Key Summary

Home loan lena sirf EMI bharna nahi hota yeh ek long-term financial commitment hai. India mein average home loan tenure 20–30 years ka hota hai, aur chhoti planning mistakes aage chal kar heavy burden ban sakti hain. Is blog mein hum simple Hinglish mein explain karenge ki ghar ka loan lene se pehle kya zaroori steps lene chahiye taaki decision pressure mein nahi, clarity ke saath liya jaaye.

🏠 What Every Family Should Do Before Taking a Home Loan

“Ghar lena sapna hota hai… par bina planning ke, yeh sapna pressure bhi ban sakta hai.”

India mein home loan market ₹30 lakh crore se bhi zyada ka ho chuka hai. Har saal lakhon families apna ghar lene ka decision leti hain. Lekin ek important sawaal aksar miss ho jaata hai:

👉 “Kya hum loan lene ke liye ready hain?”

Chaliye step-by-step samajhte hain Home Loan Planning India ka sahi approach kya hona chahiye.

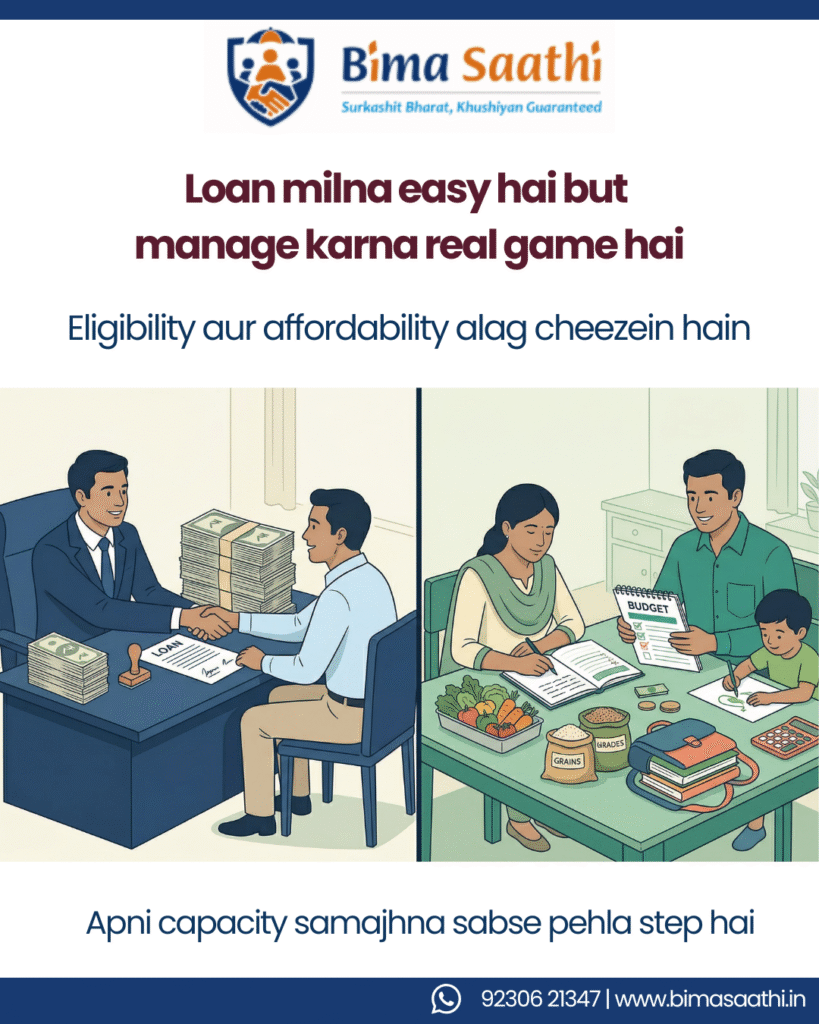

1. Apni Real Affordability Samjho (Not Just Eligibility)

Banks aapko ₹50 lakh ka loan approve kar denge…

Lekin iska matlab yeh nahi ki aapko ₹50 lakh lena hi chahiye.

👉 Rule of thumb:

- EMI should not exceed 30–40% of your monthly income

Example:

Agar aapki family income ₹60,000/month hai:

- Safe EMI = ₹18,000 – ₹24,000

Par agar EMI ₹30,000 ho gayi?

Toh baaki life compromise ho jayegi – education, health, emergencies.

2. Total Cost Samjho – Sirf Property Price Nahi

Ghar ka price ₹40 lakh hai…

Par actual cost kya hogi?

Hidden Costs:

- Registration & Stamp Duty: 5–8%

- Interior + Furniture: ₹3–10 lakh

- Maintenance charges

- Loan processing fees

👉 ₹40 lakh ka ghar actually ₹45–50 lakh tak pahunch sakta hai.

3. Interest Rate Samjho – Small Difference, Big Impact

Interest rate 8.5% vs 9% lagta hai chhota difference…

Par 20 saal mein yeh lakhon ka farq ban jaata hai.

Example:

₹30 lakh loan for 20 years:

- @8.5% → Total interest ≈ ₹32 lakh

- @9% → Total interest ≈ ₹35 lakh

👉 Difference = ₹3 lakh+

“Rate chhota lagta hai… par effect bada hota hai.”

4. Emergency Fund Banaao – Loan Se Pehle

India mein ek common mistake:

👉 Log down payment ke baad zero savings pe aa jaate hain.

Yeh risky hai.

Ideal Rule:

- At least 6 months expenses ka emergency fund hona chahiye

Example:

Monthly expense = ₹40,000

Emergency fund = ₹2.4 lakh

Agar job loss ya medical emergency aayi?

EMI rukti nahi.

“EMI rukti nahi… par income kabhi kabhi ruk jaati hai.”

Read More:

Income Protection: The Foundation of Financial Stability

https://bimasaathi.in/income-protection-the-foundation-of-financial-stability/

5. Insurance Planning Ignore Mat Karo

Home loan ka matlab hai:

👉 Family ka financial future aapki income pe dependent hai.

2 important covers:

- Term Insurance – Loan amount cover kare

- Health Insurance – Savings protect kare

India mein sirf ~30% log adequate life insurance cover rakhte hain.

Yeh gap dangerous hai.

👉 Agar kuch unexpected ho jaaye, toh:

- Loan ka burden family pe shift ho jaata hai

Read More:

Ek Hospital Bill, Saalon Ki Savings Gayab: Why Health Insurance Matters

https://bimasaathi.in/ek-hospital-bill-saalon-ki-savings-gayab-why-health-insurance-matters-in-india/

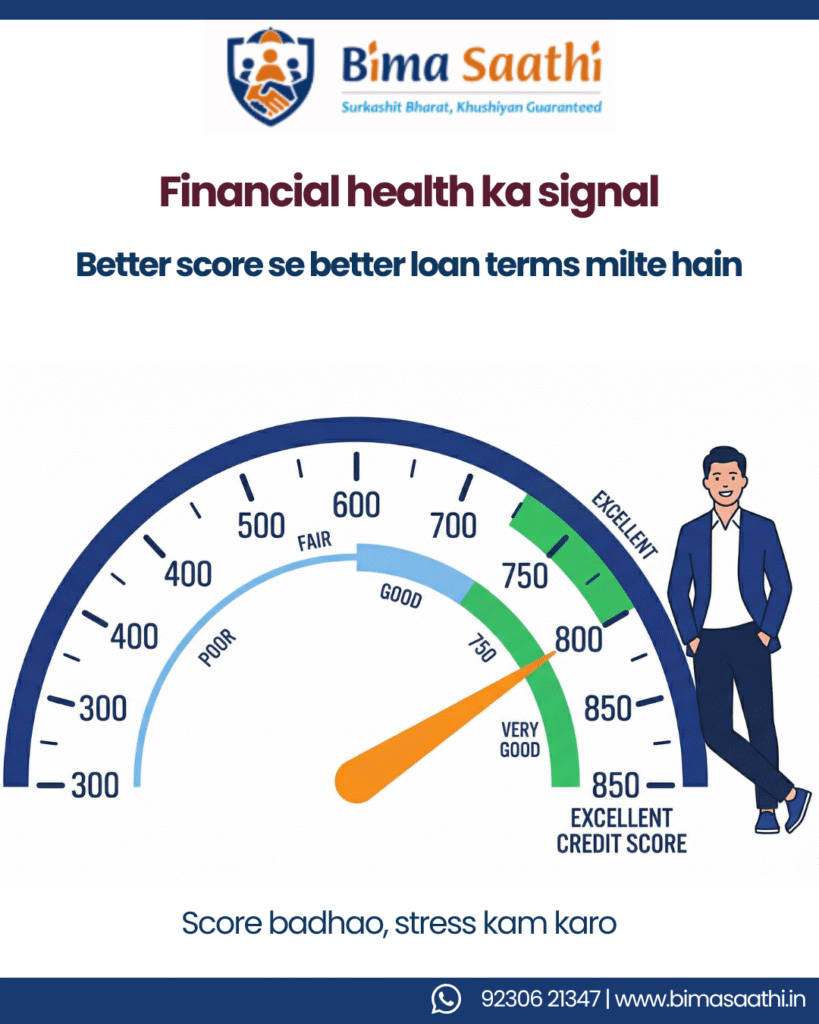

6. Credit Score Improve Karo

Aapka CIBIL score (750+) directly impact karta hai:

- Loan approval

- Interest rate

- Negotiation power

Tips:

- Credit card dues time pe pay karo

- Existing loans close karo

- Multiple loan applications avoid karo

“Achha score sirf number nahi… negotiation power hai.”

7. Fixed vs Floating Rate – Samajh Ke Choose Karo

Fixed Rate:

- EMI stable

- Safe but slightly higher

Floating Rate:

- Market linked

- Kabhi kam, kabhi zyada

👉 India mein majority loans floating rate pe hote hain.

Smart approach:

Agar risk tolerance low hai → Fixed

Agar flexibility chahiye → Floating

“Stability ya flexibility – decision aapka, impact long-term ka.”

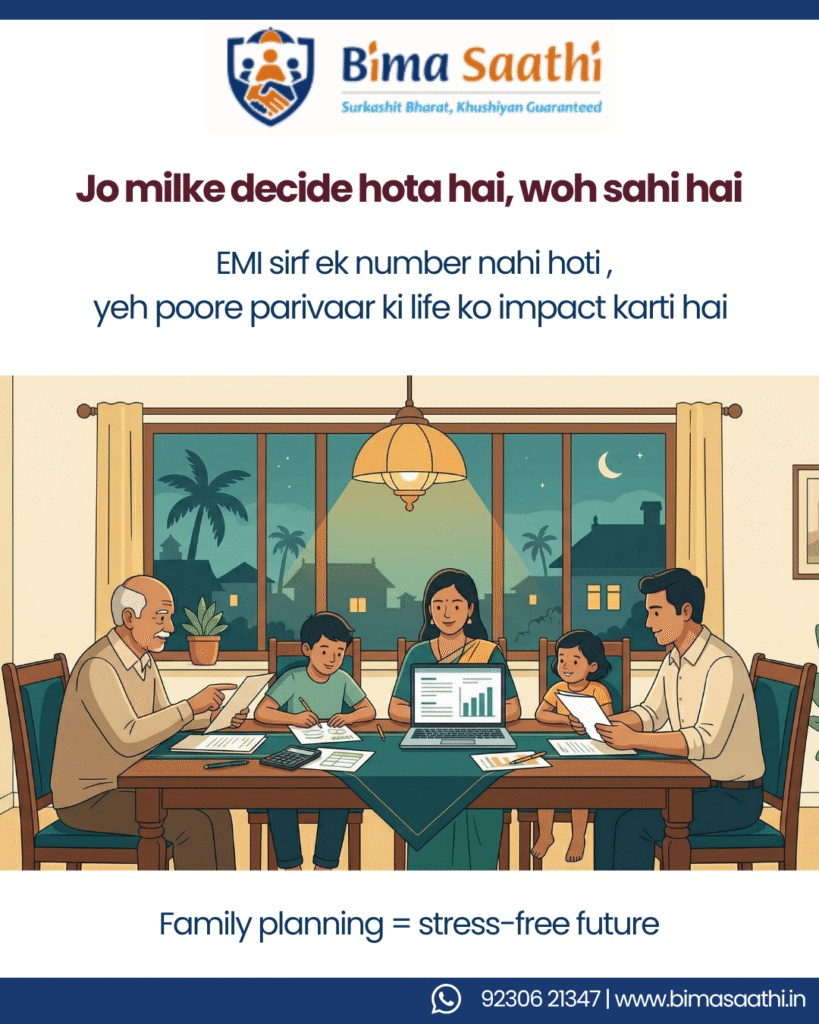

8. 👨👩👧 Family Discussion Zaroor Kariye

Ghar lena individual decision nahi hai.

👉 Yeh family decision hai.

Discuss:

- EMI affordability

- Future plans (kids, education)

- Job stability

- Location priorities

9. Loan Tenure Smartly Choose Kariye

Long tenure = Low EMI

Short tenure = Less interest

Example:

₹30 lakh loan:

| Tenure | EMI | Total Interest |

| 20 yrs | ₹26,000 | ₹32 lakh |

| 30 yrs | ₹23,000 | ₹52 lakh |

👉 EMI ₹3,000 kam…

Par interest ₹20 lakh zyada!

“Kam EMI ka matlab sasta loan nahi hota.”

10. Right Guidance Lo – Blind Decision Mat Lijiye

Insurance aur loans dono complex hote hain.

👉 Confusion normal hai.

Isliye guidance lena weakness nahi — smartness hai.

Aap yeh bhi samajh sakte ho:

“Har decision khud lene ki zaroorat nahi… sahi guide hona kaafi hai.”

Takeaways

Home loan ek financial decision nahi…

life decision hai.

Agar planning strong hai:

👉 Ghar sukoon deta hai

Agar planning weak hai:

👉 Ghar stress deta hai

FAQs – Frequently Asked Questions

1. What is the ideal EMI percentage of income in India?

Ideally, your EMI should not exceed 30–40% of your monthly income to maintain financial stability.

2. How much emergency fund is needed before taking a home loan?

You should have at least 6 months of living expenses saved as an emergency fund.

3. Does credit score affect home loan interest rates in India?

Yes, a higher credit score (750+) can help you get lower interest rates and better loan terms.

4. Should I take a fixed or floating home loan interest rate?

Fixed rates offer stability, while floating rates offer flexibility depending on market conditions.

5. Is insurance necessary when taking a home loan in India?

Yes, term and health insurance help protect your family from financial burden in case of unexpected events.

Connect with Bima Saathi

Ghar lena ek bada step hai…

aur har bada step clarity ke saath lena chahiye.

Agar aap samajhna chahte hain:

- Kitna loan safe hai

- Kaunsa insurance zaroori hai

- Kaise family ko financially protect karein

📞 Call / WhatsApp: +91 92306 21347

📧 Email: support@bimasaathi.in

🌐 Website: www.bimasaathi.in

Decision aapka hoga. Saath hum denge.

Leave A Comment