Key Summary (65 words)

Salary aane ke baad excitement high hota hai—but yahi moment aapki financial life ka foundation bhi set karta hai. Is blog mein hum discuss karenge first 5 smart financial decisions jo har salaried individual ko lena chahiye from budgeting and emergency funds to insurance and side income options like POSP. Thoda planning, thoda discipline… aur future ho jayega sorted.

Salary Aane Ke Baad First 5 Financial Decisions (Smart Start Guide)

Target Keyword: Salary ke baad financial planning

Salary ka SMS aate hi jo feeling hoti hai na… “Aaj toh treat banti hai!” 😄

Lekin sach yeh hai ki salary ka first use hi aapka financial future decide karta hai.

India mein average salaried individual apni income ka 30–40% impulsive spending mein uda deta hai (source: financial behavior surveys). Aur phir mahine ke end mein “budget tight hai” wala dialogue.

Agar aap bhi iss cycle ko todna chahte ho, toh yeh 5 decisions aapko turant lene chahiye.

1. Budget Banaao – Paisa Control Mein Lao

Sabse pehla step simple hai: budgeting.

Aapka paisa kahaan jaa raha hai, yeh samajhna zaroori hai. Aap 50-30-20 rule use kar sakte ho:

- 50% – Needs (rent, food, bills)

- 30% – Wants (shopping, eating out, Netflix 😅)

- 20% – Savings & investments

Example:

Agar aapki salary ₹40,000 hai:

- ₹20,000 → Needs

- ₹12,000 → Wants

- ₹8,000 → Savings

Reality check: India mein sirf 27% log hi proper budget follow karte hain.

Agar aap yeh ek habit bana lete ho, toh aap already majority se ahead ho.

“Budget banana restriction nahi, freedom ka blueprint hai.”

2. Emergency Fund – “Life Unpredictable Hai, Savings Predictable Honi Chahiye”

Kabhi bhi job loss, medical emergency ya sudden expenses aa sakte hain.

Isliye ek emergency fund banana must hai.

Kitna hona chahiye?

- Minimum: 3–6 months ke expenses

- Ideal: ₹1–2 lakh (depending on lifestyle)

Example:

Agar aapka monthly expense ₹25,000 hai →

Emergency fund = ₹75,000 – ₹1,50,000

Start small:

- Har month ₹3,000–₹5,000 alag rakho

- 12–18 months mein solid fund ready

India mein 80% log emergency ke liye prepared nahi hote matlab crisis mein loan lena padta hai.

“Savings woh nahi jo bachta hai, savings woh hai jo pehle nikala jaata hai.”

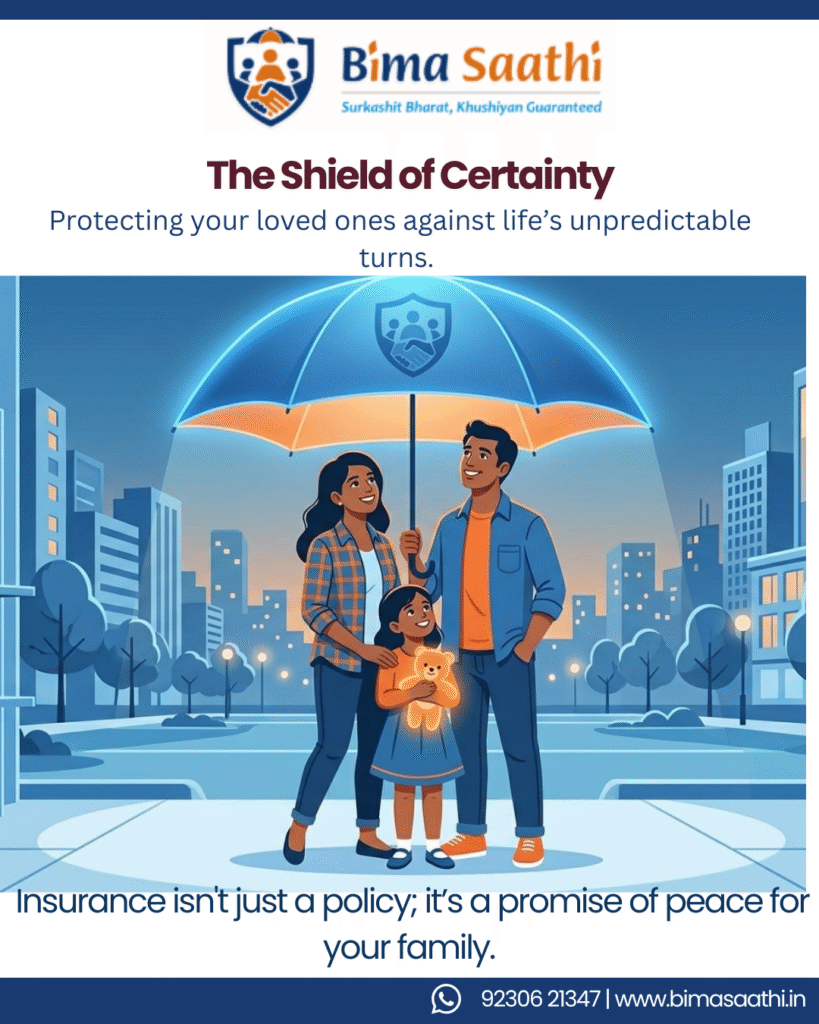

3. Insurance Lo – Protection Pehle, Investment Baad Mei

Salary ke baad financial planning ka sabse ignored step hai: insurance.

Log mutual funds mein invest kar lete hain, crypto le lete hain…

lekin protection bhool jaate hain.

Basic Insurance Checklist:

- Term Life Insurance: 10–15x annual income

- Health Insurance: ₹5–10 lakh cover

Example:

Agar aap ₹5 lakh yearly earn karte ho →

Term plan = ₹50–75 lakh

Aur premium?

- Sirf ₹500–₹800/month (young age mein)

Healthcare inflation India mein 10–12% per year badh raha hai.

Ek hospitalization ₹1–3 lakh ka bill bana deta hai.

Yahan aap explore kar sakte ho:

Insurance basics samajhne ke liye:

“Agar plan nahi hai, toh problem guaranteed hai.”

4. SIP Start Karo Chhota Investment, Bada Future

Agar aapne abhi tak investing start nahi kiya hai, toh aaj hi start karo.

SIP (Systematic Investment Plan) beginners ke liye best hai.

Example:

₹5,000/month SIP

- 12% return pe

- 10 saal mein = approx ₹11.6 lakh

Magic of Compounding:

Jitna jaldi start karoge, utna zyada benefit.

India mein sirf 3% population actively mutual funds mein invest karti hai matlab huge opportunity.

Start with:

- Index funds

- Large-cap funds

“Time in market, timing se zyada powerful hota hai.”

5. Extra Income Socho – Salary Se Aage Badho (POSP Opportunity)

Ek salary se aap survive kar sakte ho…

lekin wealth create karne ke liye multiple income sources zaroori hain.

Yahan aata hai POSP (Point of Sales Person) opportunity.

POSP Kya Hai?

- Insurance products sell karna

- Flexible timing

- Work from anywhere

Earnings Potential:

- Part-time: ₹10,000–₹25,000/month

- Full-time: ₹50,000+ possible

India mein insurance penetration abhi bhi ~4% ke aas paas hai, matlab demand huge hai.

Agar aap communication mein ache ho, toh yeh ek strong side income option hai.

Start your journey yahan se:

POSP career opportunity samjhein:

“Ek income se guzara hota hai, multiple incomes se growth hoti hai.”

Common Mistakes After Salary (Avoid These!)

- Salary aate hi shopping spree 🛍️

- Credit card ka overuse

- Savings ko last priority dena

- Insurance ignore karna

- “Kal se start karenge” mindset

Reality:

Financial success ek din mein nahi banta daily habits se banta hai.

“Aaj ka discipline, kal ki luxury banata hai.”

Quick Action Plan (Simple & Practical)

✔ Salary ka 20% automatically save karo

✔ Emergency fund start karo (even ₹500 se)

✔ Term + health insurance lo

✔ ₹2,000–₹5,000 SIP start karo

✔ Side income explore karo (POSP best option)

Conclusion

Salary sirf income nahi hai

yeh ek opportunity hai.

Agar aapne pehle 6–12 months smart decisions le liye,

toh aapka financial future secure ho sakta hai.

Warna… salary aayegi, kharch hogi, aur phir wait next month ka 😅

“Pehli salary se lifestyle nahi, system banao.”

FAQs (SEO Optimised)

1. Salary ke baad financial planning kaise shuru karein?

Salary ke baad financial planning budgeting se start karein, phir emergency fund, insurance aur SIP investments par focus karein.

2. Kitna emergency fund hona chahiye India mein?

India mein minimum 3–6 months ke expenses ka emergency fund hona chahiye, jo ₹50,000 se ₹2 lakh tak ho sakta hai.

3. Salary ke baad kaunsa investment best hai?

Beginners ke liye SIP in mutual funds best hai, kyunki yeh disciplined aur low-risk entry deta hai.

4. Kya insurance lena zaroori hai salary ke baad?

Haan, term insurance aur health insurance lena zaroori hai taaki financial risks cover ho sakein.

5. POSP kya hota hai aur kaise join karein?

POSP ek insurance selling role hai jisme aap part-time ya full-time income earn kar sakte hain, aur aap ise online join kar sakte hain.

Connect with us

Agar aap apni salary ko sirf income nahi, wealth building tool banana chahte ho…

toh right guidance zaroori hai.

💼 Insurance, financial planning aur POSP career ke liye expert support paayein:

📞 Call / WhatsApp: + (91) 92306 21347

📧 Email: support@bimasaathi.in

🌐 Visit: www.bimasaathi.in

Bima Saathi ke saath sirf policy nahi, future secure hota hai.

Leave A Comment