Key Summary

कई भारतीय परिवारों में “Joint Financial Planning” को गलत तरीके से केवल एक बैंक खाता साझा करने या मासिक खर्चों पर चर्चा करने तक सीमित समझा जाता है। Bima Saathi का मानना है कि वास्तविक संयुक्त योजना का मतलब है एक मजबूत, साझा सुरक्षा तंत्र बनाना जो दोनों साथियों की गरिमा (dignity), स्वास्थ्य (health), और आय (income) को सुरक्षित रखे—चाहे जीवन में कुछ भी हो जाए। यह ब्लॉग पारंपरिक saving advice से आगे बढ़कर यह समझाता है कि protection (insurance) आपके संयुक्त financial journey का पहला कदम क्यों होना चाहिए, और कैसे मजबूत planning आपसी सम्मान और long-term financial balance (symmetry) बनाती है।

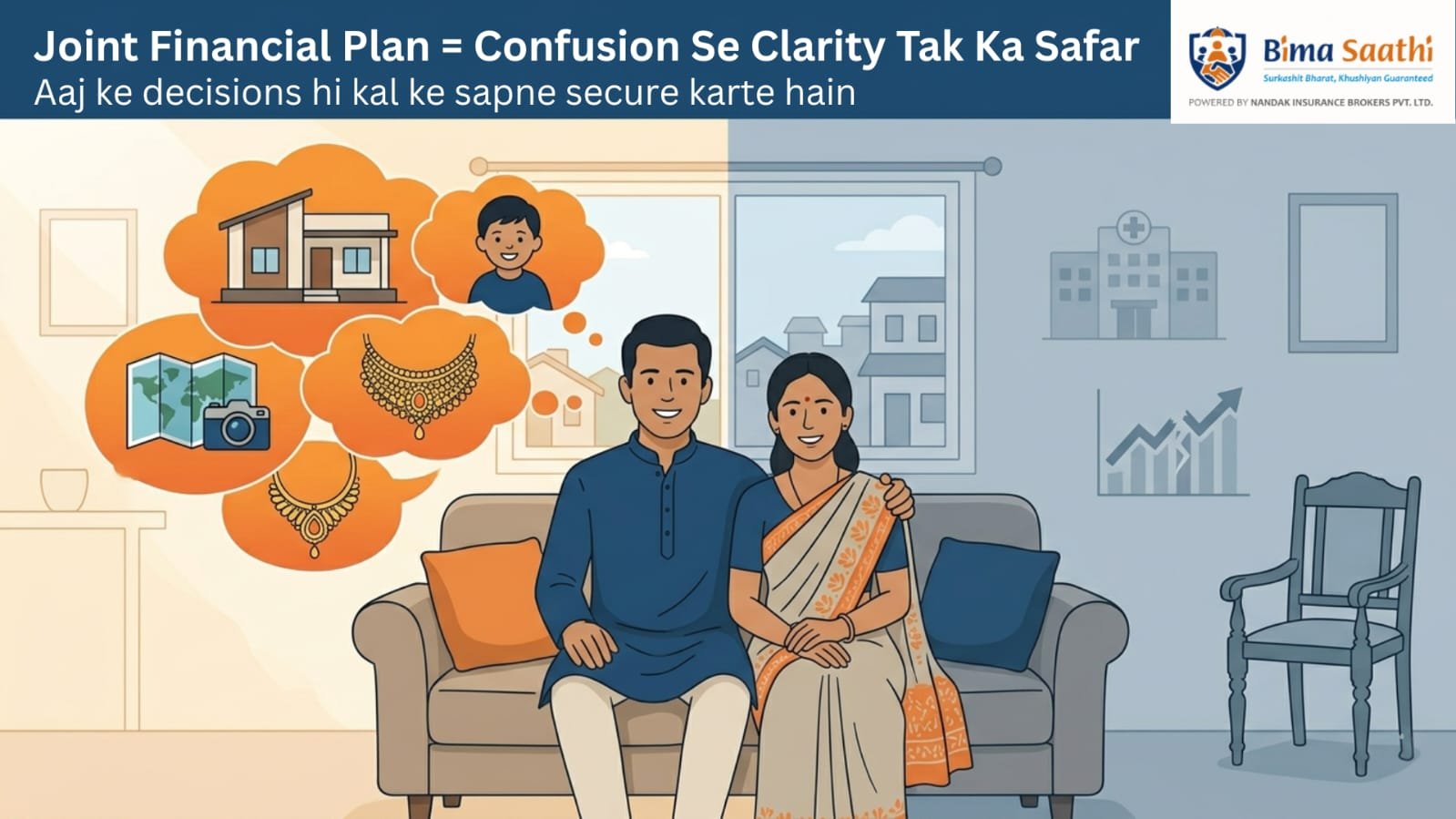

परिचय: “Shared Dreams, Silent Risks” का विरोधाभास

जब भारत में दो लोग शादी करते हैं, तो यह सिर्फ दिलों का मिलन नहीं होता; यह financial lives का भी एक merger होता है।

हम खुशी-खुशी अपने “Shared Dreams” पर चर्चा करते हैं:

“Kab ghar lenge?” (हम घर कब खरीदेंगे?),

“Bacche kab honge?” (हम बच्चे कब करेंगे?), और बहुत कुछ…

हम इन पलों के लिए उत्साह के साथ बचत करते हैं।

हम recurring deposits खोलते हैं और अपने gold investments को track करते हैं।

लेकिन इन shared dreams के साथ-साथ “Silent Risks” भी आते हैं, जिन पर अधिकांश भारतीय couples साथ बैठकर बात नहीं करते।

बहुत कम लोग मिलकर ये “Uncomfortable Conversations” करते हैं:

“What if I can’t work tomorrow?”

“What if one of us faces a medical crisis?”

अक्सर हम इन protective decisions को एक earning member पर छोड़ देते हैं, आमतौर पर पति पर, यह मानकर कि जब तक पैसा बच रहा है, परिवार सुरक्षित है।

“Pehle ‘Suraksha’, fir ‘Sukh’!”

Bima Saathi में हमारा मानना है कि modern और resilient joint financial planning की नींव सिर्फ साथ में invest करने में नहीं है; बल्कि पहले साथ में Protect करने में है।

आइए समझते हैं कि यह gap क्यों वास्तविक और खतरनाक है।

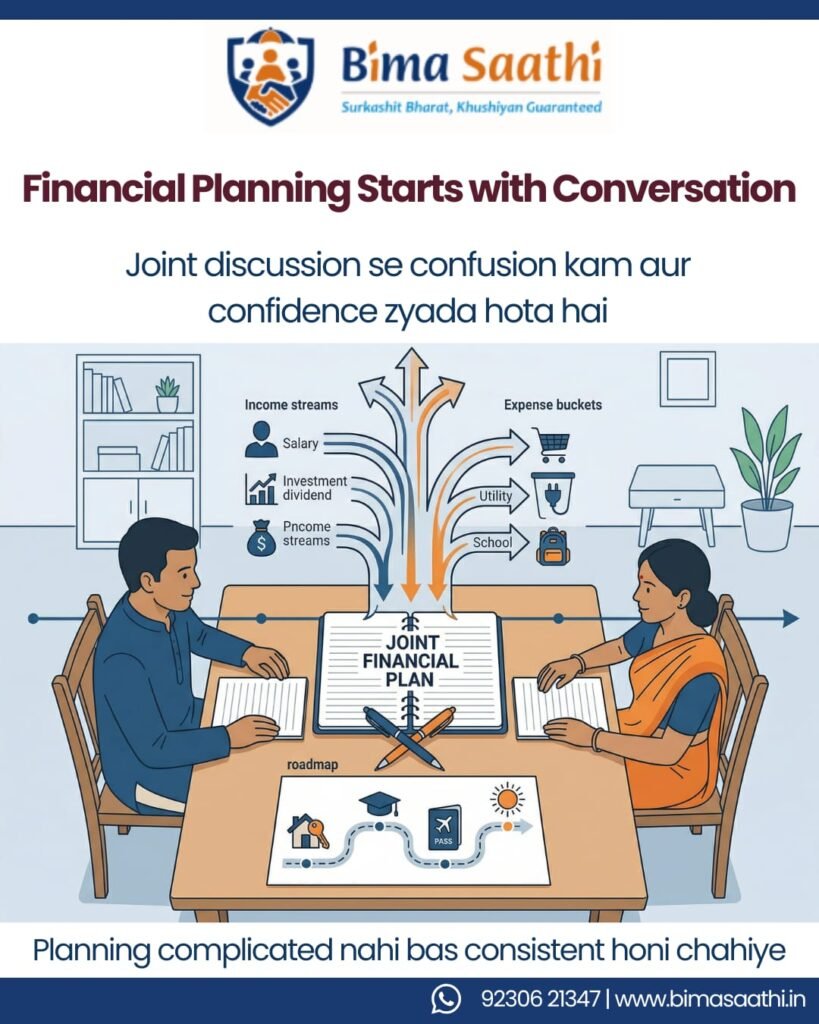

पति और पत्नी के लिए Joint Financial Planning क्या है?

Joint financial planning का मतलब है कि पति और पत्नी दोनों मिलकर financial decisions लें, उन्हें समझें और track करें।

इसमें शामिल होता है:

Income understanding: दोनों को पता हो कि कुल household income क्या है

Expense planning: Fixed और variable expenses स्पष्ट रूप से defined हों

Savings और investments: Goals के अनुसार allocate किए जाएं

Insurance coverage: दोनों का adequate protection हो

Future planning: Short-term और long-term goals aligned हों

इस पूरी प्रक्रिया का core है:

Transparency + Shared Responsibility

Joint Financial Planning क्यों जरूरी है

- 1. बेहतर Decision-Making

जब दोनों partners शामिल होते हैं, तो decision-making balanced होती है।

एक partner risk-oriented हो सकता है, दूसरा stability पसंद कर सकता है — दोनों मिलकर बेहतर outcome बनाते हैं।

Studies suggest करती हैं कि जिन households में joint decisions लिए जाते हैं, वहां long-term financial stability अधिक होती है।

“Ek ka decision fast hota hai… dono ka decision strong hota hai.”

2. Financial Transparency

अगर financial information साझा नहीं की जाती, तो trust issues और confusion पैदा हो सकते हैं।

Joint planning यह सुनिश्चित करता है:

सभी accounts और policies visible हों

कोई hidden liability न हो

यह स्पष्ट हो कि पैसा कहाँ जा रहा है

Transparency से unnecessary conflicts भी कम होते हैं।

“Jahan clarity hoti hai, wahan unnecessary tension nahi hota.”

3. Emergency Readiness

भारत में एक आम समस्या है:

सिर्फ एक व्यक्ति को financial details पता होती हैं।

अगर emergency आ जाए:

दूसरे partner को policies का पता नहीं होता

Claim process में delay होता है

Stress कई गुना बढ़ जाता है

Joint awareness सुनिश्चित करता है कि किसी भी स्थिति में दोनों तैयार हों।

“Information share nahi hai, toh planning half hai.”

4. Long-Term Goal Alignment

Family goals जैसे:

बच्चों की शिक्षा

घर खरीदना

Retirement

अगर दोनों aligned नहीं हैं, तो:

Savings mismatch हो जाता है

Goals delay होते हैं

Frustration बढ़ता है

Joint planning सुनिश्चित करता है कि दोनों एक ही दिशा में काम कर रहे हैं।

“Direction same ho, toh speed matter nahi karti.”

Reality Check: Couples में Financial Awareness Gap

भारत में financial awareness gap साफ दिखता है:

लगभग 70% households में financial decisions एक ही partner लेता है

25% से भी कम महिलाएं insurance decisions में actively शामिल होती हैं

कई मामलों में wives को policy details या nominee structure तक नहीं पता होता

यह gap long-term risk पैदा करता है।

👉 Related read: Why Every Woman Should Understand Insurance

समस्या: “Interrupt” और गरिमा (Dignity) का टूटना

Optimism एक अच्छी बात है, लेकिन finance में Optimism Bias (यह मानना कि बुरी चीजें हमारे साथ नहीं होंगी) खतरनाक है।

आपकी income आपके परिवार की oxygen है।

आपको यह सुनिश्चित करना चाहिए कि यह कभी रुके नहीं।

इस विषय पर विस्तार से जानने के लिए हमारा ब्लॉग पढ़ें:

Protecting the “Earning Years”: Disability and the Loss of Income Gap

https://www.google.com/search?q=https://bimasaathi.in/protecting-earning-years-disability/

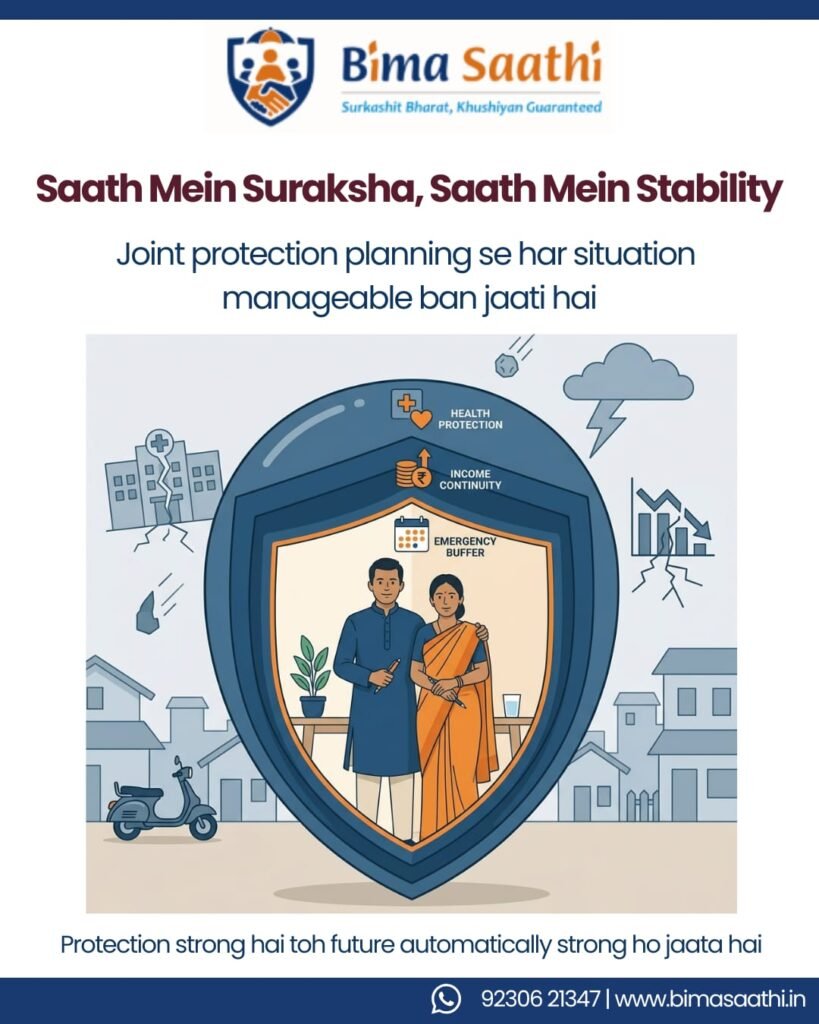

समाधान: Joint Resilience के लिए Bima Saathi Blueprint

वास्तविक joint financial wellness layers में बनता है — awareness और protection से शुरुआत होती है।

Step 1: Open Financial Conversation

एक सरल बातचीत से शुरुआत करें:

Total income क्या है

Monthly expenses क्या हैं

Important: यह discussion judgement-free होना चाहिए।

Step 2: तुरंत अपना “Protection Shield” बनाएं

Future के लिए invest करने से पहले present को protect करें।

“Pehle Suraksha, fir Sukh” (Protection first, then happiness)

2.1 Robust Insurance (Emergency Shock Absorber)

भारत में medical inflation 12–14% annually बढ़ रही है।

केवल employer cover या partner पर depend करना risky है।

ब्लॉग पढ़ें:

A Hospital Bill can Vanish your Saving: Why Health Insurance Matters

https://www.google.com/search?q=https://bimasaathi.in/importance-health-insurance-savings/

एक standalone Family Floater Plan + Super Top-up लें।

ऐसे plans चुनें जिनमें Restoration Benefit हो।

Women’s Critical Illness Riders भी जोड़ें।

2.2 Pure Term Life Insurance (Income Continuity Shield)

अगर main earner की मृत्यु हो जाए या Permanent Total Disability हो जाए, तो परिवार पर दोहरा असर पड़ता है:

Income loss

Expenses increase

आपका Sum Assured = आपकी annual income का 15–20 गुना होना चाहिए।

Income payout option वाला Term Plan एक “replacement salary” की तरह काम करता है, जो परिवार की dignity और goals को सुरक्षित रखता है।

2.3. Women’s Critical Illness Payout

महिलाओं के लिए insurance समझना बहुत जरूरी है, खासकर Tier-2 और Tier-3 cities में।

हमें “locker mentality” (सिर्फ सोने पर निर्भर रहना) से आगे बढ़ना होगा।

ब्लॉग पढ़ें:

Why Every Woman Should Understand Insurance

https://www.google.com/search?q=https://bimasaathi.in/why-women-should-understand-insurance/

Critical Illness riders diagnosis पर lump sum देते हैं (जैसे Cervical Cancer, Breast Cancer), जिससे recovery के दौरान dignity बनी रहती है।

Step 3: Goal Identification और Diversified Growth

Step 1 secure होने के बाद ही investing शुरू करें।

3.1. Child Education Planning

General inflation: 5–6%

Education inflation: 10–12%

इसलिए long-term goals के लिए Equity Mutual Fund SIPs जरूरी हैं।

SSA/PPF safe options हो सकते हैं।

ब्लॉग पढ़ें:

Financial Planning for Young Parents in India

https://www.google.com/search?q=https://bimasaathi.in/financial-planning-young-parents/

3.2. Retirement Corpus

“Education loans exist करते हैं, retirement loans नहीं।”

अपने retirement fund को compromise न करें।

Financially independent parent ही सबसे बड़ा gift है।

Step 4: Emergency Fund बनाएं

Experts recommend करते हैं:

6–9 months का expense buffer

Example:

Monthly expense ₹50,000

Emergency fund = ₹3–4.5 लाख

Step 5: Responsibility Assign करें (Knowledge Share करें)

Roles divide हो सकते हैं:

एक investments handle करे

दूसरा expenses track करे

लेकिन दोनों को overall understanding होनी चाहिए।

Step 6: Monthly Review System

हर महीने 20–30 मिनट का review करें:

- Budget check

- Savings track

- Goal progress

“Jo review hota hai wahi improve hota hai.”

Final Thoughts: Strong Relationship = Strong Financial System

शादी सिर्फ emotional bond नहीं है

👉 यह एक financial partnership भी है

Strong system के pillars:

- Transparency

- Awareness

- Planning

“Future secure karna hai… toh planning saath mein karni padegi.”

FAQs

1. Joint financial planning क्या है?

यह वह process है जिसमें दोनों partners मिलकर income, expenses और investments manage करते हैं।

2. यह क्यों जरूरी है?

यह transparency बढ़ाता है, risk कम करता है और बेहतर decisions सुनिश्चित करता है।

3. Couples कैसे शुरू करें?

Income, expenses और goals पर discussion से शुरुआत करें।

4. Insurance का क्या role है?

यह savings को protect करता है और emergencies में financial support देता है।

5. क्या couples POSP advisors बन सकते हैं?

हाँ, couples एक flexible और trust-based income बना सकते हैं।

BIMA SAATHI से जुड़ें

एक सरल सवाल:

“Aap planning alag-alag kar rahe hain… ya saath mein?”

अगर आप:

Joint financial planning शुरू करना चाहते हैं

Insurance समझना चाहते हैं

POSP opportunity explore करना चाहते हैं

तो BIMA SAATHI आपके साथ है।

Pehle samjhana. Phir margdarshan karna.

📞 Call / WhatsApp: +91 92306 21347

📧 Email: support@bimasaathi.in

🌐 Visit: https://bimasaathi.in/

Decision aapka hoga. Saath hum denge. 🤝

Leave A Comment