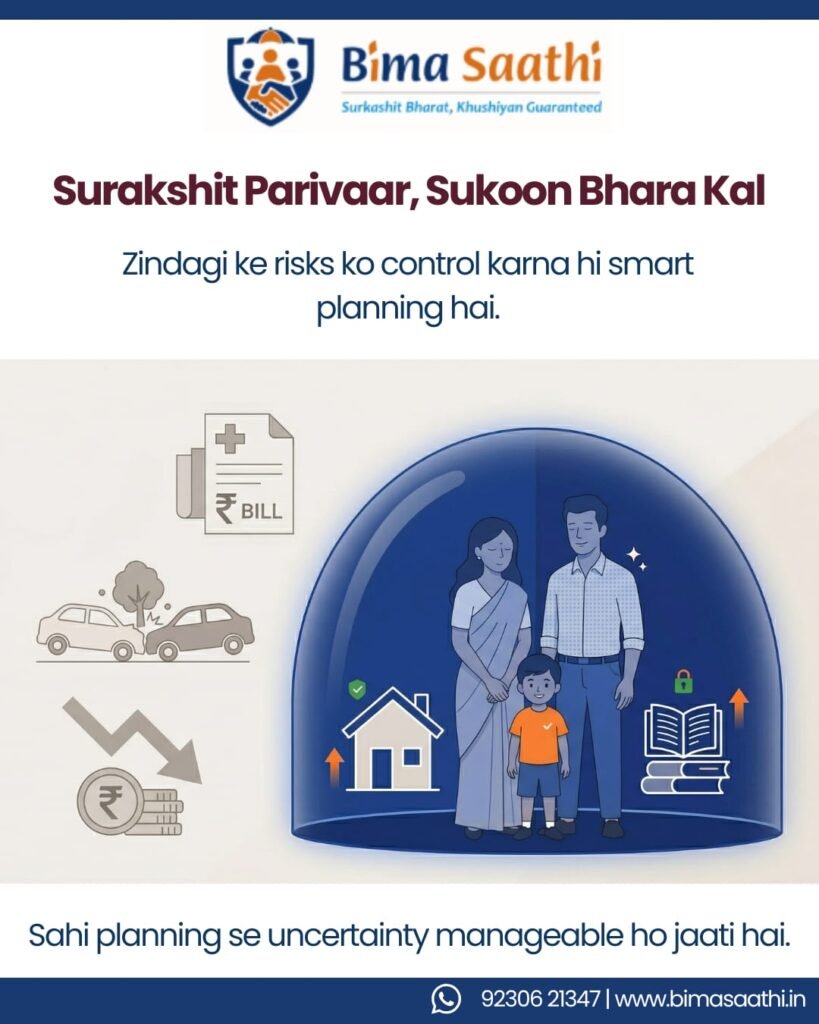

Building Your “Suraksha Kavach” (The Solution Blueprint)

The key to securing your child without over-investing is to build a comprehensive plan that integrates Protection, Continuity, and Growth.

Step 1: Immediately Build Your “Protection Shield”

Before you invest for the future, you must protect the present. If the engine breaks, no map can help you reach the destination.

1.1. Health Insurance (The Medical Shock Absorber): Do not rely on your company policy. Buy a standalone Family Floater Plan. If one family member faces a serious illness, your years of saved money shouldn’t vanish. Healthcare inflation is 12-14%; a ₹5 Lakh cover is no longer enough. To avoid wiping out your savings during a health crisis, discover why A Hospital Bill can Vanish your Saving: Why Health Insurance Matters.

1.2. Term Life Insurance (The Income Continuity Shield): A Term Plan is not “invisible spending”; it is Family Dignity. Your Sum Assured should be 15-20 times your annual income. If you are not there, this replacement salary ensures your child’s standard of living—their school, their home, and their future—remains exactly the same. Hinglish Punchline: “Term plan apke jane ke baad aur health plan apke rehne ke waqt pariwar ka khyal rakhta hai.”

Step 2: Income Protection (Protecting the “Earning Pillar”)

Most parents plan for what happens after death. But what about survival with disability or long-term illness? This is the ignored risk that often forces parents to over-invest in traditional plans.

If the earning member faces disability:

Expenses continue and increase (caregiver, modifications).

Income pauses or stops.

You use your child’s goal money to survive.

Secure a dedicated Personal Accident Cover and Critical Illness rider to bridge this gap. This provides a lump sum for immediate adjustments and acts as a monthly “salary replacement” during recovery, ensuring you never need to touch your child’s long-term fund.

Income Protection (The “Waiver of Premium” Lock-in)

This is a critical concept that prevents over-investing in wrong products. Many modern child insurance policies offer a Waiver of Premium (WoP) rider.

The Concept: If the parent (the payer) faces untimely demise, critical illness, or permanent disability during the policy term, the insurance company waives all future premiums.

Why It Matters: The policy doesn’t stop. The insurance company continues paying into the policy on the parent’s behalf. This ensures the intended corpus is built by the target maturity age (e.g., 18 or 21).

WoP addresses the ultimate parental fear: “What if I’m not there to complete the investment?” It locks in the goal corpus, providing complete peace of mind without requiring you to pour excessive, inflexible premiums into endowment plans.

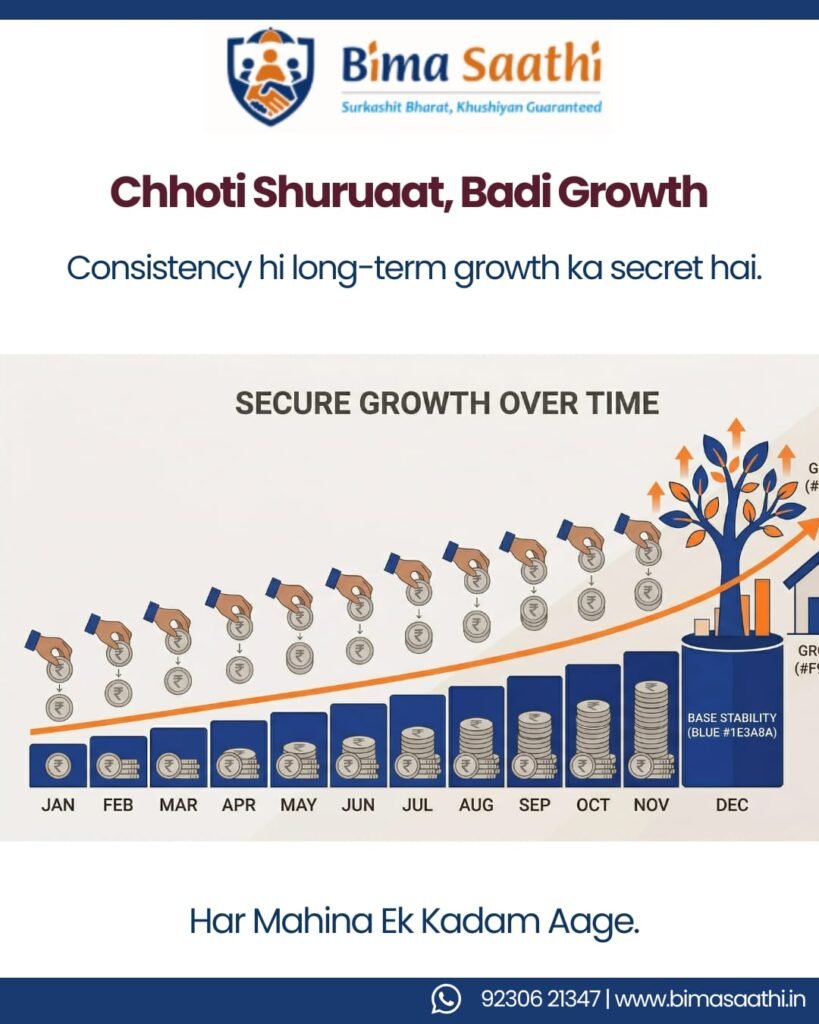

Step 3: Specific Child Goal Investment (Beat Education Inflation)

Only after Step 1 & 2 are in place should you focus on growth.

3.1. Start Early (The Power of Compounding): Even ₹2,000 invested monthly when your child is born grows significantly larger than ₹10,000 invested when they are 12 years old.

3.2. Diversify for Growth (Equity SIPs): For goals 15-18 years away, you must beat inflation. Equity Mutual Funds via SIPs are ideal. They provide 12-15% long-term historical returns, which is necessary to combat education inflation (10-12%). You cannot achieve this with FDs or Traditional Insurance alone.

Choose the Right Instruments (Not Too Many)

Avoid:

- Too many policies

- Complex products

Focus:

- Mutual funds (SIP)

- PPF

- Term insurance

Example:

₹5,000 SIP for 15 years @12%

Step 5: Don’t Ignore Liquidity

Long-term planning important hai

But liquidity bhi zaroori hai

Include:

Emergency fund (6 months expenses)

Liquid savings

Step 6: Review Regularly, Don’t Panic

Review every 6–12 months:

Goals track par hain?

Returns realistic hain?

Avoid:

- Market panic

- Trend chasing

“Consistency beats confusion.”

Why Insurance is Your True “Stability Foundation” During Volatile Times

When your career path or health is volatile, your protection net must be solid. Insurance is the structural support that prevents life’s inevitable shocks from turning your child’s future into a tragedy.

The Vijay Counter-Scenario (If Vijay faced the same shock as Ajay):

If Vijay had faced a career volatility or medical shock:

His standalone Health Insurance would have protected his existing SIPs.

His dedicated disability cover would have provided survival income, ensuring he didn’t need to default on his Term Insurance or break his Mutual Funds.

His family would be economically calm. When the crisis ended, Vijay’s child-goal SIPs would continue growing exactly as planned, with dignity.

Common Mistakes Parents Make

- Emotional investing

- Insurance ignore karna

- Over-diversification

- Inflation ignore karna

- Peer pressure decisions

“Har option lena zaroori nahi, sahi option lena zaroori hai.”

Solutions & Takeaways: Moving From Anxiety to Awareness

Young parents must shift their mindset from “return-oriented savings” to “risk-oriented protection.” Reclaim your financial dignity.

1. Pehele ‘Suraksha’, Fir ‘Sukh’ (Protection first, then happiness).

2. Health & Term Insurance are your Shield. SIPs & Investment Schemes are your Sword.

3. Start Early. Even a Small Step is a Giant Leap.

4. A financially independent parent is the ultimate security for a child.

Connect with Bima Saathi

Is your current financial system strong enough to protect your child’s dreams against inflation and unpredictable “Interruption”? Or are you confusing “saving money” with “income continuity”? At Bima Saathi, we help Indian families design their own personalized, resilient security fortresses.

Decision aapka hoga.

📞 Call / WhatsApp: +91 92306 21347

📧 Email: support@bimasaathi.in

🌐 Visit: www.bimasaathi.in

FAQs – Frequently Asked Questions

1. What is child future financial planning in India?

It is a structured approach to secure your child’s education and future expenses through insurance and investments.

2. How much should I invest for my child’s future?

You should invest 15–25% of your income depending on your financial goals.

3. Is insurance necessary for child planning?

Yes, insurance protects your income and ensures your plan continues even during emergencies.

4. Which investment is best for child education?

Mutual funds (SIP), PPF, and Sukanya Samriddhi Yojana are effective options.

5. What is over-investing in financial planning?

Over-investing means putting excessive money into investments without maintaining financial balance.

Leave A Comment