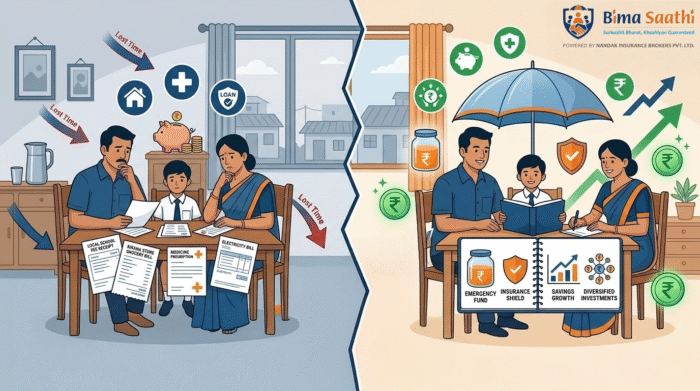

Key SummaryFor many years, financial advice suggested keeping three months of expenses as an emergency fund. But today’s financial realities, job uncertainty, rising healthcare costs, and fluctuating income mean that this buffer may no longer be enough. Strong emergency fund planning now requires a broader safety strategy that includes savings, insurance protection, diversified income sources, and better financial awareness. |

What Is Emergency Fund Planning?

Emergency fund planning means creating a financial safety buffer specifically for unexpected situations such as:

- sudden illness

- job interruption

- business slowdown

- urgent repairs

- family emergencies

This fund should be:

- easily accessible

- separate from long-term investments

- used only for genuine emergencies

“Emergency fund woh paisa hai jo mushkil waqt mein kaam aata hai.”

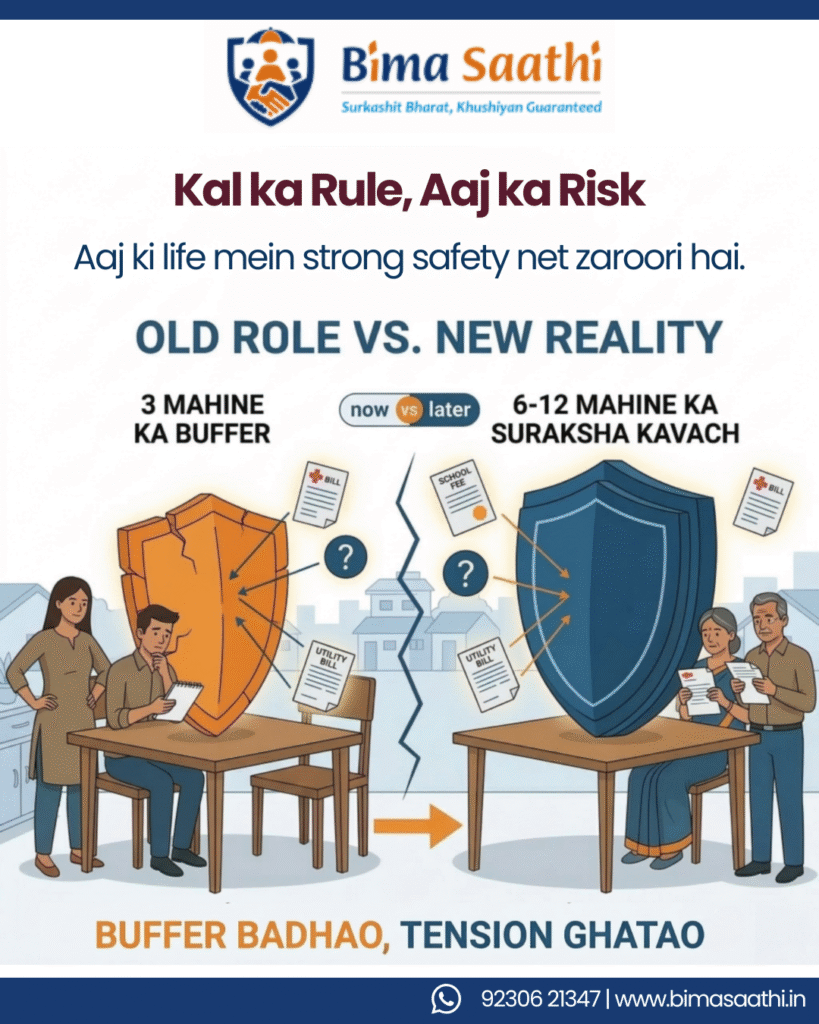

The Old Rule: “3 Months of Expenses”

Ask most people about emergency savings and the common answer is:

“Teen mahine ka buffer rakhna chahiye.”

For a long time, this rule worked well.

It assumed that:

- jobs were relatively stable

- expenses were predictable

- emergencies were manageable

But the reality of today’s economy looks very different.

Many households today experience:

- unpredictable income cycles

- rising healthcare costs

- longer job search periods

So the important question is no longer:

“Do you have 3 months of savings?”

The real question is:

“Will that be enough when life suddenly changes?”

Why the 3-Month Buffer May Not Be Enough Today

Several economic changes and AI has quietly made the traditional rule weaker.

1. Job Stability Is Not Guaranteed

Even stable jobs today can face unexpected changes.

Many professionals now experience:

- company restructuring

- temporary layoffs

- business slowdown

Employment studies suggest that job transitions can take 4–6 months on average.

If a household depends on one main earner, a three-month buffer can disappear quickly.

2. Healthcare Costs Are Rising Rapidly

Medical expenses are increasing faster than most people expect.

India’s healthcare inflation currently averages around:

12–14% annually

(Source: healthcare cost studies)

A hospitalisation that costs ₹2 lakh today could cost ₹4–5 lakh in the coming years.

For many families, one medical emergency can wipe out months of savings.

“Hospital bill planning ka sabse bada test hota hai.”

3. Household Expenses Have Grown

Families today face many regular expenses such as:

- school and tuition fees

- rent or home loan EMI

- groceries and daily needs

- transport and fuel

- mobile and internet services

In many towns and growing urban centres, a typical household may spend ₹30,000–₹70,000 per month on essential needs.

If income stops suddenly, financial pressure can build quickly.

4. Market Volatility

Whether you run a wholesale business or work in a local factory, income isn’t always a smooth line. A 3-month buffer doesn’t give you enough time to pivot or wait for the market to bounce back.

The Modern Safety Rule: 6 Months or More

Because of these realities, financial planners increasingly recommend:

Emergency Fund = 6 Months of Essential Expenses

In some cases—especially for small business owners or self-employed professionals 9 to 12 months may be even safer.

For example:

Monthly household expenses = ₹40,000

3-month buffer = ₹1.2 lakh

6-month buffer = ₹2.4 lakh

The difference may seem large, but the extra protection provides more time and financial stability during uncertainty.

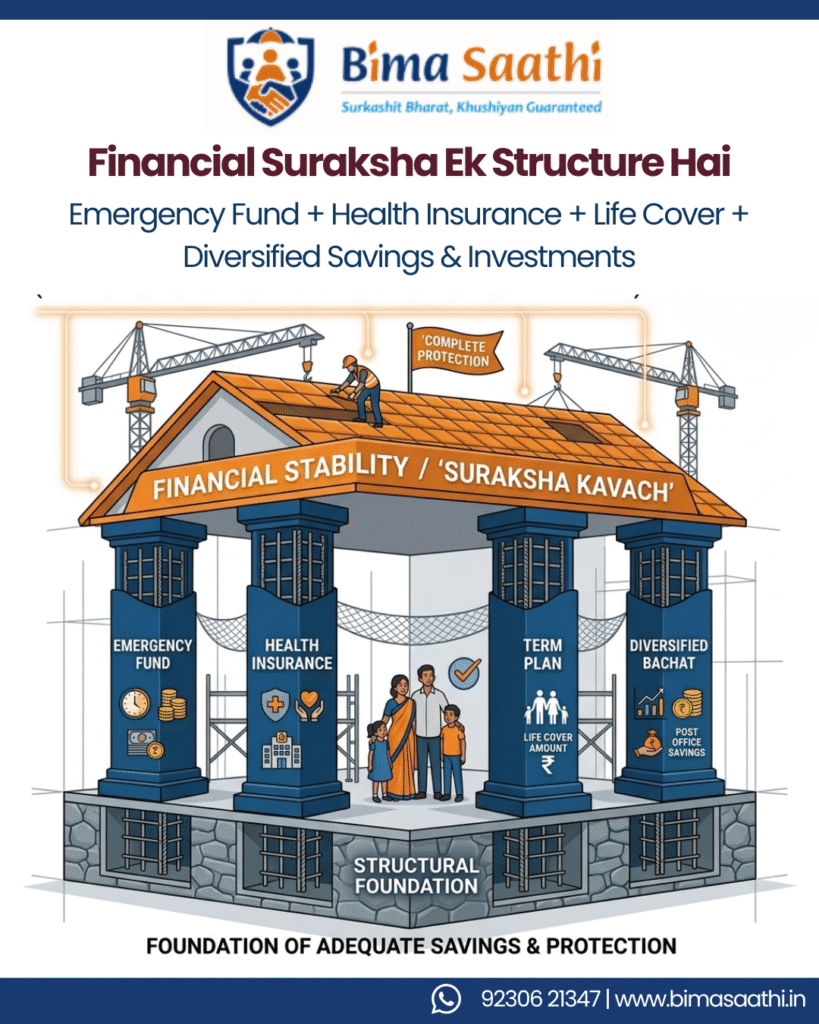

Emergency Funds Alone Are Not Enough

While emergency savings are important, they are only one part of financial protection.

A stronger financial safety system usually includes multiple layers.

Think of it like building a house.

One wall is not enough.

You need a structure.

1. Emergency Fund: The First Line of Defence

This is your immediate protection.

It helps cover:

- daily expenses

- short-term emergencies

- temporary income disruptions

Even starting with ₹2,000–₹5,000 per month can slowly build this safety net.

“Chhoti savings bhi bada safety net ban sakti hai.”

2. Insurance: Protecting Against Large Financial Shocks

Some emergencies are simply too expensive to handle through savings alone.

This is where insurance becomes important.

Key protection tools include:

- Health insurance – protects against hospital costs

- Term life insurance – protects family income security

- Personal accident cover – protects against disability or income loss

Insurance acts like a financial shock absorber.

“Insurance bade financial jhatko ko control karta hai.”

3. Income Continuity Planning

Another important protection strategy is income continuity.

This means preparing for situations where income may temporarily stop.

Ways people do this include:

- building multiple income streams

- developing side skills

- having freelance or advisory opportunities

In many towns today, people combine their primary work with additional roles such as:

- consulting

- tutoring

- online services

- advisory work

Even small secondary income sources can provide stability during difficult periods.

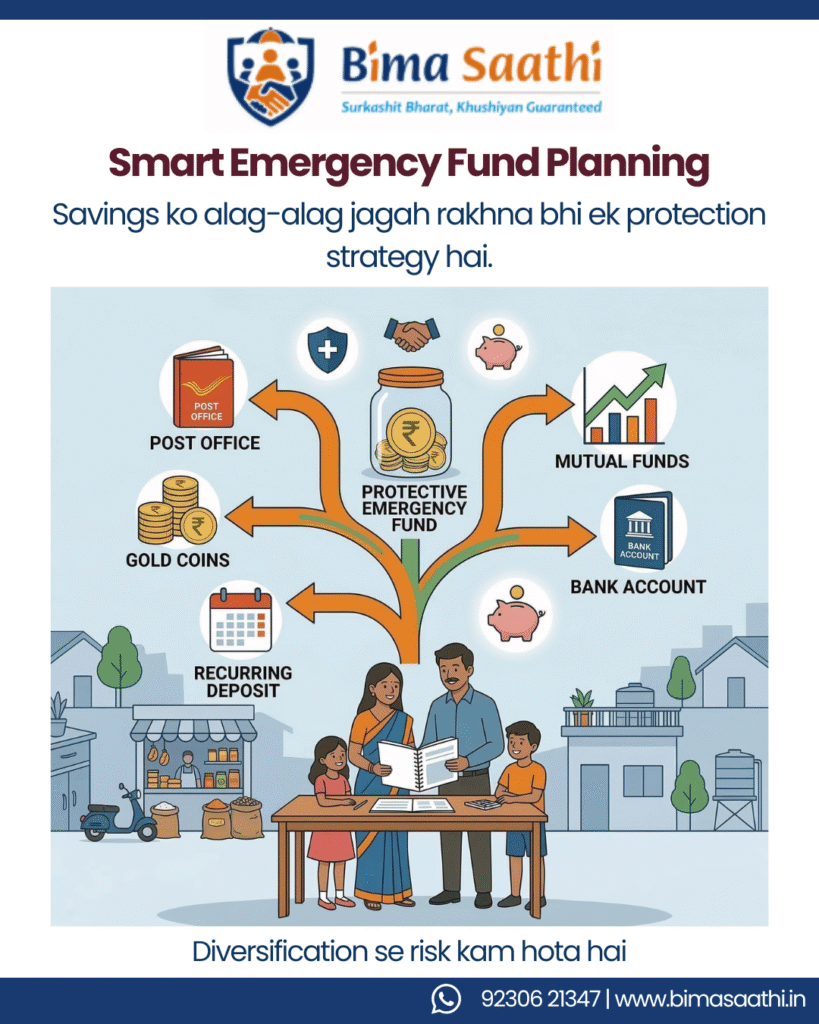

4. Diversified Investments

Diversify Your “Bachat”

Don’t put all your eggs in one basket.

- Small Savings Schemes: Post Office schemes are great for safety.

- Mutual Funds (SIPs): Even ₹500 a month in a diversified fund can help grow your wealth faster than inflation.

- Gold: Keep it for emergencies, but don’t make it your only investment, as selling it in a hurry often leads to lower returns.

A balanced financial plan may include:

- bank savings

- recurring deposits

- mutual funds

- long-term investments

Diversification helps protect financial growth from market changes.

In simple terms:

“Saare paisa ek jagah rakhna bhi risk ho sakta hai.”

Everyday Situations Where Financial Buffers Matter

Financial disruptions don’t always come in dramatic ways.

Sometimes they appear through everyday situations like:

- a shop owner facing slow business during off-season

- a salaried employee waiting months for a new job opportunity

- a sudden hospital admission for a family member

- unexpected house repairs after heavy rains

These are common realities for many households.

That is why financial preparedness matters even more outside big metropolitan cities.

Why Financial Awareness Is Still Growing

Despite its importance, many households still do not actively plan emergency funds.

Financial studies indicate that:

Nearly 70–75% of Indian households lack adequate emergency savings.

The main reasons are:

- lack of awareness

- delayed financial conversations

- confusion about financial products

This is where trusted guidance becomes valuable.

The Role of POSP Advisors

Across many towns and smaller cities, financial awareness often spreads through community conversations.

People prefer to learn from someone they know.

A neighbour.

A friend.

A trusted advisor.

This is where POSP advisors play an important role.

A POSP (Point of Sales Person) helps families understand:

- insurance protection

- financial risk planning

- emergency preparedness

By explaining these concepts clearly, they help families make informed financial decisions.

A Growing Opportunity in Financial Awareness

As financial awareness increases, many individuals are exploring the POSP career path.

This role offers:

- flexible working opportunities

- the ability to guide families responsibly

- income potential through advisory services

- meaningful community impact

In many communities, trusted financial guidance is still limited.

That means awareness and education can make a real difference.

“Jab samajh badhti hai, tab financial stability bhi badhti hai.”

A Simple Thought to Remember

Emergencies rarely announce themselves in advance.

Financial planning is not about predicting every crisis.

It is about preparing for uncertainty.

The traditional 3-month rule was a good starting point.

But today’s world often requires a stronger financial cushion.

So remember this idea:

“Emergency fund strong ho, toh mushkil waqt manageable ho jata hai.”

Start small.

Build gradually.

But make sure your financial safety net keeps growing.

Frequently Asked Questions (FAQ)

1. What is emergency fund planning?

Emergency fund planning involves saving money specifically to handle unexpected expenses such as medical emergencies, job loss, or financial disruptions.

2. How much emergency fund should a family maintain?

Most financial experts recommend keeping at least six months of essential household expenses as an emergency fund.

3. Why is a 3-month emergency fund not always enough?

Due to rising living costs, longer job search periods, and healthcare inflation, many households need a larger financial buffer.

4. Can insurance replace an emergency fund?

No. Insurance protects against large financial risks, but emergency funds are needed for everyday financial disruptions and immediate expenses.

5. How can financial advisors help with emergency fund planning?

Financial advisors and POSP professionals help families understand financial risks and create practical strategies for savings, protection, and financial stability.

Take the Next Step with Bima Saathi!

Is your family’s safety net strong enough? Or are you looking to help others in your town build their own “Suraksha Kavach”? At Bima Saathi, we are dedicated to bringing financial literacy to every corner of India.

Connect With Us Today:

- Protect Your Family: Talk to a Bima Saathi expert to design your 12-month security plan.

- Become a Bima Saathi POSP: Join us and start your journey as a financial leader in your community.

📞 Call / WhatsApp: +91 92306 21347

📧 Email: support@bimasaathi.in

🌐 Website: www.bimasaathi.in

Decision aapka hoga. Saath hum denge.

Leave A Comment